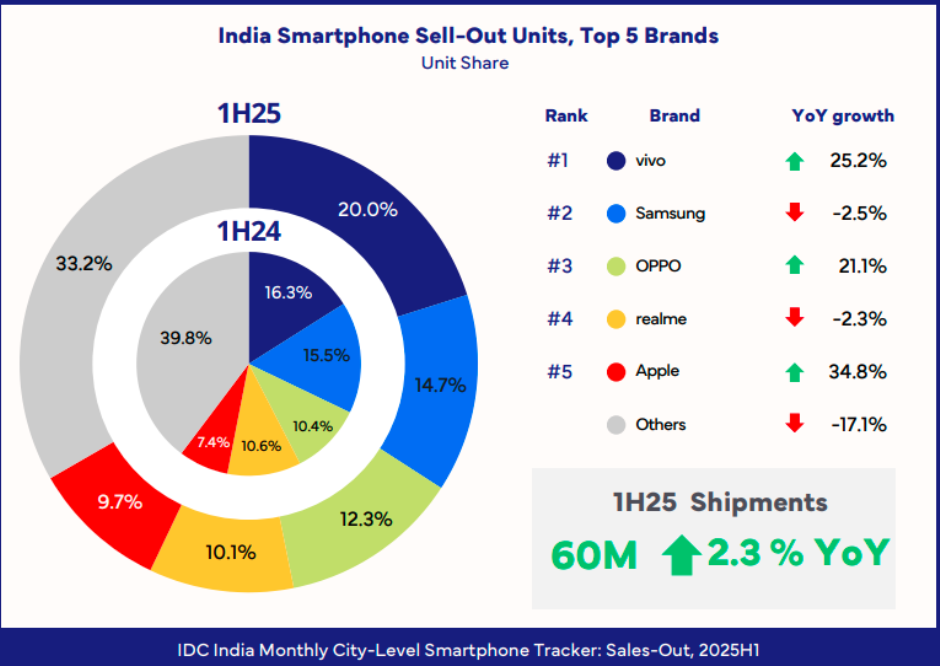

India’s smartphone market shipped 60 million units in the first half of 2025, registering 2.3 percent year-over-year growth, according to IDC.

Vivo led the market with a 20 percent share, rising sharply from 16.3 percent a year earlier on the back of strong mid-range and premium 5G sales, achieving 25.2 percent YoY growth.

Samsung ranked second with a 14.7 percent share, slipping from 15.5 percent in H1 2024 and posting a 2.5 percent decline, as intense competition eroded its mid-tier volumes.

OPPO captured 12.3 percent share, up from 10.4 percent last year, supported by a 21.1 percent YoY increase fueled by aggressive offline expansion and camera-centric models.

Realme saw its share drop to 10.1 percent from 10.6 percent, reflecting a 2.3 percent YoY dip amid fewer budget launches.

Apple continued its upward trajectory, climbing to a 9.7 percent share from 7.4 percent and marking the strongest growth among top brands at 34.8 percent YoY, thanks to rising demand for premium iPhones and expanded local manufacturing.

Apple ranked among the top five smartphone brands in North/South regions, as well as in Tier 1, 2, and 3 cities.

The “Others” category experienced the sharpest contraction, falling to 33.2 percent share from 39.8 percent with a 17.1 percent decline, indicating that smaller brands struggled to compete with leading players’ marketing and 5G portfolios.

Apple and Motorola emerged as the fastest-growing players in H1 2025. Apple continues to benefit from local manufacturing incentives and the popularity of its iPhone 15 series, while Motorola gained traction with competitively priced 5G devices and an expanded offline footprint.

Multiple cities in the Tier-4 category had a strong double-digit growth in 2025H1, fueled by demand in the ₹10K. Cities with the highest growth are #1 Mysore, #2 Shimla, #3 Asansol, #4 Rohtak, and #5 Trivandrum.

The IDC report indicated that subdued consumer spending and rising average selling prices (ASPs) continue to weigh on overall market momentum, while the uptick reflects steady demand.

Premium Segment Leads Growth

The ₹50,000+ premium smartphone category emerged as the fastest-growing segment, underscoring India’s shift toward high-end devices as affluent buyers seek advanced features and 5G capabilities. In contrast, the ₹10,000–₹20,000 range accounted for the largest share of total units sold, reinforcing its position as the volume driver of the market.

Regional Trends Highlight Urban Strength

Tier-1 cities outpaced other regions in sales growth, fueled by strong replacement demand and aggressive promotions from leading OEMs. Tier-4 cities, however, retained the biggest share of total shipments, underscoring the enduring importance of India’s vast rural and semi-urban consumer base. Tier-2 and Tier-3 cities recorded a slight decline, indicating a need for targeted marketing and financing schemes to reignite demand.

Outlook for 2025

IDC Senior Research Analyst Anjney Bhardwaj notes that while consumer demand remains cautious, the upcoming festive season and aggressive 5G rollouts could drive stronger growth in the second half of the year. Vendors are expected to focus on financing plans, trade-in offers, and localized features to tap both urban upgraders and first-time buyers in rural markets.

Baburajan Kizhakedath