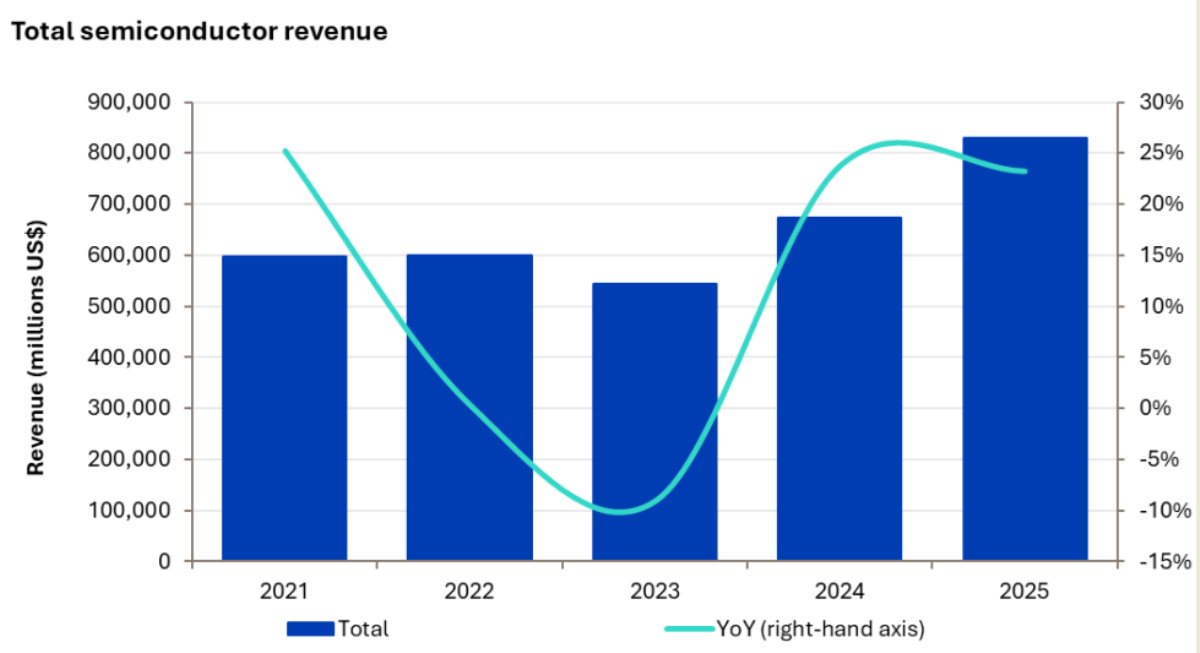

The global semiconductor industry reached a major milestone in 2025, surpassing $830 billion in revenue, driven by surging demand for artificial intelligence (AI), memory chips, and expanding growth across multiple segments, according to analysis from Omdia.

AI demand accelerates semiconductor growth

The rapid adoption of AI technologies has become the primary growth engine for the semiconductor market. Demand for AI infrastructure, including data center processors, GPUs, and high-bandwidth memory, has significantly increased chip consumption across industries.

AI-driven workloads, particularly in cloud computing and enterprise applications, are pushing the need for advanced chips, resulting in higher production volumes and rising prices for memory and logic components.

Record-breaking revenue and strong momentum

The semiconductor industry recorded unprecedented growth in 2025, with quarterly revenues crossing $200 billion for the first time. Total annual revenue is estimated to exceed $800 billion, representing nearly 20 percent growth compared to 2024.

This surge highlights the sector’s resilience and its critical role in powering modern technologies, from AI systems to consumer electronics and connected devices.

Growth expands beyond AI and memory

While AI and memory chips continue to lead the market, a key shift in 2025 is the broader contribution from other semiconductor segments.

Unlike 2024, where growth was concentrated among a few players and categories, 2025 saw strong performance across nearly all semiconductor segments. Even excluding major AI-driven companies and memory products, the rest of the market still delivered solid growth of around 9 percent.

This indicates a more balanced and sustainable industry expansion.

Memory and data center segments lead the surge

Memory technologies such as DRAM and NAND have seen exceptional demand due to AI inference and training workloads. At the same time, computing and data storage segments are emerging as dominant revenue contributors, fueled by hyperscale data center investments and AI infrastructure expansion.

Rising memory prices and strong demand for high-performance chips are further boosting overall market value.

Industry outlook remains strong

The semiconductor market is expected to maintain its growth trajectory, with projections indicating continued expansion into 2026 and beyond. Increasing investments in AI, cloud computing, IoT, and next-generation technologies will sustain demand for advanced chips.

However, challenges such as supply chain adjustments, pricing volatility, and rising manufacturing costs may influence future growth dynamics.

