Fixed wireless access (FWA) technology is on the verge of a significant surge in popularity within the US broadband market, with projections indicating a substantial increase in subscription market share over the next five years.

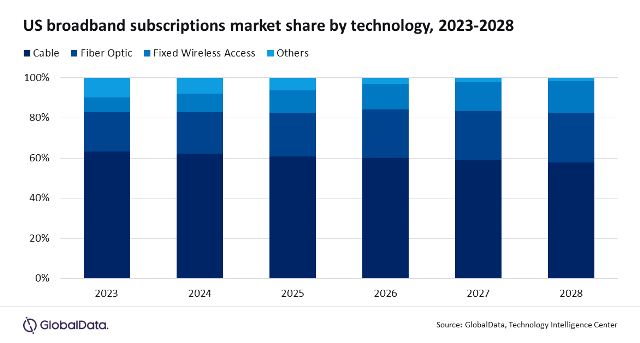

According to the latest report from GlobalData, titled “United States Fixed Communications Forecast,” FWA is expected to more than double its subscription market share, from 7.2 percent in 2023 to 15.8 percent in 2028.

According to the latest report from GlobalData, titled “United States Fixed Communications Forecast,” FWA is expected to more than double its subscription market share, from 7.2 percent in 2023 to 15.8 percent in 2028.

Despite this remarkable growth, FWA is anticipated to maintain its position as the third most popular broadband technology in the United States, trailing behind cable and fiber subscriptions. Principal Analyst at GlobalData, Tammy Parker, highlighted some of the key factors contributing to FWA’s appeal. These include its user-friendly self-installation process, affordability, and impressive reliability and performance, driven by underlying 5G technology.

Parker noted that FWA’s unique selling point lies in offering a fresh service alternative in comparison to existing solutions from established service providers. Moreover, FWA is versatile, catering to both primary and backup internet services and adaptable to locations requiring temporary connectivity.

While FWA’s growth is substantial, the cable technology is anticipated to retain its dominant position in the US fixed communications landscape, capturing a substantial 58 percent share of total broadband access lines by 2028. However, cable is facing escalating competition from the emergence of 5G FWA networks, orchestrated by mobile network operators, and the ongoing deployment of cutting-edge fiber-optic networks.

The rising prominence of fiber optics presents a notable challenge to the broadband market as it boasts remarkable reliability and the capability to deliver symmetrical multigigabit speeds, which are increasingly demanded by both consumers and businesses. Furthermore, government subsidies are fueling an unprecedented expansion of the nation’s fiber broadband infrastructure, leading to a projected increase in fiber technology’s market share from 19.5 percent in 2023 to 24.7 percent in 2028.

Cable operators are responding to these changes by upgrading their hybrid fiber/coax (HFC) networks with the advanced DOCSIS 4.0 technology. This enhancement is expected to support downstream speeds of up to 10 Gbps and an upstream capacity of up to 6 Gbps. This development will likely enable cable technology to maintain its predominant market position. Interestingly, some cable providers are also taking the initiative to roll out their own fiber networks, especially in situations where they are extending their services to nearby neighborhoods, a move that is projected to further bolster fiber technology’s market share.

The comprehensive report by GlobalData predicts a compound annual growth rate (CAGR) of 4.2 percent for the total revenue generated by US broadband services, projecting an increase from $102.9 billion in 2023 to $126.3 billion by 2028. FWA is expected to lead the revenue growth with a remarkable CAGR of 24.8 percent during the same period, while cable’s service revenue is predicted to experience a more moderate 1.5 percent CAGR, and fiber’s revenue is set to rise at a CAGR of 9.1 percent.