IHS Markit, Ovum, ABI Research and TBR have revealed their predictions for the global telecom operators and their investment pattern (Capex) for the next couple of years.

Global telecom Capex is anticipated to increase at a five-year (2016‒2020) compound annual growth rate (CAGR) of 0.8 percent, reaching $353 billion in 2020, according to IHS Markit.

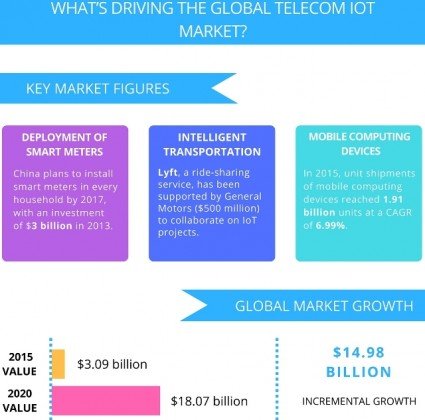

ALSO READ: Telecom Trends and Drivers Biannual Market Report

Vodafone, Deutsche Telekom, Orange, Telefonica and Telecom Italia, Europe’s five largest telecom service providers, achieved moderate revenue growth in 2016, switching from five consecutive years of unabated revenue decline. The telecom industry is anticipating that these five operators will start spending in coming years.

Capex in 2017

Telecom Capex growth is likely to be flat through 2017. A pickup in telecom Capex is expected in 2019, potentially driven by related 5G spending.

5G operators such as KT, NTT DOCOMO and SK Telecom don’t expect a major Capex hike due to 5G investment. Rather, fiber-based fixed broadband and backbone networks will be the major areas of spending.

Top-tier telecom providers will pursue a dual strategy in 2017 and beyond. They will continue to drive the transformation of their infrastructure to lower Capex and Opex costs. They will position themselves more deeply in the digital services ecosystem, seeking pockets of profitable service opportunities, according to TBR.

ALSO READ: TBR predictions on telecom industry for 2017

TBR predicts that global telecom provider Capex will dip in 2017. Beginning in 2018, efficiencies from early adopters of infrastructure transformation (specifically OSS/ BSS transformation and NFV/SDN) will improve service offers.

“Cost benefits will require greater scale and the retirement of legacy infrastructure, which will not be realized until at least 2020. Similarly, the revenue and investment advantages of 5G will slowly ramp from pre-5G in 2018 to greater deployment,” said Michael Sullivan-Trainor, executive analyst at TBR.

The anticipated flat growth in Capex is a not good news for leading telecom equipment makers such as Huawei, Ericsson, Nokia, Cisco, NEC, ZTE, HPE, IBM, Juniper Networks, Dell, Oracle, among others.

Telecoms going for digital

Ovum says CSPs are going digital. Some are moving into new markets and seeking a role in the digital transformation of our economies and societies. They want to be at the center of the Internet of Things.

Others are sticking with traditional telecom services but are using digital technologies and processes to become more efficient and improve the customer experience.

CSPs will invest in IT systems, platforms, and software that will allow them to operate in a digital ecosystem, while using analytics to optimize the network to enhance the customer experience.

1 in 3 telecom executives expect a significant increase in spending on digital solutions in the next 18 months. Investment in cloud, big data analytics, and upgrading systems to facilitate partnerships and enable customer centric services are the the priorities.

ABI Research predicts many top telecoms will transform into digital service providers (DSPs) or risk losing out to over-the-top (OTT) players like Google and WhatsApp.

T-Mobile’s digital offerings has played a huge role in boosting the company’s total revenue by 48 percent over the past three years.

ALSO READ: ABI Research report on digital transformation

“But it may not be possible for all. While Tier Ones will probably transform to DSPs, smaller telecoms may remain access-oriented,” said Sabir Rafiq, research analyst at ABI Research.

BSS and OSSs are reactive platforms capable of providing telecoms with basic services, such as configuration management and billing.

ABI Research says telecoms need to invest in DevOps and Agile development models. Telecoms will be able to rapidly launch new services and improve their services post launch in real time as they receive detrimental feedback from customers.

Is 4G investment over?

The telecom report by IHS Markit notes that the 2011‒2015 telecom equipment investment cycle driven by Long Term Evolution (LTE) is over.

IHS Markit said 2015 marked the end of a five-year global investment cycle that started in 2011 driven by LTE rollouts and their related fixed networks (core and transport).

“This cycle was characterized by synchronization between geographical regions, low single-digit yearly growth resulting from fewer but larger service providers that enjoy economies of scale, and various regional and national agendas,” said IHS Markit.

5G and IoT

But 4G investment by China Mobile, Reliance Jio and Bharti Airtel are going to have major impact on the data boom in Asia. These telecoms are not talking about 5G investment in the next 1-2 years.

Ericsson predicts that there will be 550 million 5G users by the end of 2022. If 5G picks up across the globe, there will be boom in IoT as well.

71 percent of enterprises are gathering data for IoT initiatives. This is a three percentage point increase from the previous quarter’s Voice of the Enterprise: IoT Workloads and Key Projects survey by 451 Research.

50 percent of respondents cite security as the top hurdle to IoT deployments. 41 percent cited IoT’s lack of perceived Return on Investment (ROI) and benefits as the next challenge. Enterprise IT respondents with IoT initiatives underway expect their mean IoT-related spending to grow by a robust 33 percent over the next 12 months.

Globally, major economies are set to boom. Any increase in GDP will further escalate the revenue growth of telecom operators.

IHS Markit’s macroeconomic indicators point to moderate economic growth of 2.5 percent in 2016 due to a mix of stronger growth in the U.S., Canada, Eurozone, the U.S. and Japan partially offset by weaker growth in Brazil, China and India.

Global real gross domestic product (GDP) is projected to increase 2.8 percent in 2017 and 3.1 percent in 2018.

Telecoms are gearing up for continuing to control over their Capex and Opex plans. Digital will be the focus areas for major operators.

Baburajan K

editor@telecomlead.com