Starlink has expanded to 155 countries, reaching more than 10 million subscribers and accounting for 97.1 percent of all satellite Speedtest samples globally in Q3 2025. Asia Pacific has emerged as a critical battleground for growth, shaped by infrastructure realities, regulatory frameworks, and evolving competition.

Oceania Sets the Benchmark for Performance

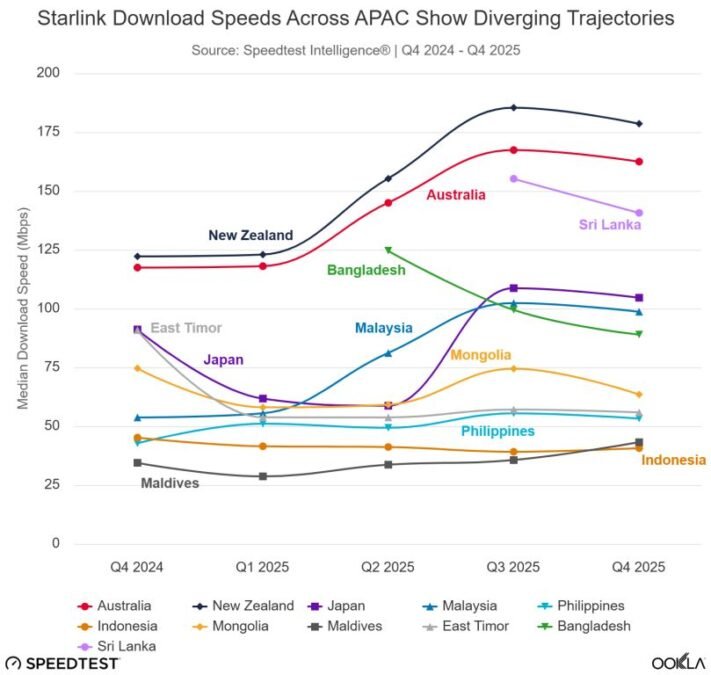

Oceania continues to lead the region across all key performance indicators. New Zealand recorded the lowest Starlink latency globally at 35 ms in Q4 2025, while Australia achieved median download speeds of 162.47 Mbps. Both markets launched in April 2021 and benefit from dense ground-station infrastructure, which directly enhances service quality.

Results highlight a core principle of low Earth orbit broadband: proximity to gateway infrastructure significantly improves latency and speed, enabling performance comparable to terrestrial broadband, according to Ookla’s 2025 Global Satellite Broadband Performance Report.

Starlink’s speed performance across Asia Pacific shows clear divergence based on market maturity, infrastructure density, and network load. Mature markets such as Australia and New Zealand consistently deliver the highest speeds in the region, supported by dense ground-station networks. Australia recorded median download speeds of 162.47 Mbps in Q4 2025, while New Zealand maintained similarly strong performance alongside global-leading latency.

Performance across Southeast Asia is more uneven. Malaysia showed significant improvement, with speeds rising from 53.74 Mbps in Q4 2024 to 98.68 Mbps in Q4 2025, reflecting network optimization and easing congestion. Philippines recorded more modest gains, increasing from 42.68 Mbps to 53.27 Mbps, indicating gradual capacity expansion.

Indonesia presents a contrasting trend, where speeds declined from 45.16 Mbps to 40.69 Mbps despite growing user demand. This suggests that network usage is outpacing infrastructure expansion, particularly in high-demand areas.

In East Asia, Japan experienced fluctuations, with speeds dropping early in 2025 before recovering to 104.60 Mbps by Q4, a pattern consistent with demand surges followed by capacity upgrades.

Regulation Defines Market Entry Across Asia Pacific

Demand alone does not determine where Starlink operates in Asia Pacific. Regulatory conditions play the decisive role. Governments across the region have required a combination of security provisions, infrastructure commitments, and foreign ownership adjustments before granting licenses.

Markets such as Bangladesh and Sri Lanka required legislative reforms to enable satellite services. India, despite securing regulatory approvals in July 2025, remains a pending launch due to unresolved spectrum pricing and security clearance requirements.

