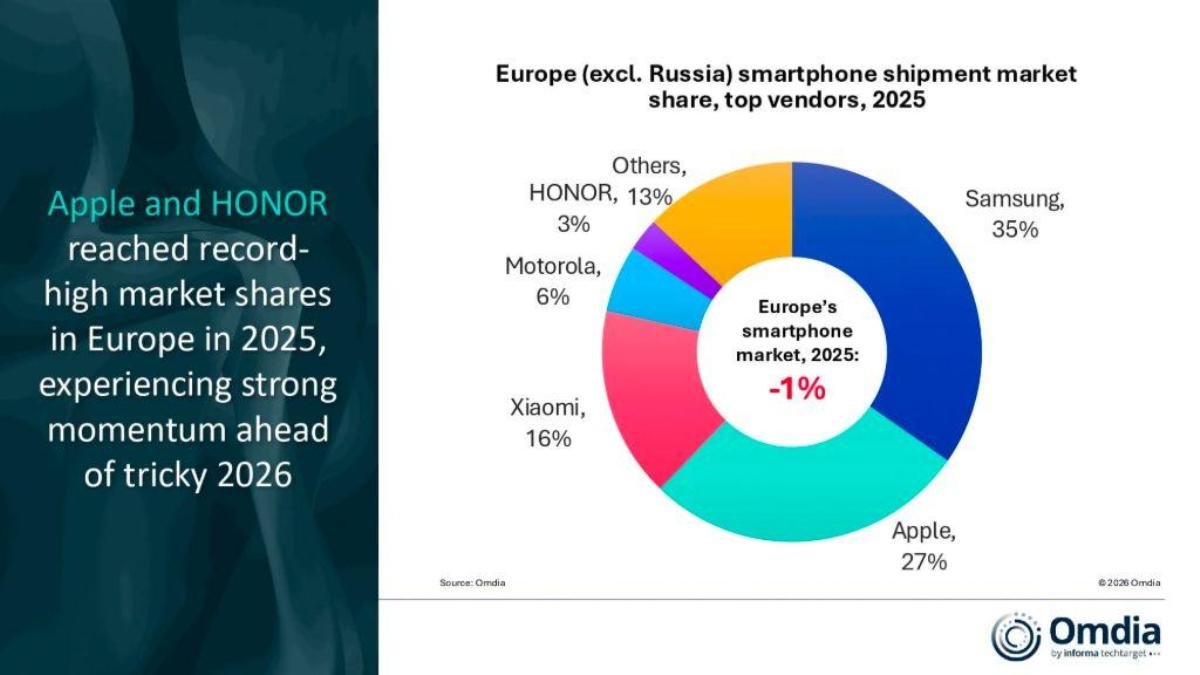

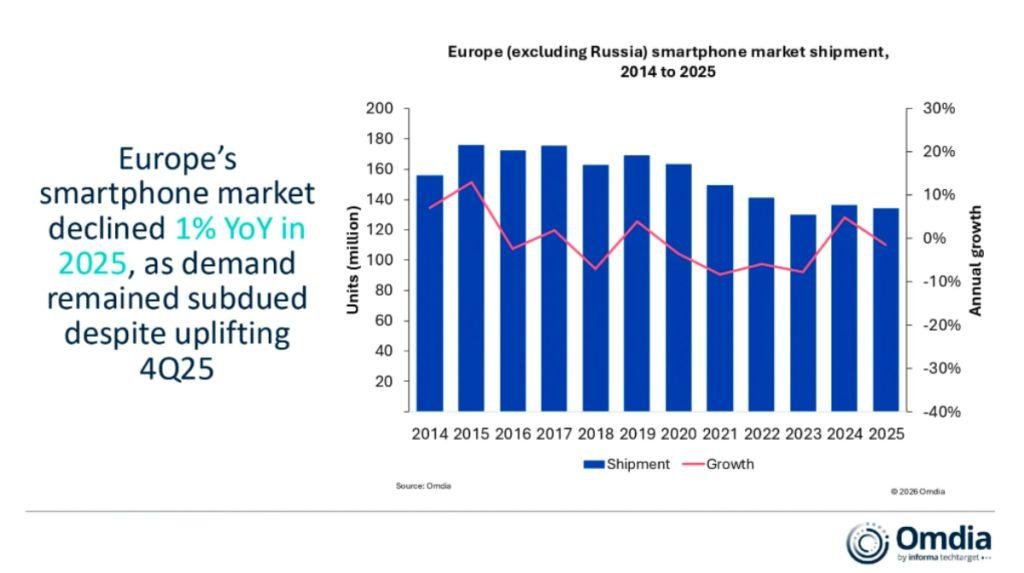

The European smartphone market declined 1 percent in 2025 to 134.2 million units due to subdued consumer demand and new regulatory requirements around eco-design and USB-C charging, Runar Bjorhovde, Senior Analyst at Omdia, said.

Europe accounted for 10.8 percent of global smartphone shipments in 2025, underlining its importance as a premium-heavy yet highly competitive region for leading vendors, Omdia report said.

Samsung Retains Leadership Despite Slow Start

Samsung Electronics remained Europe’s largest smartphone vendor in 2025, with shipments marginally increasing to 46.6 million units.

Samsung experienced a slow first half of 2025 due to the absence of the Galaxy A0x series. However, the company staged a strong comeback in the second half of the year. Growth was supported by a discounted version of the Samsung Galaxy A16 and robust demand for the Samsung Galaxy A56, which emerged as the top-selling smartphone model in Europe in 2025.

Samsung’s portfolio across price bands and strong channel presence helped it navigate regulatory changes and soft demand conditions.

Apple Achieves Record Market Share in Europe

Apple recorded 6 percent shipment growth to 36.9 million units in 2025, reaching a record-high 27 percent market share in Europe.

The growth was driven by strong iPhone refresh demand from both consumers and enterprises. Key contributors included the iPhone 16, the Pro Max versions of iPhone 17 and iPhone 16, as well as the iPhone 16e.

The iPhone 16e was among Apple’s top-shipping models in Europe, supported by the discontinuation of older models such as iPhone 14 in late 2024 due to new USB-C regulations. Compared to other global markets, Europe saw particularly strong uptake of the iPhone 16e as customers upgraded from legacy devices.

Xiaomi Holds Third Position Amid Slight Decline

Xiaomi maintained its third-place ranking with a 16 percent market share, despite a 1 percent decline in shipments to 21.8 million units.

