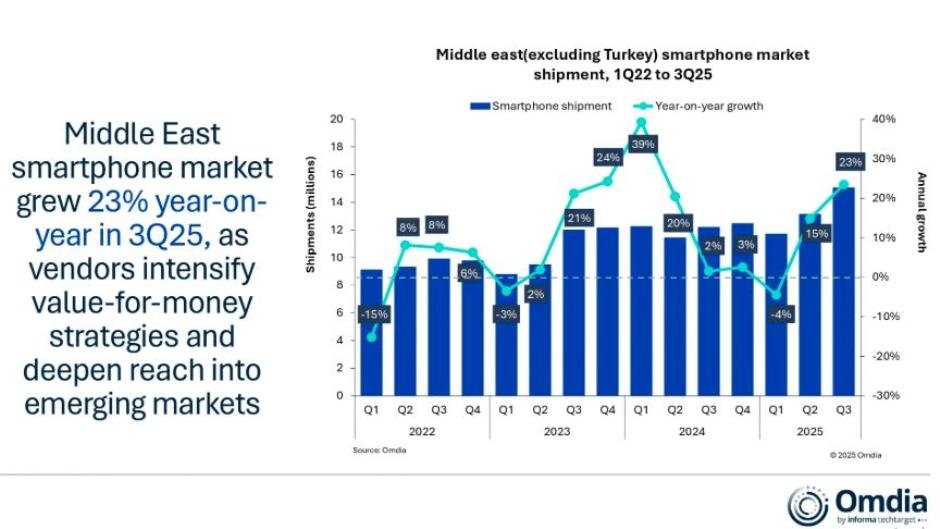

The Middle East smartphone market (excluding Turkey) witnessed a robust recovery in the third quarter of 2025 (3Q25), driven by growing demand for mid-tier 4G and affordable 5G devices.

According to Omdia report, smartphone shipments in the Middle East rose 23 percent year-on-year to 15.1 million units, signaling renewed consumer confidence and strategic vendor activity across the region.

1. Strong Overall Market Growth

The region saw a 23 percent increase in smartphone shipments in 3Q25, marking a strong rebound from previous quarters. Rising consumer upgrades from older or entry-level devices to mid-tier 4G and affordable 5G smartphones fueled this growth, Manish Pravinkumar, Principal Analyst at Omdia, said in the report.

2. Mass-Market Segment Drives Volume

Vendors focused on value-for-money devices, expanding their affordable 4G portfolios in emerging Middle Eastern markets. This strategy led to high-volume adoption and stronger market penetration in price-sensitive segments.

3. Country-Level Performance Variation

Saudi Arabia: Largest regional market recorded a 2 percent decline due to prolonged summer holidays and delayed upgrade cycles.

UAE: Grew 13 percent, boosted by retail promotions from Sharaf DG, Carrefour, Emax, Dubai Summer Surprises, and high-profile launches.

Iraq & Rest of Middle East: Exhibited strong momentum with 41 percent and 70 percent growth respectively, driven by intensified vendor activity, channel incentives, and distributor coordination.

4. ASP Softness Persists

Despite strong shipment growth, average selling prices (ASP) remained soft as vendors prioritized volume by expanding entry-level and affordable 5G offerings.

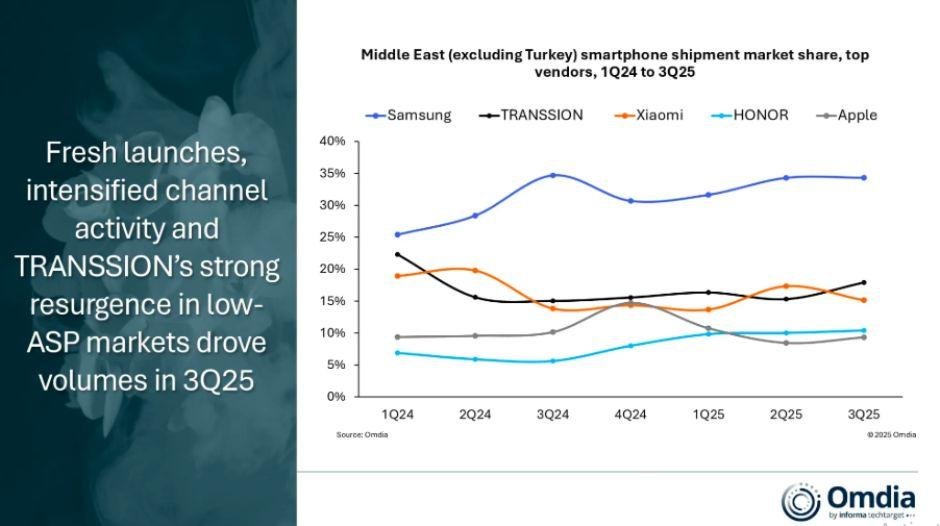

5. Samsung Retains Market Leadership

Samsung maintained its lead with 22 percent growth, supported by the Galaxy A17 4G/5G series and sustained performance of its high-volume A-series models.

6. TRANSSION Rebounds Strongly

TRANSSION recorded a 47 percent recovery, led by TECNO’s growing presence in lower-ASP markets and strong adoption among Asian and African expatriates in Gulf hubs.

7. Xiaomi Expands Direct-to-Consumer Engagement

Xiaomi delivered 35 percent growth by restructuring channel partnerships and increasing regional investments, including opening its first Dubai flagship store at Ibn Battuta Mall.

8. HONOR Achieves Highest Growth

HONOR posted 128 percent growth, driven by portfolio expansion, stronger operator and retail partnerships, and broader ecosystem integration.

9. Apple Returns to Double-Digit Growth

After six quarters of uneven performance, Apple grew 14 percent, led by strong early sell-through of the iPhone 17 series, reinforcing its premium segment leadership.

10. Market Outlook for 2026

Omdia forecasts Middle East smartphone growth to slow to 1 percent in 2026 due to rising component costs and supply constraints. Mid-to-premium segments, led by Apple and Samsung, are expected to remain resilient, while lower-ASP markets will require targeted promotions, trade-in programs, and financing options to sustain demand.

The 3Q25 rebound highlights the region’s strategic shift toward value-driven offerings and mid-to-premium upgrades. Vendors that optimize portfolios, strengthen channels, and focus on service differentiation are likely to benefit most from the market’s gradual recovery in 2026.

Baburajan Kizhakedath