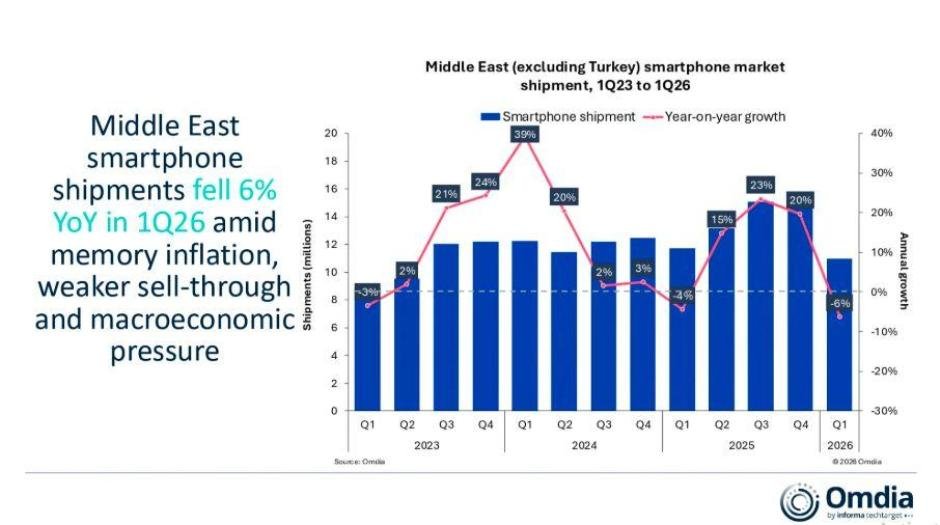

The Middle East smartphone market excluding Turkey declined 6 percent year-over-year to 11 million units in the first quarter of 2026, according to new data from Omdia. The regional smartphone industry faced mounting pressure from weaker consumer demand, rising device prices, geopolitical instability, and supply-chain disruptions despite aggressive Ramadan and Eid retail campaigns.

Omdia said smartphone vendors frontloaded inventory ahead of Ramadan and launched several new models across the region, but weaker retail sell-through and cautious consumer spending limited overall replacement demand during the quarter, Omdia report said.

Rising Smartphone Prices Push Regional ASP to Record $450

Persistent global memory cost inflation significantly increased smartphone prices across both new and existing portfolios during Q1 2026. Vendors implemented broad pricing revisions throughout the region, driving average selling prices (ASP) to a record $450, representing a 15 percent year-over-year increase.

Manish Pravinkumar said smartphone vendors entered 2026 facing rising cost pressures, softer low-end demand, and growing geopolitical uncertainty.

According to Omdia, affordability challenges particularly impacted entry-level and mid-range smartphone demand, while premium devices continued to show greater resilience across wealthier Gulf markets.

Saudi Arabia Smartphone Market Declines 3 Percent

Saudi Arabia, the region’s largest smartphone market, recorded a 3 percent year-over-year decline during Q1 2026.

Omdia attributed the decline to softer replacement demand and ongoing inventory normalization across retail channels, which offset the seasonal sales boost generated by Ramadan and Eid promotions. Consumer spending also remained cautious amid broader geopolitical concerns and rising living costs.

UAE Smartphone Market Grows 1 Percent on Premium Demand

The United Arab Emirates achieved modest 1 percent growth during the quarter, supported by resilient premium smartphone demand and continued flagship device launches.

Strong local consumption helped sustain sales momentum, although softer tourism activity toward the end of the quarter reduced discretionary spending and retail traffic in some segments.

Kuwait Stable as Hala Shopping Festival Supports Sales

Kuwait maintained relatively stable smartphone demand during Q1 2026, supported by seasonal retail activity linked to the February Hala Shopping Festival.

Vendors used the festival period to stimulate replacement demand and reduce inventory levels, particularly within premium and upper mid-range smartphone categories.

Iraq Smartphone Shipments Drop 18 Percent

Iraq experienced the sharpest decline among major regional markets, with smartphone shipments falling 18 percent year-over-year.

Omdia said currency depreciation, higher import taxes on electronics, and geopolitical uncertainty significantly weakened consumer affordability and retail demand. Rising import costs also disrupted channel inventory planning and reduced promotional activity across formal retail channels.

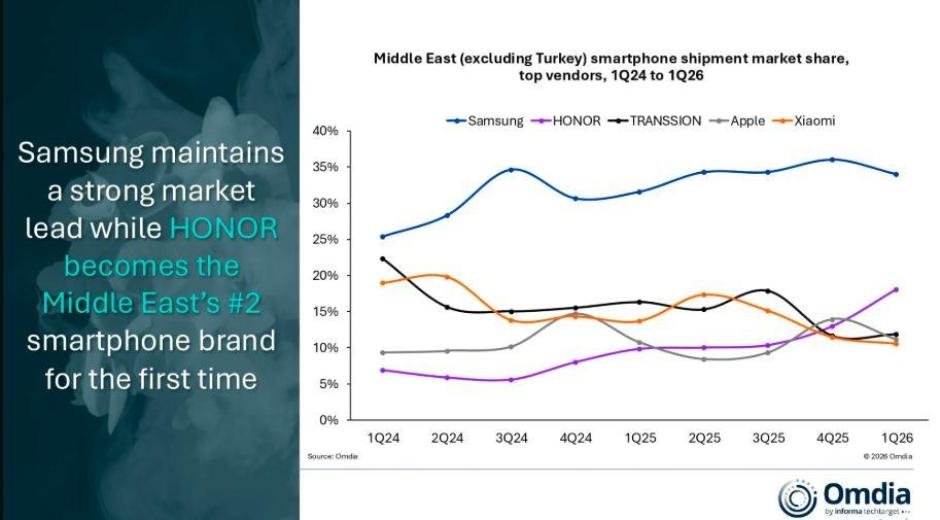

Samsung Extends Market Leadership While HONOR Surges

Samsung Electronics retained its leadership position in the Middle East smartphone market with a 34 percent market share during Q1 2026.

The company strengthened its position through strong shipments of the Galaxy S26 series alongside refreshed A-series smartphones.

HONOR became the region’s second-largest smartphone vendor for the first time, recording 73 percent year-over-year growth. Omdia attributed HONOR’s rapid expansion to improved retail execution, broader distribution, and strengthening brand perception across Gulf markets.

Meanwhile, Xiaomi and TRANSSION faced increasing pressure within entry-level segments as affordability constraints weakened replacement demand.

Apple continued to benefit from resilient premium demand, with the iPhone 17 Pro Max emerging as one of the region’s top-shipping smartphone models during the quarter.

Omdia Forecasts 22 Percent Market Decline in 2026

Omdia expects the Middle East smartphone market excluding Turkey to decline 22 percent during 2026 as rising prices, selective supply allocation, and macroeconomic uncertainty continue affecting regional demand.

The research firm said vendors are likely to encounter a more difficult operating environment during the remainder of 2026 due to higher smartphone prices and uneven consumer confidence.

Lower-income Gulf markets and value-conscious economies such as Iraq are expected to face prolonged replacement cycles as affordability deteriorates further. At the same time, premium-focused Gulf markets are also projected to see shipment declines, although brands are expected to maintain focus on flagship devices through financing offers, trade-in programs, and premium retail campaigns.

Omdia also warned that rising geopolitical tensions and potential disruptions to regional logistics routes could create additional pressure on smartphone pricing, supply availability, and channel operations throughout late 2026.

BABURAJAN KIZHAKEDATH