The global semiconductor industry delivered record-breaking performance in the first quarter of 2026, powered by an unprecedented surge in artificial intelligence demand, particularly across data centers and memory.

AI infrastructure spending by hyperscalers pushed top chipmakers such as NVIDIA, TSMC, and Broadcom to new revenue highs, marking the start of a structural growth phase for the sector.

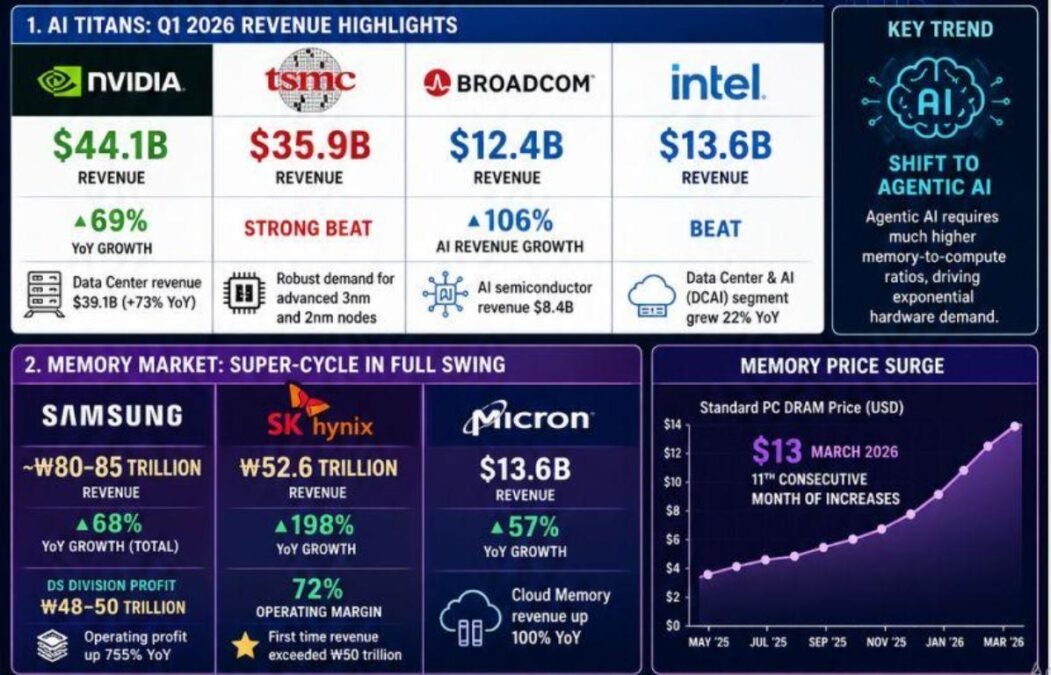

AI Leaders Post Explosive Growth

AI-focused semiconductor companies dominated Q1 2026 results, with strong gains driven by data center expansion and advanced chip demand.

NVIDIA reported $44.1 billion in revenue, up 69 percent, with data center revenue alone reaching $39.1 billion, growing 73 percent. The company’s growth was fueled by demand for its Blackwell architecture, despite a $4.5 billion export-related charge.

TSMC generated $35.9 billion in revenue, exceeding expectations on strong demand for advanced 3nm and 2nm nodes, while maintaining a high gross margin of 66.2 percent. Its leadership as the primary foundry for AI chips continues to strengthen.

Broadcom posted $12.4 billion in revenue, with AI semiconductor revenue surging 106 percent to $8.4 billion, reflecting strong demand for custom AI accelerators and networking chips.

Intel reported $13.6 billion in revenue, with its Data Center and AI segment growing 22 percent, supported by rising demand for AI inference workloads.

Memory Market Enters Super-Cycle

The memory segment witnessed a historic rebound, driven by shortages in high bandwidth memory and rising DRAM prices.

SK Hynix reported revenue of ₩52.6 trillion, up 198 percent, achieving a record 72 percent operating margin, as it strengthened its leadership in HBM3E supply.

Samsung Electronics posted total revenue of approximately ₩80 trillion to ₩85 trillion, with its Device Solutions division generating strong profits amid a 755 percent surge in operating income, driven by AI server demand and inventory recovery.

Micron Technology reported $13.6 billion in revenue, rising 57 percent, with cloud memory revenue doubling year-on-year due to AI-driven demand.

Stable Growth in Mobile, Automotive, and Equipment

Outside AI, segments such as mobile and automotive delivered steady performance.

Qualcomm reported a record $12.3 billion in revenue, with automotive revenue exceeding $1 billion for the second consecutive quarter, supported by its expansion into data center markets.

ASML posted €8.8 billion in revenue, with strong demand for lithography equipment, particularly in logic chip manufacturing, despite near-term margin pressures.

AMD is expected to report strong results, driven by the rollout of its MI300 and MI350 AI accelerators.

Key Industry Trends in Q1 2026

The semiconductor market is transitioning from generative AI to “agentic AI,” which requires significantly higher compute and memory resources, increasing demand for advanced chips.

Memory prices continued to surge, with standard PC DRAM prices reaching $13 in March 2026, marking the eleventh consecutive month of increases.

Advanced node utilization remained tight, with TSMC and Intel reporting near-full capacity for sub-5nm nodes, while demand for legacy nodes stayed relatively weak.

Strong Outlook for 2026 and Beyond

The latest Omdia report indicated there will be a significant increase in semiconductor revenue growth forecast for 2026 to 62.7 percent, driven by exceptional demand for memory chips amid ongoing supply constraints. The DRAM market is expected to nearly double in value, while NAND revenue could surge up to four times compared to 2025 levels.

The strong growth is being fueled by rising adoption of AI workloads, particularly in enterprise and data center environments. At the same time, supply shortages are intensifying as manufacturers prioritize high bandwidth memory production, which offers higher margins but limits overall output.

Semiconductor companies have issued bullish forecasts for the remainder of 2026 and into 2027, supported by sustained AI demand.

NVIDIA expects revenue of $54 billion in Q3 FY26, with Blackwell chips already sold out for the next 12 months, while Broadcom is targeting $100 billion in AI chip revenue by 2027.

TSMC has raised its capital expenditure to as high as $56 billion and expects revenue growth above 30 percent in 2026, highlighting strong demand for its 2nm technology.

ASML has increased its full-year sales guidance to €36 billion to €40 billion, reflecting continued investments in next-generation chip manufacturing.

Micron indicated that its HBM supply is fully booked for 2026, while SK Hynix is accelerating capacity expansion with new fabs to meet long-term demand.

Semiconductor Stocks Rally on AI Momentum

Investor confidence in the AI-driven semiconductor boom pushed the Philadelphia Semiconductor Index to record highs, rising 3.2 percent in a single session and delivering more than 47 percent gains year-to-date, Reuters news report said.

Semiconductor companies are expected to report first-quarter earnings growth of 109.2 percent, significantly outperforming the broader S&P 500 information technology sector, which is forecast to grow 48.2 percent.

Shares of Intel surged 22.6 percent, while AMD rose 13.7 percent and Arm gained 12 percent, reflecting strong demand for AI infrastructure.

Structural Growth with Emerging Risks

The semiconductor industry has entered a structural growth phase driven by exponential increases in AI “token consumption,” as agentic AI systems require significantly more compute and memory.

However, risks remain as companies ramp up capital expenditure exceeding $150 billion collectively, raising concerns about a potential supply glut beyond 2027.

For now, strong AI demand continues to outweigh these concerns, positioning the semiconductor sector as one of the fastest-growing industries in 2026.

BABURAJAN KIZHAKEDATH