The vendor continued to rely heavily on its budget-friendly Redmi series. Towards the end of 2025, Xiaomi expanded its overseas ‘new retail strategy’ into Europe, opening several Xiaomi Stores and broadening its ecosystem portfolio. This strategy aims to deepen brand engagement and strengthen its omnichannel presence in key European markets.

Motorola and HONOR Show Mixed Fortunes

Motorola remained fourth in Europe, although shipments declined 5 percent to 7.7 million units. The company faced subdued demand in the first half of 2025 but rebounded in the second half, achieving double-digit growth in the fourth quarter. Growth was supported by strong performance in Poland, Italy, Spain and the UK.

HONOR entered Europe’s top five for the first time, growing 4 percent to 3.8 million units. Its growth was primarily driven by the affordable X-series. HONOR’s increased focus on volume and channel partnerships is aimed at building a stronger foundation for its premium ambitions in the region.

Scale Becomes Critical in Competitive Market

Runar Bjorhovde noted that Europe’s five largest smartphone vendors continued to gain combined share in 2025, highlighting the importance of scale for long-term success.

Despite the shift toward larger players, intense channel competition remains across European markets. Retail and operator partners are increasingly open to introducing new vendors with differentiated products and brands. Vendors such as vivo, Nothing and Fairphone recorded high double-digit growth in 2025, demonstrating that strong differentiation can create opportunities even in a mature market.

2026 Outlook: Memory Pricing and Supply Risks

Looking ahead to 2026, concerns around rising memory pricing could create fresh challenges for smartphone vendors in Europe. The key question is which vendors will prioritize Europe if faced with price increases or supply shortages.

Omdia expects the largest vendors to demonstrate greater resilience due to their scale and broader price-band coverage. However, scaling a smartphone business in Europe remains gradual and investment-intensive. With a large premium segment and a relatively less price-sensitive mass market, Europe continues to be strategically attractive for global smartphone brands over the long term.

SHAFANA FAZAL