Worldwide semiconductor revenue in 2023 reached $533 billion, reflecting an 11.1 percent decline from the previous year, Gartner reveals in a report.

The semiconductor industry has faced significant challenges, witnessing cyclicality and grappling with one of the steepest declines in memory revenue in its history, according to Alan Priestley, VP Analyst at Gartner.

The semiconductor industry has faced significant challenges, witnessing cyclicality and grappling with one of the steepest declines in memory revenue in its history, according to Alan Priestley, VP Analyst at Gartner.

“While the semiconductor industry experienced its typical cyclicality in 2023, the market endured a challenging year, with memory revenue suffering one of the most substantial declines in history,” noted Alan Priestley. “This underperformance had a ripple effect, adversely affecting several semiconductor vendors, with only 9 out of the top 25 vendors posting revenue growth in 2023, and 10 experiencing double-digit declines.”

Intel Regains Top Position in 2023

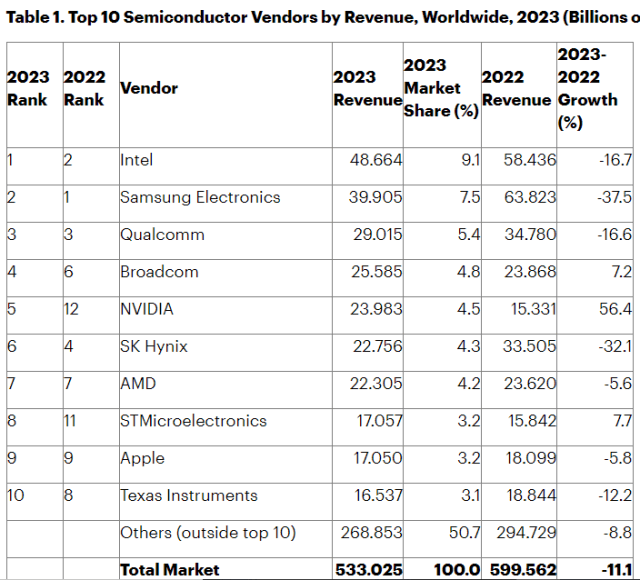

Following the challenges faced by memory vendors, the ranking of the top 10 semiconductor vendors underwent significant changes compared to the previous year.

Intel has reclaimed the No.1 position from Samsung, securing the top spot after two years in the No. 2 position. Intel’s 2023 revenue amounted to $48.7 billion, surpassing Samsung’s revenue of $39.9 billion.

Nvidia experienced notable growth in 2023, with semiconductor revenue increasing by 56.4 percent to reach $24 billion. This achievement propelled Nvidia into the top five for the first time, driven by its leading position in the artificial intelligence (AI) silicon market.

STMicroelectronics climbed three positions to secure the No. 8 spot, a position it held in 2019. The company’s 2023 revenue increased by 7.7 percent, primarily fueled by a strong presence in the automotive segment.

Memory Revenue Faces Sharp Decline

Memory product revenue saw a sharp decline of 37 percent in 2023, marking the most significant decrease among all semiconductor market segments. Weak demand and excess channel inventory, particularly in the first half of the year, impacted smartphones, PCs, and servers, the major segments for DRAM and NAND.

DRAM revenue declined by 38.5 percent in 2023, totaling $48.4 billion.

NAND flash revenue experienced a decrease of 37.5 percent, amounting to $36.2 billion.

Nonmemory Revenue Witnesses 3 percent Decline

Nonmemory revenue exhibited a more resilient performance, declining by 3 percent in 2023. The segment faced challenges due to weaker demand and excess channel inventory throughout the year.

Unlike memory vendors, non-memory vendors experienced a relatively stable pricing environment in 2023. The demand for non-memory semiconductors in AI applications drove growth, with the automotive sector, especially electric vehicles, and the defense and aerospace industries outperforming other application segments.