India’s smartphone market is likely to contract by a mid-single-digit percentage in 2026, weighed down by rising device prices, cautious consumer spending and limited perceived gains from upgrading, according to new analysis from Omdia.

While seasonal demand and possible policy support could help stabilise shipments in the second half of the year, competitive dynamics are expected to shift away from headline innovation toward tighter cost control and sharper retail execution, Omdia report said.

Omdia expects Chinese smartphone brands with a strong entry-level focus to recalibrate their strategies, moving up the value curve into the ₹25,000 to ₹60,000 “flagship killer” segment. This price band offers relatively better margin headroom at a time when memory costs are climbing. In contrast, the ultra-premium segment above ₹60,000 is projected to remain structurally dominated by Apple, Samsung and vivo.

Rising memory prices and a depreciating rupee are constraining hardware-led differentiation across the industry. As a result, brands are increasingly leaning on channel-driven levers such as service and ecosystem bundling, deeper financing options, trade-in programs and phased launches aligned with component availability. Retail execution is emerging as a decisive factor.

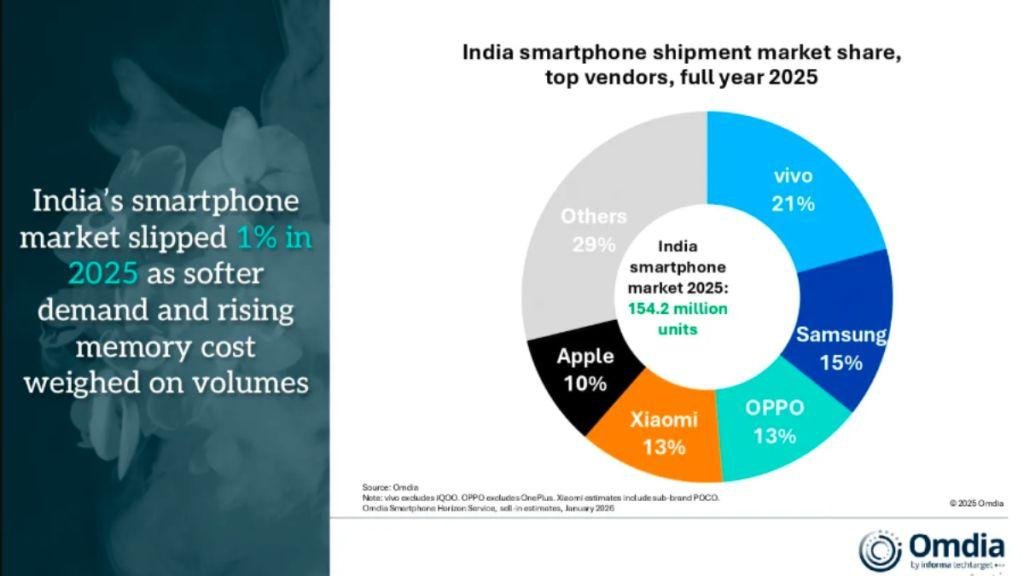

India’s smartphone shipments fell 7 percent year on year to 34.5 million units in the fourth quarter of 2025. For the full year, the market declined 1 percent to 154.2 million units. The Q4 slowdown reflected typical post-festive seasonality but was amplified by elevated channel inventories, currency pressure and weakened affordability in the mass market following price hikes linked to memory inflation.

