India’s telecom market in early 2026 is entering a more mature phase, with operators increasingly focusing on experience-led differentiation rather than price disruption to drive growth and retain subscribers. Following recent tariff adjustments and tighter regulatory emphasis on user-measured performance, telecom companies are reshaping their strategies around network quality, localized execution, and customer experience.

At a national level, Reliance Jio continues to dominate with more than 500 million subscribers and over 43 percent of the sector’s Adjusted Gross Revenue (AGR). Its 5G standalone deployment is not only influencing domestic market dynamics but also strengthening India’s position in Opensignal’s Global Network Excellence Index, where it ranks 15th among large landmass markets. Jio leads on Consistent Quality (CQ) in 58 out of 63 metro areas, reinforcing its strong nationwide presence.

However, national leadership alone no longer defines competitive success. Operators are increasingly discovering that subscriber gains and losses are determined at the metro and regional level rather than through broad national strategies, Opensignal’s Burhan Kamal – VP, Client Analytics & Insights for MEIA and Sylwia Kechiche – VP, Industry Analysis, said in a report.

BSNL continues to gain subscribers primarily through lower-priced plans, even as it trails competitors in CQ metrics. In contrast, Bharti Airtel is strengthening its position by attracting higher-value users through premiumization strategies, while Vodafone Idea is focusing investments on defending its presence in key circles.

Opensignal’s Subscriber Analytics highlights that competitive advantage is now increasingly local. Metro-level Consistent Quality (CQ) provides a more accurate indicator of subscriber movement than national averages. Operators are winning in markets where network performance aligns closely with localized commercial strategies, supported by targeted capital expenditure and customer value management.

This shift has given rise to what can be described as an “Urban Fortress” strategy, where telecom operators build strong, defensible positions in specific cities or regions by aligning network investments, performance, and tailored offerings.

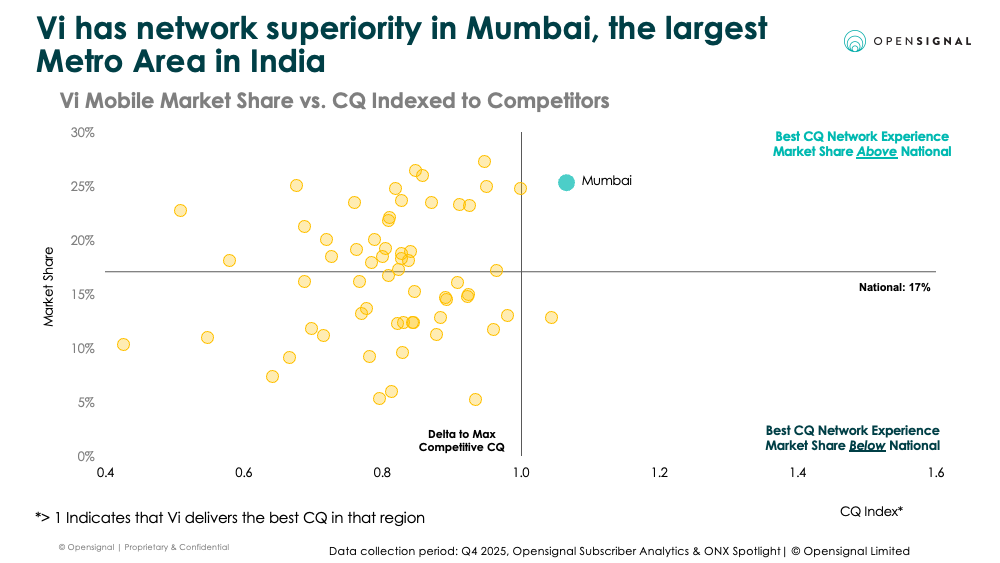

Vodafone Idea’s performance in Mumbai illustrates this trend. Despite experiencing subscriber losses nationally, with Jio accounting for 59 percent of its net losses in the fourth quarter of 2025, Vi maintains a strong foothold in Mumbai. This is supported by its ₹45,000 crore ($4.5 billion) Capex plan targeting 17 priority circles, including Maharashtra, combined with localized customer value management strategies such as Below-The-Line offers and region-specific digital bundles. Rather than engaging in nationwide price competition, Vi is reinforcing its market position through targeted, location-specific initiatives.

Vodafone Idea had 10,772,169 mobile phone customers in Mumbai in December-2025 as compared with 10,680,874 subscribers at the end of 2024, according to TRAI report.

