Smartphone buyers in Q1 2026 are clearly shifting preferences, and the latest shipment and market share data from IDC shows why some brands are gaining demand while others are losing ground.

Buyers are moving toward premium and reliability

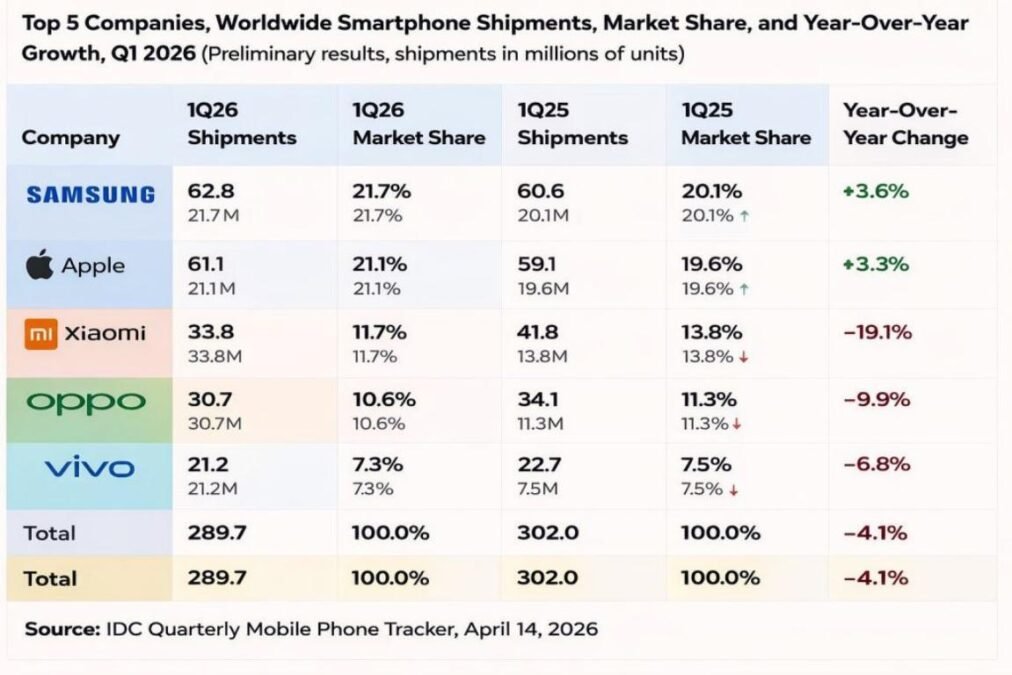

If you are buying a smartphone in 2026, chances are you are leaning toward brands that offer longer lifespan, better performance, and consistent updates. This is reflected in the numbers:

Samsung shipments increased to 62.8 million units in Q1 2026 from 60.6 million in Q1 2025, with market share rising from 20.1 percent to 21.7 percent

Apple shipments grew to 61.1 million units from 59.1 million, with share expanding from 19.6 percent to 21.1 percent.

“Apple and Samsung benefited from their dominance in the premium segment where they strategically held back price increases, while others such as Xiaomi, OPPO, and vivo made concerted efforts to shift share to higher price bands,” said Kiranjeet Kaur, associate director of Consumer Devices, IDC, said.

From a smartphone buyer perspective, this means more people are choosing premium devices, even if prices are higher, because they expect better durability, camera performance, and ecosystem benefits.

Mid-range smartphone buyers are becoming more cautious

Brands like Xiaomi, OPPO, and vivo traditionally attract smartphone buyers looking for value-for-money devices. But in Q1 2026, buyer behavior has changed:

Xiaomi shipments dropped from 41.8 million to 33.8 million, with share falling from 13.8 percent to 11.7 percent,

OPPO declined from 34.1 million to 30.7 million, with share slipping from 11.3 percent to 10.6 percent.

Vivo shipments fell from 22.7 million to 21.2 million, with share slightly down from 7.5 percent to 7.3 percent.

For smartphone buyers, this reflects growing hesitation in the mid-range segment. With rising prices, many are either delaying upgrades or stretching budgets toward premium brands instead of buying mid-tier smartphones.

Fewer options in the budget segment

The “Others” category declined, with shipments falling from 83.6 million in Q1 2025 to 80.1 million in Q1 2026, while market share remained almost flat at 27.7 percent vs 27.6 percent.

This suggests that smartphone buyers are finding fewer compelling options in the lower price segments, leading to reduced demand across smaller brands.

Overall buying sentiment is cautious

Total smartphone shipments dropped from 302.0 million units to 289.7 million units, a 4.1 percent decline, showing that many consumers are:

Holding on to devices longer

Waiting for better deals or upgrades

Prioritizing essential features over frequent upgrades

What this means for buyers

From a consumer perspective, the Q1 2026 trend is clear:

Buyers prefer trusted brands with strong ecosystems

There is a shift toward quality over price

Upgrade cycles are getting longer due to higher costs

Mid-range brands need stronger differentiation to win back demand

Bottom line

The Q1 2026 smartphone market reflects a more selective and value-conscious buyer mindset. Samsung and Apple are gaining because they meet expectations around performance and longevity, while Xiaomi, OPPO, and vivo are losing ground as buyers rethink spending in a more uncertain market.

BABURAJAN KIZHAKEDATH