Nokia revealed that its core networks portfolio has been ranked #1 for competitiveness in Omdia’s “Market Landscape: Core Vendors – 2025” report.

The ranking reflects Nokia’s strengths in cloud-native readiness, automation, core as a service, breadth of portfolio, and its leadership in 5G Standalone core deals with CSPs, Raghav Sahgal, President, Cloud and Network Services, Nokia, said.

Roberto Kompany, Principal Analyst, Mobile Infrastructure, Omdia, has highlighted Nokia’s ability to align with future market needs, noting its top position in areas critical to operators’ success.

Nokia currently has 125 CSP customers for its 5G Standalone core, with 54 already live, including recent wins with Ooredoo Qatar and Telefonica Spain. The company said the recognition validates its multi-cloud strategy, innovation, and growing customer base across packet core, IMS voice, and subscriber data management.

Nokia’s cloud-native portfolio enables operators to run 2G through 5G and IMS cores on cloud-native functions, covering packet core, data management, voice, analytics, charging, signaling, exposure, cloud infrastructure, orchestration, and services. The approach allows operators to deploy entire cores on unified cloud platforms, reducing cost and complexity while accelerating secure service rollouts.

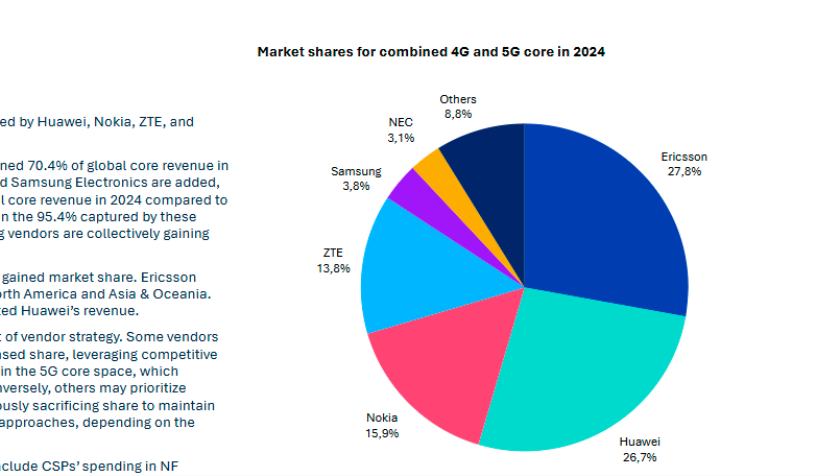

The 4G and 5G core market remains highly concentrated, with five vendors holding an 88 percent combined share in 2024, down from 95.4 percent in 2020, and the top three accounting for 70.4 percent of revenue. Competition is intensifying around next-generation 5G core, making leadership positioning critical. Omdia’s 2025 assessment categorizes 11 vendors into three groups based on business performance and portfolio.

Huawei, Ericsson, Nokia, and ZTE are the market leaders, while Mavenir, NEC, and Oracle are major challengers whose positions slipped compared to last year. Samsung, along with IPLOOK, ENEA, and new entrant Viettel, are in the upcoming vendors group, though their smaller portfolios and limited market reach make benchmarking them more complex. Vendors’ relative scores reflect not a decline in capabilities but rather the pace of improvements compared to peers, highlighting that differentiation is increasingly driven by innovation speed and portfolio expansion.

Ericsson leads in business performance with strong market share gains, more 5G deals with CSPs, and an increased number of new logos in 2025. It ranks second in portfolio strength, excelling in cloud native readiness, automation, policy and charging, and AI/ML-driven analytics.

Huawei is second in business performance, leading in new customer wins and 5G deals while maintaining solid portfolio strength, particularly in signaling, policy and charging, and AI/ML, though it lags in cloud native readiness and core-as-a-service.

Nokia leads in portfolio capabilities with strong performance in cloud native readiness, automation, and core-as-a-service, while ranking third in business performance due to a lower share of 5G core revenue despite strong CSP deal wins and market share growth. ZTE continues to strengthen its position, improving in both business performance and portfolio, winning more 5G deals and customers, with strong leadership in analytics, AI/ML, and a solid position in core-as-a-service.

Mavenir enhanced its portfolio in 2025 with strong maturity in cloud native NFs, ranking second in cloud native readiness and third in automation, but its business performance weakened due to fewer 5G CSP deals compared to rivals.

Oracle strengthened its portfolio, leading in signaling and showing strengths in automation and policy and charging, but its business performance slipped with fewer 5G deals and new logos. Its 5G core strategy is selective, focusing on routing, policy, and analytics, with reliance on partnerships for key functions like packet core, while offering its 5G core via Oracle Cloud and seeking growth in core-as-a-service.

NEC improved its business performance, benefiting from a higher 5G share of total core revenue and new CSP logos, but it remains constrained by fewer 5G deals and a strong focus on the Japanese market. Its strategy leans on enterprise opportunities and core-as-a-service, though it still needs to strengthen signaling and expand its NF portfolio, particularly in areas like NWDAF.

Samsung improved its portfolio score in 2025 but remains limited to packet core NFs, lacking signaling, policy, charging, NWDAF, and core-as-a-service offerings, with its absence from several regions constraining revenue opportunities. It could move into the major challengers category if it expands market share and wins more 5G CSP deals.

IPLOOK strengthened both business performance and portfolio scores, offering 4G and 5G RAN and core solutions with strengths in cloud native readiness, and to a lesser extent, automation and core-as-a-service, though its main focus remains private networks.

ENEA improved in both dimensions, gaining more 5G CSP deals and ranking second in analytics and AI/ML while maintaining strengths in cloud native readiness and automation, though it provides only a limited set of NFs including PCF, SDM, UDR, and SEPP. Viettel, a new entrant, scored well in portfolio within its limited scope, developing packet core, NRF, and NSSF, along with ongoing work on NEF, NWDAF, and a converged charging system; it will improve further once it secures 5G CSP deals outside its own group.

In 2024, Ericsson led the global core revenue market, followed by Huawei, Nokia, ZTE, and Samsung, with the top five together holding 88 percent share, slightly higher than 87.6 percent in 2023 but down from 95.4 percent in 2020 as smaller vendors continue to gain ground. Ericsson, Huawei, and Nokia collectively captured 70.4 percent of global revenue, almost unchanged from 2023. Ericsson, Nokia, and ZTE gained share, with Ericsson strengthening in North America and Asia & Oceania, while Huawei’s revenue was hit by reduced CSP spending in China. Market share remains central to vendor strategies, with some players trading margins for growth by offering competitive pricing to secure 5G core deals, while others prioritize profitability over expansion, depending on region and deal structure. Ericsson held 27.8 percent market share, Huawei 26.7 percent, Nokia 15.9 percent, ZTE 13.8 percent, Samsung 3.8 percent, NEC 3.1 percent, and other vendors 8.8 percent.

Baburajan Kizhakedath