India’s smartphone market shipped 70 million units in the first half of 2025, posting 0.9 percent YoY growth, according to IDC report. The rebound was led by a 7.3 percent YoY rise in Q2 shipments to 37 million units after two quarters of decline.

Vivo retained the top spot for the sixth consecutive quarter, followed by Samsung, Oppo, and fast-growing challengers Nothing (+84.9 percent) and iQOO (+68.4 percent).

While new model launches, price cuts on older devices, and stronger offline channel margins boosted sales, subdued demand and rising average selling prices (ASPs) are expected to temper annual recovery.

Premium and mid-premium segments outperformed, with the $600–$800 range growing 96.4 percent and $400–$600 up 39.5 percent YoY, driven by Oppo, OnePlus, and Apple. Entry-level phones (<$100) grew 22.9 percent YoY, led by Xiaomi’s Redmi A4/A5, while the $200–$400 range saw a 2.5 percent shipment drop.

Qualcomm-based devices surged 37.6 percent YoY to 33.9 percent share, while MediaTek shipments fell 15.4 percent, dropping its share to 44.3 percent. Offline channels expanded 14.3 percent YoY to 53.6 percent share, benefiting from omnichannel strategies, while online sales remained flat.

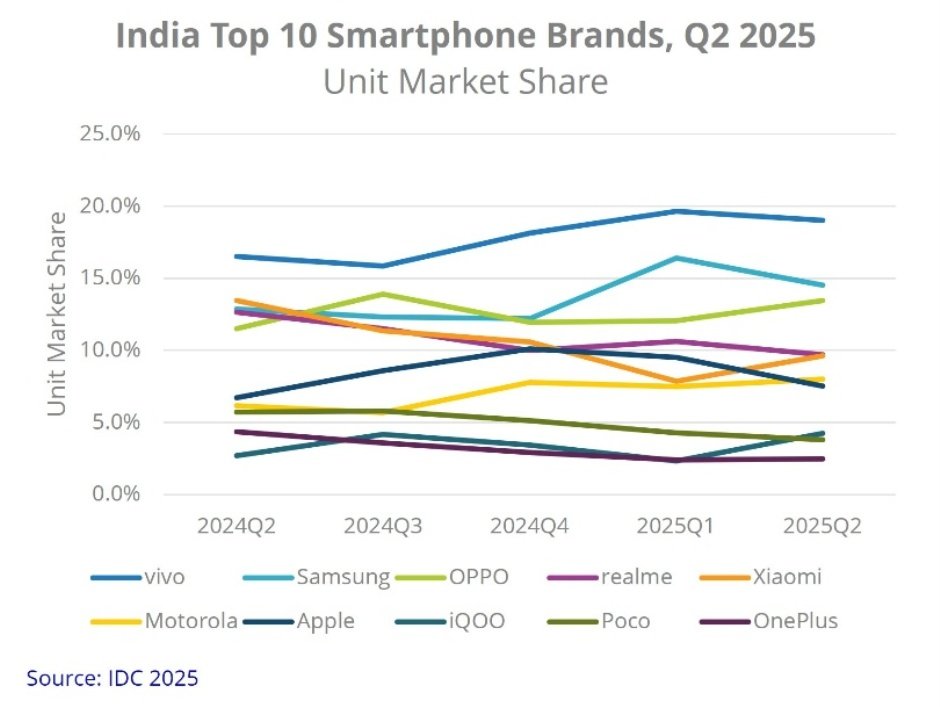

In Q2 2025, vivo led the Indian smartphone market with a 19.0 percent share, up from 16.5 percent a year ago, posting 23.5 percent year-on-year growth.

Samsung followed with 14.5 percent share, rising from 12.9 percent, and 21.0 percent growth.

OPPO ranked third at 13.4 percent, up from 11.5 percent, with a 25.4 percent increase in shipments.

Realme’s share dropped to 9.7 percent from 12.6 percent, reflecting a 17.8 percent decline, while Xiaomi fell to 9.6 percent from 13.5 percent, with a 23.5 percent drop.

Motorola saw strong momentum, climbing to 8.0 percent share from 6.2 percent, up 39.4 percent year-on-year.

Apple’s share improved to 7.5 percent from 6.7 percent, with 19.7 percent growth. Apple shipments grew 21.5 percent to 5.9 million units in 1H25, with the iPhone 16 emerging as India’s top-shipped model.

iQOO recorded the highest growth among the top players at 68.4 percent, expanding its share to 4.3 percent from 2.7 percent.

Poco’s share slid to 3.8 percent from 5.7 percent, a 28.8 percent decline, and OnePlus dropped to 2.5 percent from 4.4 percent, down 39.4 percent.

Others accounted for 7.7 percent share, up from 7.3 percent, with 12.7 percent growth. Overall, the market grew 7.3 percent year-on-year in Q2 2025.

IDC expects a low single-digit shipment decline for 2025 due to rising ASPs and budget segment contraction, even as iPhones maintain double-digit growth momentum.

“The second quarter of 2025 witnessed a flurry of new model launches across all price segments. This, coupled with price reductions on older models, increased offline channel margins, and strong above-the-line (ATL) marketing efforts, collectively fueled market growth,” said Aditya Rampal, Senior Research Analyst, Devices Research, IDC Asia Pacific.

Baburajan Kizhakedath