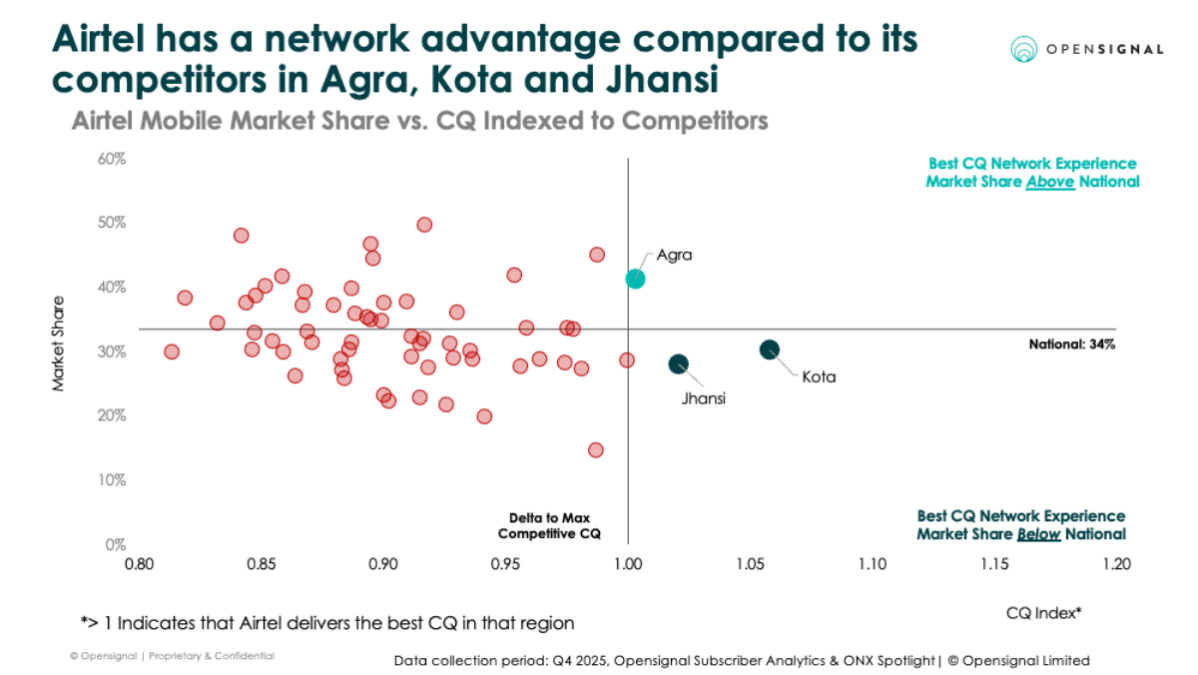

Bharti Airtel demonstrates a similar localized growth pattern. The operator has increased its national market share by around 1 percentage point since early 2024, with 73 percent of gains coming from Jio, indicating direct switching between premium users. Airtel’s success is particularly visible in cities such as Agra, Kota, and Jhansi, where strong network experience supports its premium offerings like Airtel Black converged plans. This growth is backed by sustained quarterly Capex exceeding ₹11,000 crore ($1.3 billion), enabling targeted network improvements in high-potential regions.

The evolving market dynamics also highlight the growing importance of the point of sale. With tariff hikes reducing the effectiveness of price-led acquisition, operators must now ensure that their network superiority is visible and credible to consumers in specific locations. Performance advantages translate into commercial success only when they are clearly communicated through both retail and digital channels.

Solutions such as Opensignal’s Frontline Network Experience (FNX) are enabling telecom operators to demonstrate independently verified, location-specific performance metrics. This allows frontline teams to move beyond generic claims of having the “best network” and instead present more relevant, localized propositions such as being better than a customer’s current provider.

The concept of relative performance is becoming a powerful tool in customer acquisition. Operators do not necessarily need to lead across an entire city; they can gain market share by outperforming the incumbent provider in specific areas. Even a marginal advantage in CQ can create opportunities to attract high-value subscribers, particularly when supported by precise, data-driven marketing.

As the Indian telecom market matures, the traditional one-size-fits-all national strategy is becoming less effective. Success in 2026 depends on a combination of hyper-local insights, targeted investments, and the ability to translate network performance into tangible customer value.

Telecom operators that master local positioning, leverage mobile network experience strategically, and communicate their strengths effectively at the point of sale will be best placed to sustain growth. Ultimately, experience-led differentiation is emerging as the defining factor in India’s telecom evolution, replacing price disruption as the primary driver of competition.

BABURAJAN KIZHAKEDATH