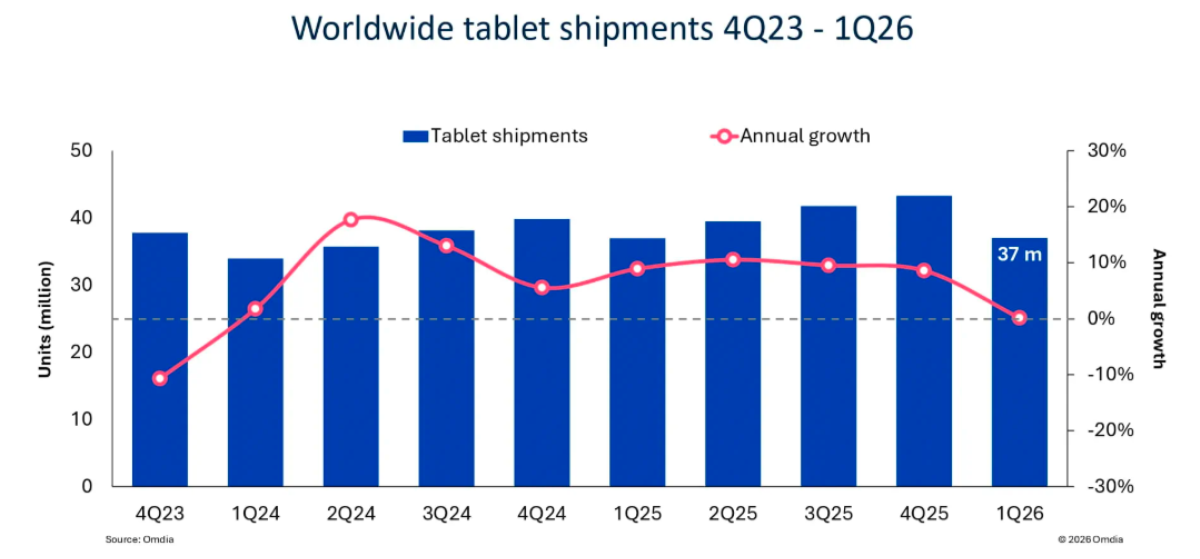

The global tablet market remained nearly unchanged in Q1 2026, with shipments rising just 0.1 percent to 37 million units, according to Omdia report.

Despite stable shipment volumes, leading tablet vendors are increasingly shifting focus toward premium devices as supply constraints, weak consumer demand, and pricing pressures weigh on the broader market.

Apple retained its leadership in the global tablet market with shipments of 14.8 million units in Q1 2026, recording 7.9 percent growth year on year. Apple’s performance was driven by strong demand for the iPad Air lineup, helping the company strengthen its position in the premium tablet category. Apple continued to dominate the market with an estimated share of around 40 percent of global tablet shipments.

Samsung ranked second with 5.8 million tablet shipments, though the vendor faced pricing challenges that resulted in a 12.6 percent decline. Samsung’s market share stood at roughly 15.7 percent during the quarter.

Huawei emerged as one of the fastest-growing tablet vendors in Q1 2026. Huawei shipped 3.2 million units, representing 28 percent annual growth, supported by its expansion strategy across Asia Pacific markets. Huawei captured approximately 8.6 percent market share during the quarter.

Lenovo also posted strong momentum, with shipments rising 20 percent to 3 million units. Lenovo benefited from education deployments and shipment pull-ins, securing an estimated 8.1 percent share of the global tablet market.

Xiaomi rounded out the top five vendors with shipments of 2.6 million units. However, Xiaomi experienced a 13.6 percent decline amid weakening demand in the mass-market tablet segment. Its market share remained near 7 percent.

Omdia analyst Himani Mukka said leading tablet vendors in 2026 are prioritizing premium devices as profitability and consumer demand remain stronger at the higher end of the market.

Device vendors operating across both smartphone and tablet businesses are increasingly focusing investment and supply allocation toward smartphones, which contribute significantly more revenue and margins.

Latin America, along with the Middle East and Africa, delivered the strongest regional shipment growth in Q1 2026. However, much of this increase was linked to inventory build-up rather than actual end-user demand, signaling a cautious outlook for the second half of 2026.

Omdia also highlighted continued weakness in the Chromebook market. Global Chromebook shipments declined sharply as education-related deployments slowed and supply-chain constraints delayed projects such as Japan’s GIGA School Program 2.0.

Within the Chromebook segment, Lenovo remained the largest vendor despite shipments falling 11.2 percent year on year to 1.5 million units. HP shipped 1 million units, down 15.3 percent, while Acer shipped 937,000 units with relatively stable demand in North America and APAC.

Dell Technologies recorded the steepest decline among leading Chromebook vendors, with shipments dropping 28.3 percent year on year to 413,000 units. Meanwhile, ASUS was the only Chromebook vendor to post growth, with shipments increasing 3.5 percent year on year to 406,000 units, giving it a 9 percent market share.

Omdia expects the tablet and Chromebook markets to remain under pressure through the second half of 2026 as vendors face supply constraints, weaker promotional flexibility, and limited refresh demand in lower-priced segments.

BABURAJAN KIZHAKEDATH