The latest Canalys report has revealed the list of top 10 smartphone makers in 2024 and their growth strategies.

The global smartphone market experienced a 7 percent growth in 2024, reaching 1.22 billion units. In the last years, smartphone market fell.

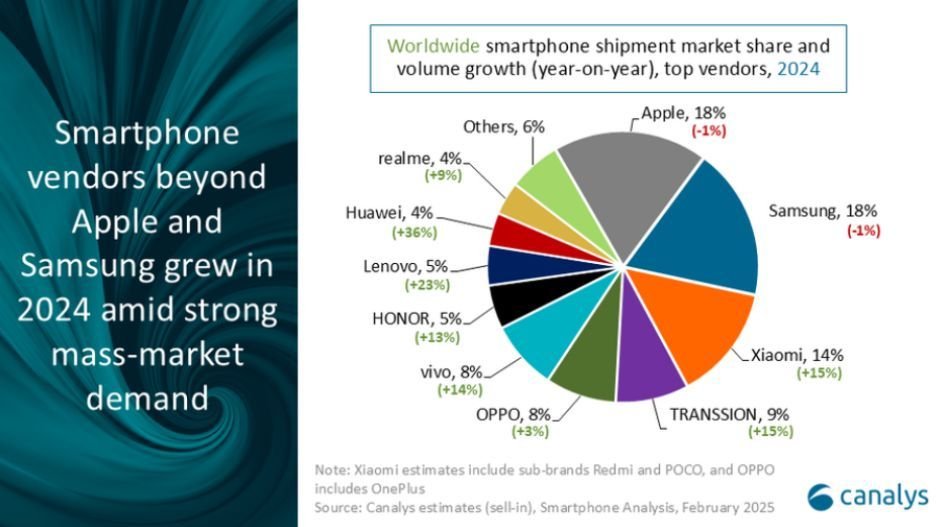

Apple (18 percent), Samsung (18 percent), Xiaomi (14 percent), Transsion (9 percent), Oppo (8 percent), Vivo (8 percent), Honor (5 percent), Lenovo (5 percent), Huawei (4 percent), and Realme (4 percent) are the top selling smartphone brands in 2024.

Strategies of smartphone makers?

Apple has maintained its leading position due to emerging market growth and stable performance in North America and Europe, offsetting challenges in Mainland China, despite a 1 percent decline in shipments to 225.9 million units.

Samsung, in second place, also saw a 1 percent decline in shipments to 222.9 million units but maintained profitability by focusing on high-end models.

Xiaomi strengthened its position as the third-largest vendor with a 15 percent growth in shipments to 168.6 million units, driven by strong momentum in Mainland China and emerging markets.

TRANSSION climbed to fourth place for the first time with a 15 percent increase in shipments to 106.7 million units.

OPPO (including OnePlus) ranked fifth with a 3 percent increase to 103.6 million units.

Vendors have capitalized on a surge in mass-market demand, driven by a refresh cycle of pandemic-era smartphones and channel replenishments. The open-market channel has been a key focus, with a strong emphasis on value-for-money products. However, the aggressive push for volume growth has led to the risk of margin erosion, prompting vendors to cut fixed costs and optimize resource allocation.

The market recovery has been evident in both emerging and mature economies, with China growing at 4 percent, North America at 1 percent, and Europe at 3 percent. Strong promotional strategies, including discounts, trade-ins, and device bundles, have played a crucial role in boosting demand.

Apple and Samsung have remained resilient due to the ongoing premiumization trend. Consumers continue to opt for higher-end flagship models, leading to a notable 11 percent increase in shipments of the iPhone 16 Pro and Pro Max compared to their predecessors, reaching over 55 million units.

Samsung’s S-series achieved its highest volume since 2019, with a strong bias toward the Ultra model. To sustain S-series growth, Samsung aims to enhance AI-powered experiences, including bundling the Galaxy S25 with a Gemini Advanced subscription. Additionally, Samsung seeks to transition mid-range A-series users to standard and plus flagship models to drive premium segment growth.

Vendors face a challenging 2025 due to global and regional complexities. Growth in emerging markets, which has been the industry’s primary driver, is beginning to plateau as saturation sets in. Balancing short-term performance with effective inventory management and long-term strategic investments will be crucial. Economic fluctuations, potential US tariffs, and compliance regulations add further unpredictability. However, opportunities such as increasing premiumization, China’s subsidy initiatives, and evolving financing models present avenues for growth.

Baburajan Kizhakedath