The global mobile telecom industry is strengthening its leadership in climate action, with mobile operators accelerating carbon reduction initiatives, renewable energy adoption, and science-based emissions targets.

According to the latest GSMA analysis, operators have reduced operational carbon emissions while expanding mobile connectivity and handling rapidly growing data traffic, although additional efforts will be required to meet 2030 decarbonization goals.

Mobile Operators Lead Corporate Climate Commitments

As of June 2026, 81 mobile operators have adopted near-term Science Based Targets (SBTs), representing nearly half of the global mobile industry by connections and more than two-thirds by revenue.

Among these operators:

77 operators have had their near-term targets validated by the Science Based Targets initiative (SBTi).

50 operators have committed to achieving net-zero emissions.

46 net-zero targets have already been validated by the SBTi.

Half of the validated net-zero targets aim to achieve net zero by 2040 or earlier.

Climate Reporting Improves Across the Telecom Industry

Mobile operators continue to outperform most industries in climate transparency.

A total of 77 operators submitted climate disclosures to CDP in 2025, compared with 61 operators in 2020.

Nearly one-third of reporting operators received CDP’s highest A rating in 2025, compared with less than 4 percent of companies across all other industries.

The report evaluates climate disclosure data from 116 mobile operators, representing approximately 85 percent of global mobile connections.

Telecom Industry Emissions Continue to Decline

The mobile industry’s operational emissions reached an estimated 115 million tonnes of CO₂ equivalent (MtCO₂e) in 2024, accounting for approximately 0.2 percent of total global greenhouse gas emissions.

Operational emissions (Scope 1 and Scope 2) represent around one-quarter of the industry’s overall carbon footprint, while Scope 3 value chain emissions contribute the remaining three-quarters.

Operational emissions declined by 5 percent during 2024, double the average annual reduction achieved over the previous four years.

Between 2019 and 2024, operators reduced operational emissions by 13 percent, despite mobile connections increasing by 10 percent and mobile data traffic expanding by more than four times.

Preliminary estimates indicate another 3 percent reduction during 2025.

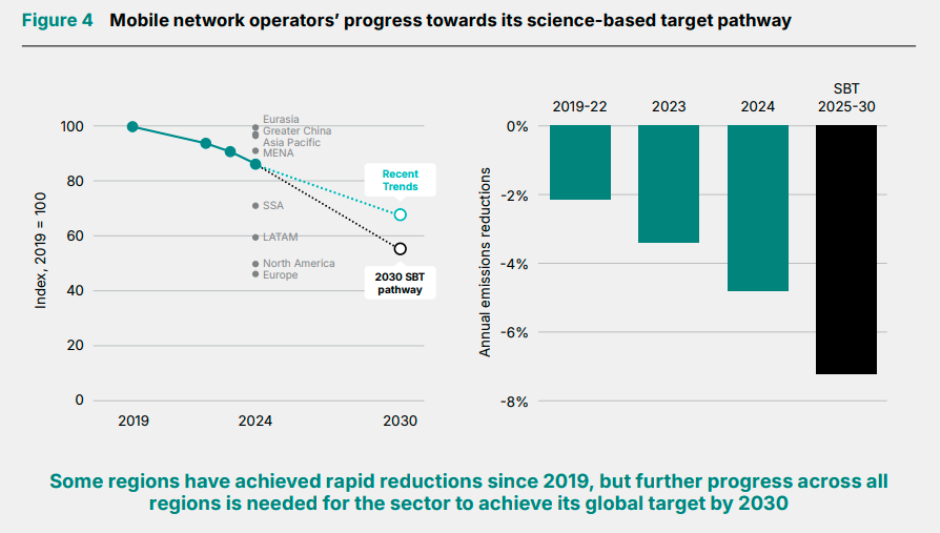

However, the industry remains behind its climate trajectory. Current trends suggest emissions will decline by 33 percent by 2030, compared with the 45 percent reduction required under the Science Based Targets pathway. Achieving this target will require average annual global emission reductions of approximately 7 percent, particularly across Asian markets.

