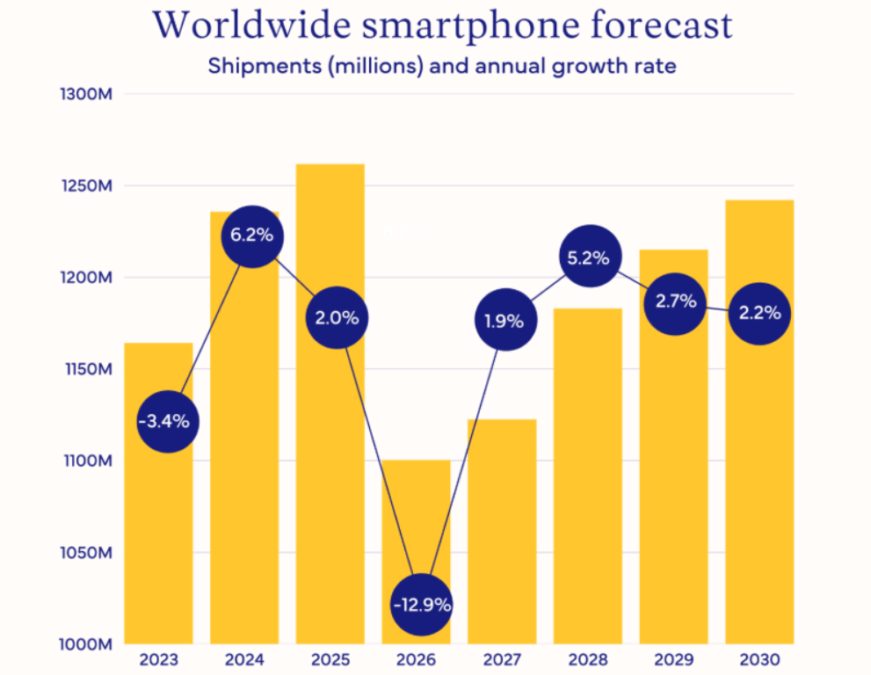

Worldwide smartphone shipments are projected to decline 12.9 percent in 2026 to 1.12 billion units, marking the lowest annual volume in more than a decade, IDC report indicated.

The revised outlook on the global smartphone industry reflects a sharp downgrade from IDC’s earlier November forecast, as the intensifying global memory shortage disrupts production, raises component costs, and squeezes margins across the consumer electronics industry.

Memory Supply Crisis Triggers Structural Reset

Francisco Jeronimo, vice president for Worldwide Client Devices at IDC, described the current situation as a systemic shock rather than a temporary supply squeeze.

The memory shortage, affecting key components such as DRAM and NAND, is creating ripple effects throughout the smartphone supply chain. Android vendors operating in the low-end segment are expected to face the most severe impact due to limited pricing power and thin margins.

Rising component costs are forcing manufacturers to pass higher prices to consumers, which is dampening demand in price-sensitive markets. IDC notes that vendors heavily reliant on entry-level devices are particularly vulnerable.

Apple and Samsung Positioned to Gain Market Share

While smaller Android brands struggle, premium-focused players such as Apple and Samsung Electronics are expected to navigate the disruption more effectively.

IDC suggests that as lower-tier competitors face shipment declines and potential exits, Apple and Samsung could expand their market share. Strong brand positioning, supply chain leverage, and diversified product portfolios give them greater resilience during periods of component inflation.

Smartphone ASP to Hit Record $523

Despite the projected drop in shipment volumes, smartphone average selling prices are forecast to rise 14 percent in 2026 to a record $523. IDC believes this price increase reflects both elevated memory costs and a shift in product mix toward mid-range and premium devices.

According to IDC senior research director Nabila Popal, the memory crisis marks a structural reset of the smartphone market. The total addressable market is expected to shrink as the sub-$100 segment becomes permanently uneconomical. IDC estimates that approximately 171 million devices previously sold below $100 will no longer be viable under current cost conditions.

Memory prices are projected to stabilize by mid-2027 but are unlikely to return to previous levels, signaling long-term changes in pricing strategies and product positioning.

Regional Impact: Emerging Markets Hit Hardest

Regions with high dependence on low-cost smartphones are forecast to experience the steepest shipment declines in 2026:

Middle East and Africa: Down 20.6 percent year-on-year

China: Down 10.5 percent

Asia Pacific excluding Japan and China: Down 13.1 percent

The contraction in these regions reflects both supply constraints and reduced affordability at higher price points.

Outlook for Recovery in 2027 and 2028

IDC forecasts that as memory supply conditions stabilize, the smartphone market could see a modest 2 percent recovery in 2027. A stronger rebound of 5.2 percent year-on-year growth is expected in 2028.

However, analysts emphasize that the market will not return to its previous structure. Consolidation among smaller vendors, a higher pricing baseline, and a continued shift toward premium devices are likely to define the next phase of the global smartphone industry.

The 2026 downturn underscores how deeply semiconductor supply chains influence global technology markets, with long-term implications for smartphone vendors, consumers, and component suppliers alike.

BABURAJAN KIZHAKEDATH