IDC in its latest research report revealed that business transformation of Intel addresses largest market opportunities.

In 2022, Intel unveiled a new strategy aimed at achieving a 10-12 percent annual revenue growth by 2026.

In 2022, Intel unveiled a new strategy aimed at achieving a 10-12 percent annual revenue growth by 2026.

The cornerstone of this strategy involved shifting its focus from smaller, slower-growing markets to larger, high-growth markets. By implementing this approach, Intel successfully expanded the size and growth potential of its serviceable addressable market (SAM).

As part of this strategic shift, Intel made strategic exits from certain market segments such as memory, connected home, and cellular modems, while simultaneously entering new segments like foundry wafer, discrete GPUs, and high-performance computing (HPC) processors.

Figure 1 compares Intel’s semiconductor and wafer foundry markets SAM after its reorganization (2022 New) to its SAM before its reorganization (2022 Old).

IDC said Intel’s new semiconductor and wafer foundry SAM in 2022 amounted to $351.9 billion, which was 45 percent larger than what its old semiconductor SAM would have been for the same year. Furthermore, this new $351.9 billion SAM represented 50 percent of the total semiconductor and wafer foundry markets ($711.6 billion) in 2022, surpassing the 34 percent share that its old $243.1 billion SAM would have represented. This growth in SAM positions Intel favorably in a market opportunity that is growing at a faster pace than the overall semiconductor and wafer foundry markets combined.

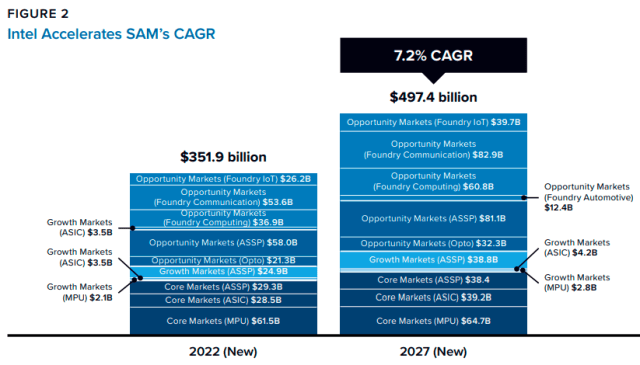

Another important indicator of Intel’s progress lies in how its strategic realignment has prepared it for emerging market opportunities, characterized by a new SAM that experiences higher growth rates compared to the overall semiconductor and wafer foundry markets.

Figure 2 compares Intel’s new SAM in 2022 to the forecast of that new SAM for 2027. This comparison shows Intel’s new SAM will grow at a compound annual growth rate (CAGR) of 7.2 percent from $351.9 billion in 2022 to $497.4 billion in 2027. In contrast, the combined semiconductor and wafer foundry markets will grow at a CAGR of 6 percent from $711.6 billion in 2022 to $955.1 billion in 2027.

Figure 2 compares Intel’s new SAM in 2022 to the forecast of that new SAM for 2027. This comparison shows Intel’s new SAM will grow at a compound annual growth rate (CAGR) of 7.2 percent from $351.9 billion in 2022 to $497.4 billion in 2027. In contrast, the combined semiconductor and wafer foundry markets will grow at a CAGR of 6 percent from $711.6 billion in 2022 to $955.1 billion in 2027.

In 2022, Intel reported a total revenue of $63.1 billion, encompassing revenue from semiconductors as well as other sources. This figure represented a 16 percent decline (non-GAAP) compared to 2021. However, a closer analysis of these results reveals contrasting performance within Intel’s business units. The business units operating within the new solution segments of Intel’ SAM (foundry, automotive, graphics, communications) witnessed growth, whereas those based on traditional core segments (PC microprocessors, server microprocessors) experienced declines.

The drop in revenue can largely be attributed to the significant inventory correction taking place in the core segments, which were of greater magnitude due to their larger size. This decline in Intel’s revenue for 2022 stood in contrast to the modest 0.7 percent growth observed in the overall semiconductor market and the significant 28.9 percent growth observed in the total wafer foundry market.

Nonetheless, Intel’s strategic decision to exit volatile markets such as memory and consumer markets (connected home) shielded it from further decline in a semiconductor market undergoing a significant correction in the first half of 2023.

Intel’s transformation to focus on high-growth markets mirrors the broader transformation occurring in the semiconductor industry. Embracing a solutions-based approach driven by end-market demand, Intel is investing in semiconductors, software, hardware, and services that cater to future usage scenarios and build requirements.

For instance, Intel offers OpenAPI, which facilitates cross-architecture programming across all its business units, Unison through CCG to enable seamless connectivity between PCs and mobile devices, and Granulate through DCAI to optimize datacenter applications and workloads.