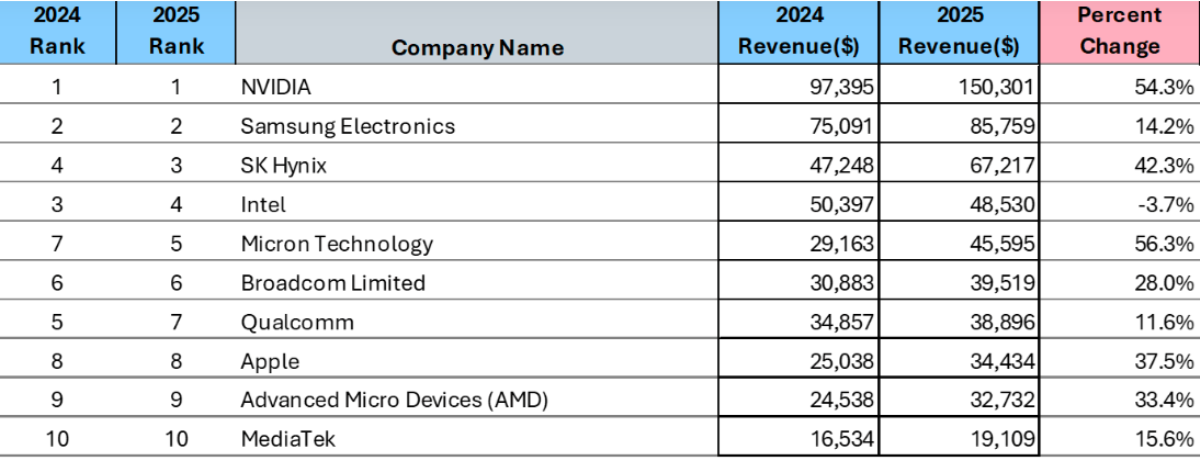

Top semiconductor companies see strong revenue growth in 2025 led by AI and memory demand

The global semiconductor industry in 2025 experienced a significant shift in revenue dynamics compared to 2024, with most leading companies posting strong growth driven by artificial intelligence, memory demand, and data center expansion.

NVIDIA maintained its top position, recording a sharp increase in revenue from $97.4 billion in 2024 to $150.3 billion in 2025, reflecting a 54.3 percent growth. This surge underscores its leadership in AI GPUs and its central role in powering next-generation computing workloads.

Samsung Electronics remained in second place, with revenue rising from $75.1 billion to $85.8 billion, representing a 14.2 percent increase. The growth was supported by steady recovery in the memory segment, although at a more moderate pace compared to AI-focused players.

SK Hynix climbed to third position, posting a strong 42.3 percent growth as revenue increased from $47.2 billion in 2024 to $67.2 billion in 2025. The company benefited significantly from demand for high-bandwidth memory used in AI applications.

Intel slipped to fourth place and was the only company among the top tier to record a decline, with revenue falling from $50.4 billion to $48.5 billion, a drop of 3.7 percent, highlighting ongoing competitive and market challenges.

Micron Technology delivered one of the strongest performances, with revenue surging 56.3 percent from $29.2 billion to $45.6 billion, driven by memory price recovery and AI-related demand.

Broadcom reported solid growth, with revenue increasing from $30.9 billion to $39.5 billion, up 28 percent, supported by strong demand in networking and infrastructure solutions.

Qualcomm recorded moderate growth of 11.6 percent, with revenue rising from $34.9 billion to $38.9 billion, reflecting stable performance in mobile and connectivity markets.

Apple moved up in semiconductor rankings with revenue increasing from $25.0 billion to $34.4 billion, marking a 37.5 percent rise, driven by its expanding in-house chip ecosystem.

Advanced Micro Devices also posted strong gains, with revenue growing 33.4 percent from $24.5 billion to $32.7 billion, fueled by demand for high-performance computing and AI processors.

MediaTek retained its position in the top 10, with revenue increasing from $16.5 billion to $19.1 billion, representing a 15.6 percent growth supported by smartphone and consumer electronics demand.

Overall, the comparison between 2024 and 2025 highlights a clear trend of AI-driven growth reshaping the semiconductor landscape. Companies with strong positions in AI, memory, and data center technologies significantly outperformed others, while most players benefited from broader market recovery, pushing the industry into a new phase of expansion.

Conclusion

The semiconductor industry’s rise beyond $830 billion in 2025 marks a pivotal moment, driven by AI adoption and widespread demand across sectors. With growth no longer limited to a few segments, the industry is entering a more balanced phase, positioning itself as the backbone of the global digital economy.

BABURAJAN KIZHAKEDATH