Europe and North America Lead Regional Carbon Reductions

Every global region reduced operational emissions between 2019 and 2024.

Europe and North America each reduced emissions by more than 50 percent.

Latin America achieved a 40 percent reduction.

Sub-Saharan Africa reduced emissions by 30 percent.

Middle East and North Africa (MENA) lowered emissions by almost 10 percent.

Greater China recorded its first emissions decline in 2024, falling by a record 7 percent, supported by expanding renewable energy adoption.

Renewable Energy Becomes the Largest Driver of Emission Reductions

Mobile operators consumed approximately 300 TWh of electricity during 2024, representing roughly 1 percent of global electricity consumption.

Continuous network modernization and retirement of legacy infrastructure improved energy efficiency, reducing electricity consumption per mobile connection by 3 percent since 2019 to 29 kWh per connection in 2024.

Operators spent around $50 billion on energy during 2024, increasing the financial importance of energy efficiency and renewable electricity.

The industry purchased or generated approximately 70 TWh of renewable electricity in 2024.

Renewable energy’s contribution to total operator electricity consumption more than doubled from 10 percent in 2019 to 24 percent in 2024.

Regional renewable energy adoption varies significantly:

Europe: approximately 70 percent renewable electricity.

North America: 50 percent.

Latin America: 45 percent.

Mobile operators also consumed around 2.5 billion litres of diesel and gasoline during 2024.

Following the closure of the Strait of Hormuz, crude oil prices in April 2026 increased by more than 70 percent compared with the 2025 average. In diesel-dependent markets, operators are increasingly deploying solar-powered and hybrid energy systems, with early adopters reporting fuel cost savings of around 30 percent.

AI’s Impact on Telecom Energy Consumption Remains Uncertain

Artificial intelligence is rapidly increasing electricity demand from global data centres.

Worldwide data centre electricity consumption is projected to double to around 950 TWh by 2030, primarily driven by hyperscale cloud providers and AI workloads.

Currently, telecom operators account for less than 10 percent of total data centre electricity consumption, although investment announcements indicate significant future expansion among operators in Asia and the Middle East.

Direct generative AI traffic has nearly doubled over the past year but still represents only around 0.2 percent of total mobile traffic, suggesting AI has not yet materially increased mobile network energy consumption. However, indirect impacts, including higher consumption of AI-driven video content, remain uncertain.

Scope 3 Emissions Remain the Biggest Challenge

Approximately 75 percent of the telecom industry’s carbon footprint originates from Scope 3 value chain emissions, making supplier engagement essential.

The GSMA has introduced a new Scope 3 Assessment Tool to improve emissions measurement consistency across the industry.

Climate progress among suppliers varies significantly:

80 percent of major cloud and IT service providers have validated near-term science-based targets.

Around 50 percent of network equipment manufacturers and smartphone manufacturers have validated targets.

Fewer than 25 percent of the 25 largest tower companies have validated climate targets.

Tower Companies Present Major Decarbonization Opportunity

The report identifies telecom tower infrastructure as one of the industry’s largest remaining decarbonization challenges.

The world’s top 100 tower companies operate approximately 4 million telecom sites, representing around two-thirds of global telecom towers.

Together, they consume approximately 2 billion litres of diesel annually, primarily across Sub-Saharan Africa and the Asia-Pacific region.

Despite their environmental impact, only one-quarter of the top 100 tower companies publicly disclosed emissions data during the past year.

The GSMA recommends that mobile operators accelerate tower decarbonization by incorporating emissions reporting into master service agreements, restructuring energy contracts to reward carbon reduction, coordinating sustainability commitments across shared infrastructure, and replacing diesel generators with on-site solar power and battery storage to lower emissions while improving energy resilience.

BABURAJAN KIZHAKEDATH