India’s wearable device market is undergoing a critical transition. Shipments of wearable devices declined 6.3 percent year-over-year (YoY) in the first half of 2025 (1H25) to 51.6 million units. The slowdown marks the fifth consecutive quarterly decline, with volumes falling 9.4 percent YoY in Q2 2025 to 26.7 million units.

Despite weaker demand, average selling prices (ASPs) are inching upward, signaling a shift in consumer preferences toward differentiated features and premium positioning, According to International Data Corporation’s (IDC) India Monthly Wearable Device Tracker said.

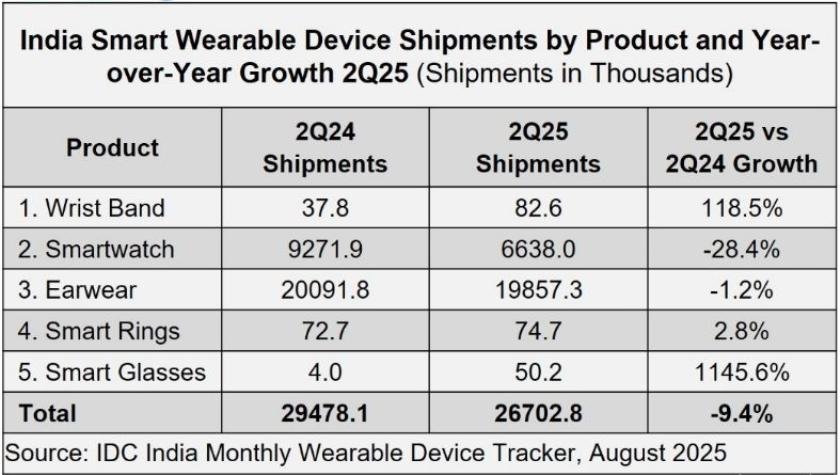

Growth Trends: From Mass Volumes to Emerging Categories

Smartwatches remain the hardest hit, with shipments down 28.4 percent YoY in Q2 2025. The category’s share of the wearables market dropped to 24.9 percent, down from 31.5 percent a year ago, as demand fatigue and entry-level saturation weighed heavily. Advanced smartwatches also declined, with volumes plunging nearly 40 percent.

Earwear, traditionally the growth engine of wearables, slipped 1.2 percent YoY, though the segment showed mixed performance. Truly Wireless Stereo (TWS) continued to dominate with a 71.2 percent share, while neckbands dropped 16.1 percent. Over-the-ear devices emerged as a bright spot, surging 97.4 percent YoY.

Emerging categories are showing early promise. Smart rings rebounded with 2.8 percent YoY growth, led by Ultrahuman, Gabit, and Aabo. Smart glasses surged from just 4,000 units a year ago to 50,000 in Q2 2025, driven by Meta and Lenskart launches. Wristbands, led by Samsung’s Galaxy Fit3, jumped 118.5 percent YoY to 83,000 units.

Purchasing Behavior: Online Weakness, Offline Resilience

Average selling prices are rising modestly—up 2.2 percent YoY in Q2 2025 to $19.2—indicating that consumers are willing to spend more for differentiated experiences. Online sales, however, dropped sharply by 13.8 percent YoY, with smartwatch shipments falling over 37 percent. Offline channels proved more resilient, slipping just 1.8 percent YoY overall, and even recording 4.4 percent growth in earwear. White-label smartwatches are also making a comeback through offline retail bundles in smaller markets, highlighting the evolving purchasing behavior of India’s consumers.

Innovation Outlook: Premiumization and AI-Driven Features

Vendors are betting on innovation to offset slowing volumes. In smartwatches, brands are pivoting toward mid-premium devices featuring advanced health sensors, NFC payments, AI-driven predictive health insights, and seamless device ecosystem integration. Earwear brands are exploring AI-led features such as personalized voice assistance, environment-aware sound tuning, real-time translation in Indian languages, and next-generation noise cancellation to stand out in a crowded market.

Smart glasses and smart rings, meanwhile, are carving out a niche with premium offerings, while Samsung’s success in wristbands shows consumers are open to fresh takes on familiar categories. IDC projects that while overall wearables may remain under pressure, innovation-led categories will drive the next phase of growth in India’s wearable market, Anand Priya Singh, market analyst, Smart Wearable Devices, IDC India, said.

Top wearable brands

In Q2 2025, boAt (Imagine Marketing) strengthened its leadership in India’s wearable market, increasing its share from 26.7 percent a year ago to 28 percent. Noise (Nexxbase) maintained second place with a stable 13.1 percent share compared to 13 percent in Q2 2024. Boult recorded strong growth, rising from 8.1 percent to 10.9 percent, reflecting its expanding presence in the market. OPPO (including OnePlus) also inched up slightly from 7.6 percent to 8 percent. Realme improved its position, growing from 5.3 percent to 6.5 percent. Meanwhile, the collective share of other vendors fell sharply from 39.3 percent to 33.5 percent, indicating stronger consolidation among the top five players.

Top smartwatch makers

In Q2 2025, Noise (Nexxbase) consolidated its leadership in the smartwatch segment, growing its market share from 25.7 percent to 30.9 percent. boAt also strengthened its position, rising from 11.6 percent to 13.7 percent. Boult made significant gains, more than doubling its share from 3.9 percent to 8.2 percent. Titan maintained steady performance, inching up from 7.9 percent to 8.1 percent. Fire-Boltt, however, saw a sharp decline, with its share dropping from 24.2 percent to 6.7 percent, losing a large portion of its market dominance. The “Others” category expanded notably from 26.7 percent to 32.4 percent, indicating growing traction for smaller and emerging brands.

Leaders in TWS segment

In Q2 2025, boAt (Imagine Marketing) retained its leadership in the TWS segment with a 31.9 percent share, though slightly down from 33.9 percent a year earlier. Boult gained momentum, increasing its share from 12.8 percent to 14.9 percent, strengthening its second-place position. Noise saw a marginal decline, slipping from 9.3 percent to 8.9 percent. OPPO, including OnePlus, inched up from 7.4 percent to 7.8 percent, while Realme improved from 6.4 percent to 7.5 percent. The share of other brands dropped from 30.2 percent to 29 percent, indicating continued consolidation among the top players.

Baburajan Kizhakedath