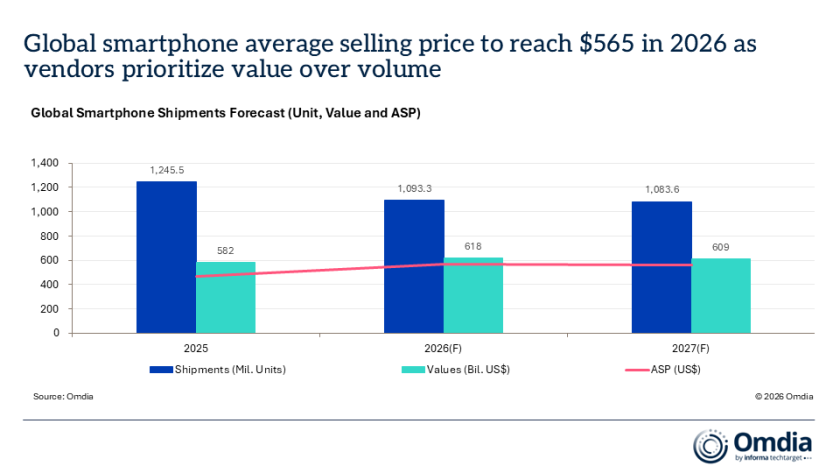

The global smartphone industry is undergoing a major structural transformation in 2026 as rising component costs, memory price inflation, and geopolitical uncertainty push manufacturers to prioritize premium devices over low-cost, high-volume models. According to Omdia, global smartphone shipments are forecast to decline by 12.2 percent year-on-year to 1.093 billion units in 2026, representing a loss of 152 million units compared with 2025.

Despite the decline in shipment volumes, the industry’s total market value is expected to grow by 6.1 percent in 2026, driven by unprecedented increases in smartphone pricing. Omdia forecasts the global average selling price (ASP) will rise from $467 in 2025 to $565 in 2026, an increase of $98 per device or 21 percent year-on-year. This represents the largest ASP increase ever recorded by the smartphone industry in both percentage and dollar terms.

The pricing surge is being fueled by escalating component costs across the supply chain. Average DRAM and NAND flash memory prices increased by more than 80 percent quarter-on-quarter during the first quarter of 2026, with further price increases recorded in the second quarter of 2026. While memory price growth is expected to slow to single-digit rates during the second half of 2026, costs are expected to remain structurally elevated, creating ongoing pressure on smartphone manufacturers.

To protect margins, smartphone vendors are actively reducing their dependence on entry-level devices and increasing the production share of mid-range and premium smartphones. Almost every major smartphone brand, with the exception of Apple, has increased retail prices for its latest-generation products to offset higher manufacturing expenses.

The impact of these price increases will vary significantly by region. Demand is expected to decline sharply across Africa, the Middle East, and Latin America, where consumers are highly dependent on affordable smartphones and are more sensitive to price increases. In contrast, developed markets with stronger premium smartphone adoption are expected to experience relatively mild shipment declines.

According to Omdia, some manufacturers are attempting to secure an early advantage by increasing component inventories to minimize the impact of future memory price hikes. The research firm expects the smartphone industry to move toward a stabilization phase during the second half of 2027 as DRAM and NAND pricing reaches a new equilibrium. During this period, manufacturers are expected to shift focus from supply chain pressures to broader strategic priorities.

Industry players are also preparing for a future readjustment phase when memory prices begin to decline. Omdia expects this phase to emerge in early 2028, supported by increased supply capacity. Vendors with lean operating structures are expected to benefit most from lower component prices, while companies holding excess inventories could face profitability challenges. However, any easing in memory prices could arrive earlier depending on the evolution of AI datacenter demand.

Beyond hardware sales, smartphone companies are increasingly relying on broader business ecosystems to improve resilience. Vendors are focusing on generating higher value from existing customers through cross-selling connected devices, promoting subscriptions and digital services, and increasing monetization opportunities across their installed user base.

The market slowdown is expected to continue into 2027, although at a much slower pace. Omdia forecasts smartphone shipments will decline by only 0.9 percent in 2027. Even as memory costs begin to moderate, the manufacturing economics of sub-$100 smartphones are expected to remain challenging, limiting the ability of vendors to reduce retail prices significantly. Looking further ahead, Omdia expects meaningful shipment growth to return in 2028. Major global smartphone brands are likely to remain cautious about expanding ultra-low-cost product portfolios, leaving the entry-level smartphone segment increasingly dominated by smaller regional and local manufacturers. As a result, premiumization, ecosystem expansion, and higher-margin services are expected to become the primary growth drivers for the global smartphone industry over the coming years.

BABURAJAN KIZHAKEDATH