Omdia’s latest report shows Latin America’s smartphone market returning to growth, rising 1 percent year-over-year in the third quarter of 2025 with shipments reaching 35.2 million units. This marks the Latin America region’s strongest quarterly performance since the fourth quarter of 2015, supported by resilient demand, improved economic conditions, and cautious inventory management across vendors and channels.

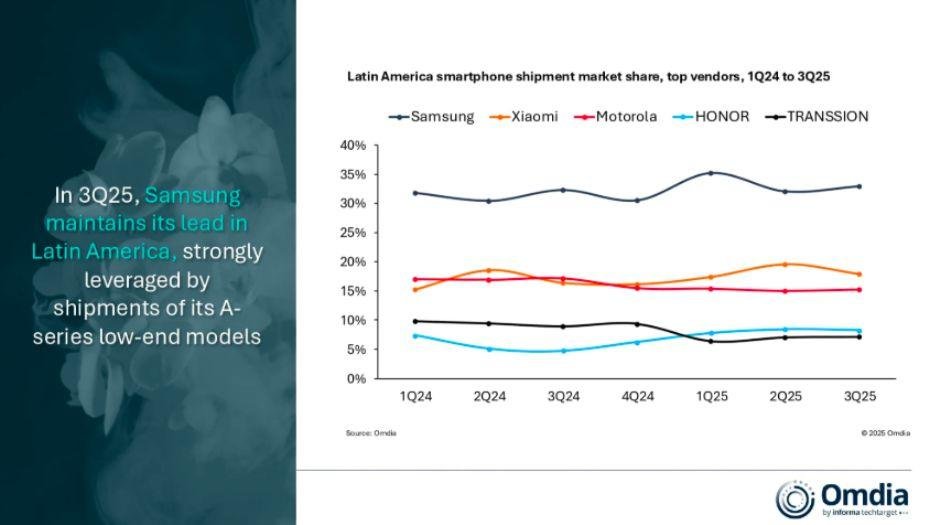

Samsung led the market with 11.6 million units and a 33 percent share, driven by strong performance of its low-end A-series models, which made up 68 percent of its shipments.

Xiaomi followed with 6.3 million units, capturing an 18 percent share.

Motorola ranked third but recorded its sixth consecutive quarterly decline with an 11 percent drop.

HONOR secured fourth place with 2.9 million units, achieving record shipments for the third straight quarter. Its growth was driven by momentum in the Caribbean, Colombia, and Ecuador, which now contribute more than 40 percent of its total volume.

TRANSSION completed the top five despite a 19 percent year-over-year decline.

The recovery in Latin America’s smartphone market was supported by expansion in key markets such as Brazil and Central America, along with rebounds in Chile, Colombia, and Ecuador. Brazil, which represents 29 percent of the region’s market with 10.3 million units (up 5 percent year-over-year), saw new players including realme, OPPO, HONOR, and Jovi (vivo) strengthen their presence through local production and partnerships with operators and retailers.

Conversely, Mexico, the second-largest market with 7.4 million units and a 21 percent share, declined 11 percent, marking its fourth consecutive quarter of contraction. Reduced shipments of sub-300 dollar devices due to conservative inventory strategies drove the slowdown.

Beyond Brazil, markets such as Central America and Ecuador continued their upward trajectory, supported by sustained demand for low-end smartphones. Colombia and Chile also showed recovery, aided by better economic indicators including easing inflation, rising investment, and improved consumer spending.

While overall regional shipments increased, the sub-300 dollar category, which accounts for 71 percent of all units, fell 2 percent year-to-date through the third quarter. The decline stems from ongoing inventory challenges, weaker consumer demand, and vendor strategies that increasingly prioritize higher average selling prices to improve financial sustainability.

This shift has propelled a surge in high-value devices. Shipments of smartphones priced above 500 dollars recorded a strong 20 percent year-to-date increase, contributing to an 8 percent rise in ASP during the quarter. Competition in the premium segment is intensifying, traditionally led by Apple and Samsung, as brands such as OPPO, Xiaomi, HONOR, vivo, realme, and Google in Mexico increase their investments to capture more share.

Miguel Angel Perez, Senior Analyst for Latin America at Omdia, said the rise in higher-value device shipments shows how manufacturers are working to maintain market presence and strengthen brand positioning as the low-end market becomes increasingly saturated. He said manufacturers with long-term ambitions need to focus on raising ASPs, improving ecosystem profitability, and building customer loyalty to secure sustainable financial performance.

Omdia expects the Latin American smartphone market to close 2025 flat compared to 2024, with 137.0 million units shipped. He warned that 2026 may present new challenges. Rising memory and storage costs could push up device prices, particularly in entry-level categories, slowing market momentum. He said manufacturers and retailers will need strategies including subsidies, margin optimization, bundling, and flexible financing to reduce the impact on consumers.

Baburajan Kizhakedath