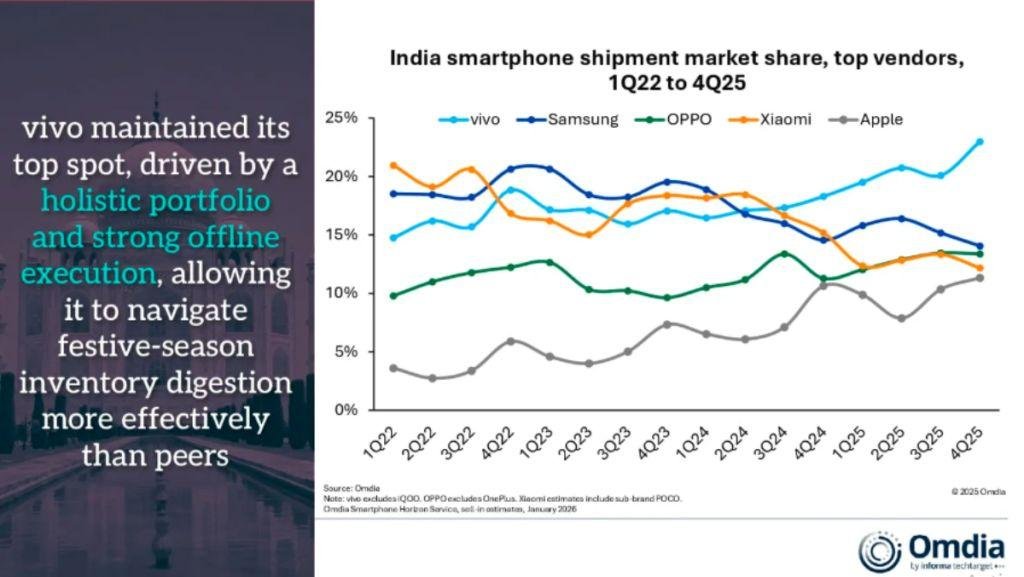

Over the full year 2025, performance increasingly favoured brands that prioritised value-driven strategies over sheer volume. Companies with disciplined portfolio management, strong offline presence and tighter inventory control outperformed rivals pursuing aggressive shipment-led growth. This played out against a backdrop of higher input costs, elongated replacement cycles and restrained consumer demand.

vivo retained its leadership position in the December quarter, shipping 7.9 million units and capturing a 23 percent market share. The brand also held the top spot for full-year 2025. Samsung followed with 4.9 million units and a 14 percent share, while OPPO excluding OnePlus overtook Xiaomi to secure third place with 4.6 million units and a 13 percent share. Xiaomi and Apple shipped 4.2 million and 3.9 million units, respectively.

Several vendors quietly reset maximum operating prices during the quarter, particularly in LPDDR4-heavy and price-sensitive segments, to pass through higher component costs. Pricing adjustments affected both new launches and carry-over models, reflecting the combined impact of memory inflation and currency depreciation.

vivo emerged as the strongest pull brand in the market, drawing demand from both consumers and retailers. Its Q4 performance was anchored by high volumes from models such as the Y31 5G, Y19s 5G, T4X 5G and V60e. The company benefited from deep offline penetration, a large on-ground promoter network and a decentralised operating model that allows faster execution at the state level.

OPPO maintained momentum through a balanced A- and K-series strategy, with the A-series driving scale and the K-series gaining traction in mainline retail. Both OPPO and vivo followed a disciplined six-month refresh cycle for their V- and Reno-series portfolios and actively supported retailers through ageing stock clearance and shelf-level competition management, helping sustain sell-out visibility during a broader market correction.

Samsung saw volumes soften despite targeted upgrade and cashback programs around the Fold 7 and S25 FE. Xiaomi’s shipments also declined, even as it avoided aggressive price hikes, with volumes largely supported by entry models such as the Redmi 14C 5G and POCO C75. Apple’s performance remained broadly flat, supported by steady demand for the iPhone 17 base model, as some consumers delayed purchases in anticipation of promotional offers on older iPhone models early in 2026.

realme faced volume pressure following pricing adjustments, though models including the 15X, C71 and C73 helped cushion the impact. Among challengers, OnePlus returned to growth after rebuilding relationships with mainline retailers, supported by a strong offline response to the OnePlus 15 series. Motorola and Nothing continued selective offline expansion, focusing on high-traffic stores with targeted promoter deployment.

As the market heads into 2026, Omdia expects execution at the retail level, rather than breakthrough features, to determine which brands can weather a softer demand environment and protect profitability in India’s increasingly value-conscious smartphone market.

BABURAJAN KIZHAKEDATH