This pattern underscores that Starlink’s expansion is shaped less by technical feasibility and more by its ability to align with national sovereignty concerns, including data localization and lawful interception.

LEO Technology Reshapes Satellite Broadband Capabilities

Traditional satellite providers operating in medium Earth orbit and geostationary orbit have long served enterprise and government customers, but their high latency has limited consumer adoption. Providers such as Kacific have delivered wide coverage but with latency levels that restrict real-time applications.

Starlink’s low Earth orbit constellation operates at approximately 550 km, dramatically reducing latency compared with GEO systems positioned up to 36,000 km above Earth. This shift enables use cases such as video conferencing, cloud computing, and online education, transforming satellite broadband from a last-resort solution into a viable alternative to fixed networks in many Asia Pacific markets.

Geography Drives Demand for Satellite Connectivity

Asia Pacific’s geography creates a strong structural case for satellite broadband. Countries like Philippines and Indonesia consist of thousands of islands, making nationwide fiber deployment economically impractical. Mongolia faces a different challenge, with vast rural areas and low population density limiting the reach of terrestrial infrastructure.

In these environments, satellite connectivity is not just an alternative but often the only feasible broadband solution for remote communities, maritime operations, and rural enterprises.

Pricing and Affordability Vary Widely by Market

Starlink’s pricing across Asia Pacific remains relatively consistent in absolute terms but varies significantly in affordability. Monthly plans range from about $45 in Australia to around $68 in the Philippines. However, income disparities mean the same pricing represents a much larger share of household income in developing economies.

In markets like the Philippines, where average household internet spending is significantly lower, Starlink remains a premium offering. This has limited its adoption primarily to remote areas and enterprise use cases, despite strong underlying demand.

Performance Divergence Reflects Infrastructure Gaps

Performance data across Asia Pacific reveals a region with wide disparities. Mature markets such as Australia and New Zealand consistently deliver high speeds and low latency, while emerging markets show mixed results depending on infrastructure availability.

Latency is particularly sensitive to gateway proximity. Markets with local ground stations, including Australia, New Zealand, and Bangladesh, recorded latency as low as 35–36 ms in Q4 2025. In contrast, markets relying on distant gateways, such as East Timor and the Maldives, reported latency exceeding 100 ms.

This highlights infrastructure investment as a critical factor influencing service quality and a key negotiation point for governments licensing satellite services.

Competitive Landscape Intensifies with New Entrants

Starlink currently holds a dominant position in Asia Pacific, but competition is increasing. Amazon’s Project Kuiper is set to play a major role, particularly through its agreement to transition Australia’s Sky Muster customers to LEO services from 2026.

Meanwhile, China is advancing its own LEO constellations, including Qianfan, which is expanding through partnerships with regional telecom operators. This model allows it to bypass some of the regulatory challenges faced by Starlink, offering governments an alternative aligned with local ownership preferences.

South Asia Emerges as a High-Growth Region

South Asia represents the newest phase of Starlink’s regional expansion. Bangladesh has demonstrated strong early performance, achieving 88.95 Mbps median download speeds and 35 ms latency within months of launch. Sri Lanka has also delivered robust results following regulatory reforms, positioning satellite broadband as a complement to existing infrastructure.

India remains the largest untapped opportunity. With partnerships already in place with major telecom operators, even a partial rollout would significantly expand Starlink’s footprint in the region.

The Next Phase of Starlink in Asia Pacific

As Starlink moves into 2026, its growth in Asia Pacific will be shaped by a combination of regulatory negotiations, infrastructure deployment, and competitive pressure. Emerging capabilities such as direct-to-device connectivity are expected to further influence licensing discussions, extending the role of satellite networks into mobile communications.

The region’s diversity ensures that no single strategy will apply across all markets. Instead, Starlink’s success will depend on its ability to adapt to local regulatory conditions, invest in ground infrastructure, and position its services within increasingly competitive broadband ecosystems.

SHAFANA FAZAL