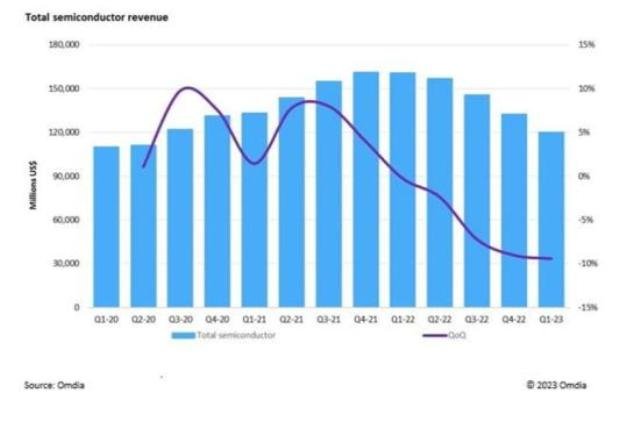

The semiconductor industry experienced a record fifth consecutive quarterly decline in revenue during the first quarter of 2023, according to a research report by Omdia.

This sustained downturn, the longest since 2002 when Omdia began tracking the market, has raised concerns within the industry. Revenue in 1Q23 settled at $120.5 billion, marking a significant 9 percent decline from 4Q22. The semiconductor market’s cyclical nature follows a period of remarkable growth between 4Q20 and 4Q21, driven by increased demand during the global pandemic.

This sustained downturn, the longest since 2002 when Omdia began tracking the market, has raised concerns within the industry. Revenue in 1Q23 settled at $120.5 billion, marking a significant 9 percent decline from 4Q22. The semiconductor market’s cyclical nature follows a period of remarkable growth between 4Q20 and 4Q21, driven by increased demand during the global pandemic.

Memory and MPU Markets Struggle

Key contributors to the decline were the memory and Microprocessing Units (MPU) markets. The MPU market in 1Q23 amounted to $13.1 billion, representing only 65 percent of its size in 1Q22 when it reached $20 billion. The memory market suffered even more, with 1Q23 revenues at $19.3 billion, merely 44 percent of its size in 1Q22 when it reached $43.6 billion. The combined decline of both MPU and memory markets resulted in a 19 percent decrease in 1Q23, dragging the overall market down to a 9 percent quarter-over-quarter (QoQ) decline.

Generative AI Brings Hope

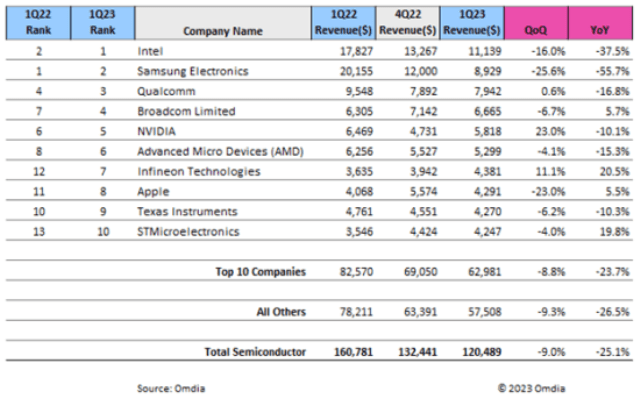

Cliff Leimbach, Senior Analyst at Omdia, highlighted that a lack of demand in the semiconductor market has persisted for multiple quarters, leading to declining Average Selling Prices (ASPs) for many components. However, generative AI has emerged as a beacon of hope for the industry. NVIDIA, a leader in this space, experienced strong revenue growth as they capitalized on generative AI, bucking the trend for most semiconductor companies in the beginning of 2023. Nevertheless, other semiconductor companies are yet to leverage this domain in a similar manner.

Shifts in Market Share Rankings

The continuous decline in the memory market over the past three quarters has significantly reshaped the market share rankings. Previously, three of the top five semiconductor companies by revenue were memory-focused companies: Samsung, SK Hynix, and Micron. However, only Samsung remains in the top ten rankings, signifying the challenges faced by memory-focused semiconductor companies. SK Hynix and Micron, which were previously part of the top ten, are no longer in the rankings, marking the first time since 2008 that they have encountered such struggles.

NVIDIA and Infineon Show Resilience

NVIDIA, releasing its financial results after the CLT report publication, surpassed estimates due to strong demand for the company’s generative AI chips. This robust performance demonstrated the potential of AI-driven innovations in the semiconductor industry.

Infineon, on the other hand, entered the top ten rankings this year following an impressive 11 percent increase in QoQ revenue. The company’s strength in the automotive sector played a crucial role in its rise.

Industry’s Outlook

The semiconductor industry remains cautiously optimistic despite the prolonged decline. The potential of generative AI and opportunities in various sectors, such as automotive, may pave the way for recovery. As the market continues to evolve, companies are likely to explore new avenues and adapt to changing consumer demands to drive future growth.