The Indonesian smartphone market in 2025 and early 2026 remains one of Southeast Asia’s most competitive battlegrounds, defined by aggressive pricing strategies, tight market share gaps and rapidly evolving consumer buying patterns. Chinese smartphone vendors continue to dominate shipments, while South Korea’s Samsung stands as the only non-Chinese brand in the top tier.

Smartphone market share: A tightly contested race

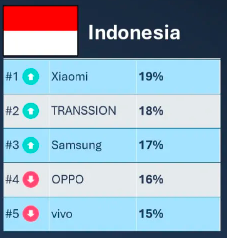

Indonesia’s smartphone landscape is marked by narrow margins separating the top five vendors.

Xiaomi – 19 percent

Xiaomi secured the number one position in 2025, driven by strong demand for value-focused, feature-rich smartphones across entry and mid-range segments.

Transsion – 18 percent

Backed by brands such as Tecno, Infinix and itel, Transsion expanded rapidly by targeting price-sensitive consumers and deepening offline retail penetration.

Samsung – 17 percent

Samsung maintained its leadership as the top non-Chinese vendor, leveraging its broad portfolio across premium Galaxy S models and mid-tier Galaxy A series devices.

OPPO – 16 percent

OPPO sustained strong momentum through offline distribution networks and camera-centric marketing targeting youth buyers.

vivo – 15 percent

vivo remained aggressive in the mid-range and entry-level 5G segments, appealing to first-time upgraders and younger demographics.

The gap between the top five brands is just 4 percentage points, highlighting intense competitive pressure in a market where pricing and distribution are critical success factors, according to the latest Omdia report.

By January 2026, market dynamics showed continued shifts, with Samsung holding 16.47 percent share and OPPO at 14.68 percent, while Xiaomi and vivo maintained double-digit positions. Transsion continued to dominate emerging and unclassified segments, accounting for more than 18.3 percent of shipments through ultra-affordable 5G devices priced below Rp3,000,000.

Vendor strategies: Value, ecosystem and pricing discipline

Indonesia has entered a “Value-First” smartphone era, where buying decisions are increasingly shaped by affordability, bundled data offers, software experience and ecosystem integration rather than pure hardware specifications.

Samsung’s dual-track approach

Samsung is executing a premium-plus-volume strategy. Flagship Galaxy S devices reinforce brand equity, while Galaxy A series smartphones drive shipment volumes. The company has maintained relatively flat pricing despite rising component costs, absorbing margin pressure to defend share. However, user concerns around OLED display issues and charging speeds could influence upgrade cycles.

Xiaomi’s ecosystem convergence

Xiaomi’s strategy centers on hardware-software convergence under its HyperOS platform. Devices such as its Redmi Note series remain volume drivers in the Rp4,000,000 to Rp5,000,000 band. However, rising component costs have pushed some flagship prices higher, while consumer feedback on pre-installed apps and advertising remains a friction point.

Transsion’s budget dominance

Transsion continues to win in entry-level and gaming-focused devices. Models under Infinix and Tecno brands offer high-refresh-rate displays and gaming chipsets at aggressive price points around Rp4,000,000. Yet, performance-related complaints such as overheating during extended gaming sessions reflect the technical challenges of balancing cost and durability in tropical climates.

OPPO and vivo adjust to cost inflation

OPPO and vivo are repositioning devices with differentiated features to justify higher prices amid memory cost inflation. Enhanced durability ratings, larger batteries and camera optimization are being emphasized to offset rising retail prices.

Buying patterns: 5G, bundles and price sensitivity

Indonesian consumers remain highly price-sensitive, with strong preference for:

Mid-range 5G smartphones under Rp5,000,000

Offline retail purchases supported by installment financing

Bundled data offers and streaming subscriptions

Social media and gaming optimized devices

The merger of XL Axiata and Smartfren into XLSMART, alongside aggressive 5G expansion by operators such as Telkomsel, is accelerating 5G handset adoption. Telco bundling programs offering hundreds of gigabytes of bonus data are increasingly influencing device purchase decisions.

Pricing pressure and the “Memory Winter”

A defining theme of early 2026 is sharp increases in DRAM and NAND flash contract prices, driven by supply diversion toward AI data centers. This has forced vendors to either raise prices or reduce margins. As a result, differentiation through software optimization, AI features and ecosystem services is becoming more critical than pure hardware upgrades.

Outlook: Local manufacturing and AI-ready growth

Looking toward 2030, compliance with Indonesia’s TKDN local content rules and expansion of local assembly hubs in Batam and Cikarang will shape competitive advantage. Vendors that successfully balance rising component costs with optimized software performance and AI-ready capabilities will be best positioned to capture Indonesia’s growing middle class.

FASNA SHABEER