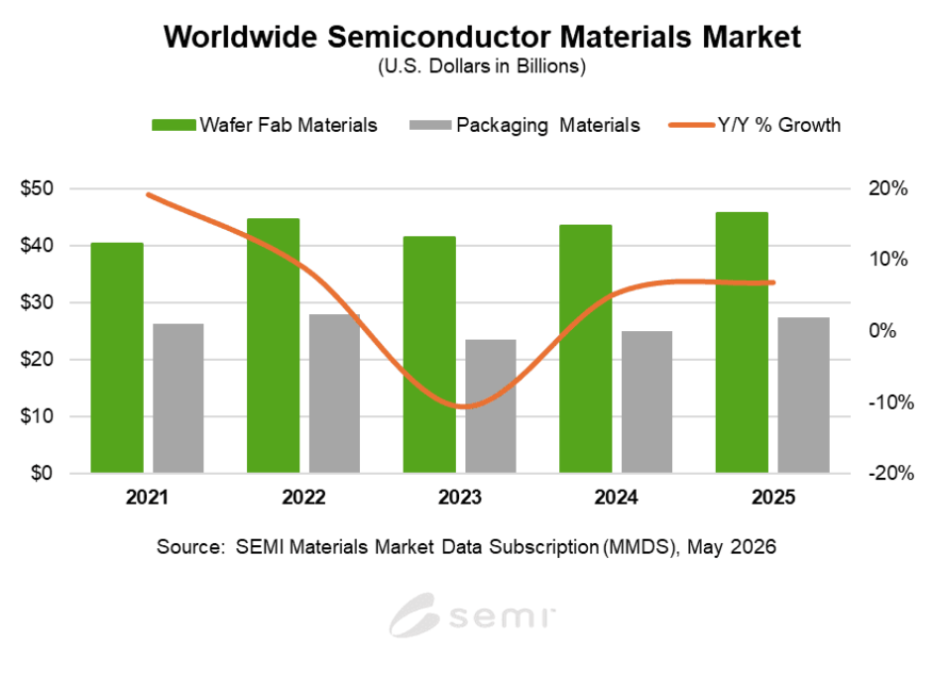

The global semiconductor materials market recorded strong momentum in 2025, with revenue increasing 6.8 percent year-over-year to $73.2 billion, according to data from SEMI. The growth was fueled by rising demand for artificial intelligence (AI), high-performance computing (HPC), advanced memory technologies, and increasing complexity in semiconductor manufacturing processes.

The semiconductor industry continued to benefit from investments in advanced-node chip production, next-generation packaging technologies, and AI infrastructure expansion. Growth was visible across both wafer fabrication materials and packaging materials segments during the year, SEMI report showed.

Wafer fabrication materials revenue rose 5.4 percent to $45.8 billion in 2025. Strong demand for lithography-related materials, including photomasks, photoresists, and ancillary materials, supported growth as semiconductor manufacturers increased production of advanced chips requiring tighter lithography precision and higher process intensity. Wet chemicals also posted double-digit growth due to rising materials consumption in leading-edge semiconductor manufacturing.

Packaging materials revenue outperformed the wafer fabrication segment, increasing 9.3 percent to $27.4 billion. Advanced substrates and bonding wire led the growth, supported by higher gold prices and strong demand for advanced chip packaging used in AI accelerators, graphics processors, and high-bandwidth memory applications.

The growing adoption of advanced packaging technologies such as chiplets, 2.5D packaging, and 3D integration is increasing demand for sophisticated substrate materials capable of supporting higher interconnect density, improved thermal management, and enhanced performance efficiency.

Regionally, Taiwan remained the world’s largest semiconductor materials market for the 16th consecutive year, generating $21.7 billion in revenue in 2025. Taiwan’s dominance reflects its leadership in global foundry manufacturing and advanced semiconductor production.

China ranked second with semiconductor materials revenue of $15.6 billion and recorded the strongest growth among major regions at 12.5 percent. The expansion was supported by aggressive investments in domestic semiconductor manufacturing capacity and continued efforts to strengthen supply chain self-sufficiency.

South Korea secured the third-largest position with $11.2 billion in revenue, driven by strong demand for advanced memory chips, including DRAM and NAND flash technologies used in AI servers and data centers.

North America posted one of the strongest growth rates globally, with semiconductor materials revenue rising 10.7 percent to $6.2 billion. The region is benefiting from increased semiconductor manufacturing investments, AI chip demand, and government-backed initiatives aimed at strengthening domestic semiconductor supply chains.

Japan’s semiconductor materials market increased 2.3 percent to $6.8 billion, while the Rest of the World category grew 6.7 percent to $7.5 billion. The Rest of the World segment includes Singapore, Malaysia, the Philippines, other Southeast Asian countries, and smaller semiconductor manufacturing markets.

Europe was the only major region to report a decline, with semiconductor materials revenue falling 6.0 percent to $4.2 billion in 2025, reflecting weaker semiconductor manufacturing activity and slower industrial demand recovery.

The outlook for the semiconductor materials market remains positive as AI adoption, cloud computing growth, advanced memory demand, and investments in next-generation semiconductor technologies continue to drive global chip manufacturing expansion.

BABURAJAN KIZHAKEDATH