The global smartphone market in Q1 2026 has entered a decisive strategic phase, with vendors rapidly reshaping pricing, portfolios, and market focus to navigate rising component costs and weakening demand.

According to Omdia report, the market grew by 1 percent year on year, supported by channel inventory frontloading.

Omdia’s Sanyam Chaurasia said: “Smartphone vendors have little choice but to raise prices as cost pressures intensify. While price increases are happening across the industry, the impact is not uniform.”

IDC report noted 4.1 percent decline in shipments to 289.7 million units, signaling underlying demand weakness.

IDC’s Nabila Popal said: “The smartphone market has entered one of its most challenging periods, driven by acute memory supply constraints that are directly impacting both shipments and demand.”

Pricing power becomes the key differentiator

A central theme across vendors is pricing strategy. With mobile DRAM and NAND prices surging nearly 90 percent quarter on quarter in Q1 and expected to rise another 30 percent in Q2, vendors are being forced to pass on costs.

However, pricing power varies widely. Apple has largely maintained stable pricing, while Samsung has adopted a selective pricing strategy across markets. In contrast, vendors such as Xiaomi and TRANSSION, with stronger exposure to entry-level segments, face margin pressure due to limited ability to increase prices.

Premium segment focus strengthens

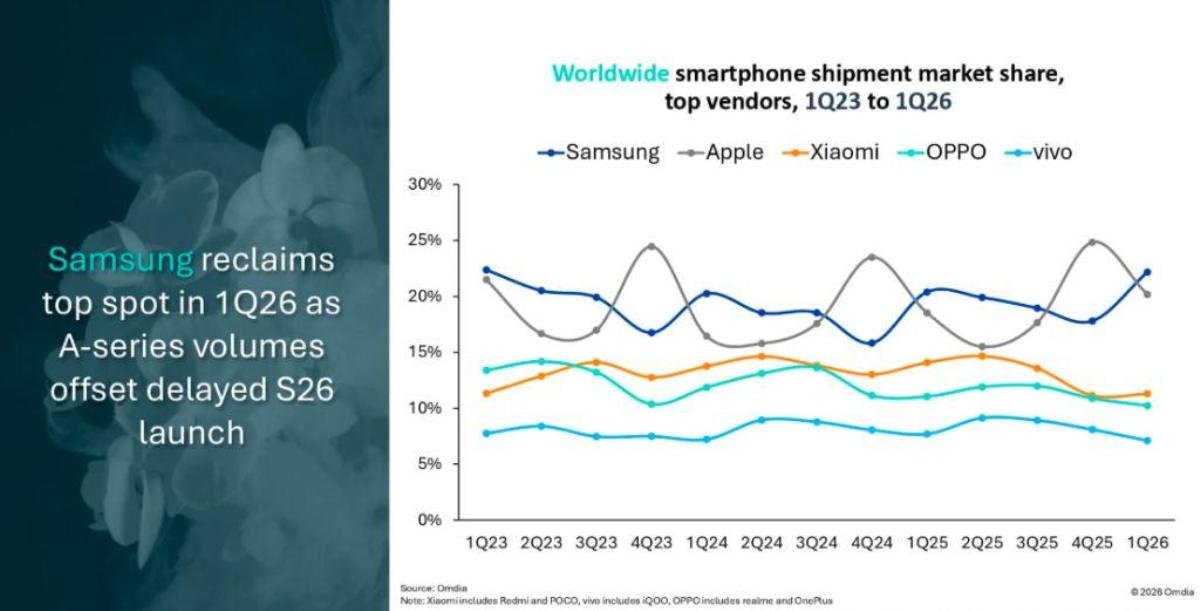

Samsung and Apple continue to outperform by leveraging their dominance in the premium segment. Strong demand for flagship devices such as the Galaxy S26 Ultra and iPhone 17 series supported shipment growth of 3.6 percent and 3.3 percent respectively. Their scale and stronger relationships with memory suppliers provide better insulation from cost volatility, enabling them to protect margins while sustaining demand.

Portfolio optimization and cost control intensify

Android vendors are responding with tighter product portfolios, selective launches, and configuration adjustments. Strategies include reducing promotions, limiting channel incentives, and adopting “despecing” approaches to control bill-of-materials costs. Xiaomi, for instance, reduced shipments of older models to avoid aggressive price increases, while OPPO and vivo focused on balancing domestic strength with global challenges.

Geographic diversification and expansion strategies

Regional strategy is becoming critical. Huawei’s strong performance in China, supported by competitive pricing, and HONOR’s aggressive overseas expansion contributed to share gains outside the top five. Meanwhile, vendors are balancing between defending home markets and pursuing growth in regions such as Europe and emerging markets, where rising prices are beginning to impact demand significantly.

Channel and financing strategies gain importance

With higher retail prices creating demand friction, vendors are increasingly relying on financing options, trade-ins, and tighter channel pricing to sustain sales. Inventory build-up by channel partners has temporarily supported shipments, but this is expected to delay rather than eliminate demand pressure in the coming quarters.

Outlook: margin protection over volume growth

Both Omdia and IDC highlight that 2026 will be a challenging year, with shipments expected to decline further as cost pressures intensify. Vendors are shifting focus from volume-driven growth to margin protection, premiumization, and operational efficiency. The industry is moving toward higher average selling prices, reduced low-end exposure, and a more disciplined approach to product and channel management.

As supply-side constraints, geopolitical risks, and pricing pressures converge, smartphone vendors are entering a phase where strategic execution across pricing, portfolio, and market positioning will determine long-term competitiveness.

BABURAJAN KIZHAKEDATH