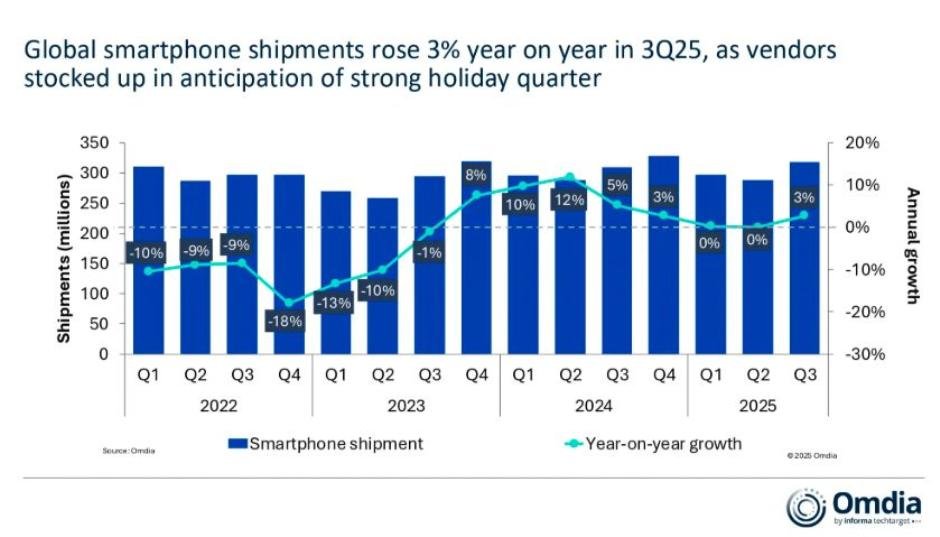

The smartphone market returned to growth in the third quarter of 2025, as shipments rose between 2.6 percent and 3 percent year-on-year to around 323 million units, according to IDC and Omdia. The rebound reflects renewed consumer demand, robust replacement cycles, and growing interest in AI-enabled smartphones and innovative foldable devices.

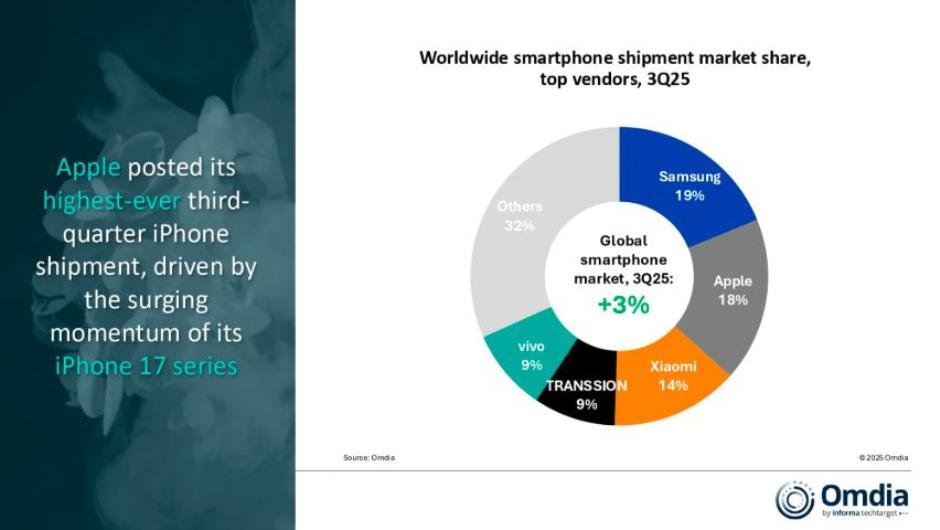

Samsung Maintains Leadership with 19 percent Market Share

Samsung retained its position as the world’s top smartphone vendor for the third consecutive quarter, capturing a 19 percent global market share. The company’s performance was supported by strong demand for its Galaxy A-series midrange smartphones and the upgraded Galaxy Z Fold 7 and Galaxy Z Flip 7, which outperformed earlier foldable generations.

Both IDC and Omdia noted that Samsung achieved its strongest July-quarter growth on record, driven by a balanced portfolio spanning premium and affordable segments. The company’s dual focus on innovation and accessibility, coupled with aggressive trade-in and financing programs, strengthened its market position amid a challenging global economy. Samsung shipped 61.4 million smartphones in Q3 2025 vs 57.7 million in Q3 2024, IDC report said.

Apple Records Best-Ever Q3 with 18 percent Market Share

Apple posted its strongest third-quarter performance ever, growing shipments by around 4 percent year-on-year and securing an 18 percent share of global smartphone shipments. Early demand for the iPhone 17 series drove sales beyond expectations, with the base iPhone 17 standing out for its upgraded storage and unchanged pricing.

According to Omdia report, the redesigned iPhone 17 Pro and Pro Max attracted high-end consumers globally, while the iPhone Air, though shipping modest volumes, proved valuable as a technical testbed for Apple’s next-generation form factors.

IDC highlighted that Apple achieved its best results ever for a July quarter, underscoring its dominance in the premium segment. Apple shipped 58.6 million smartphones in Q3 2025 vs 57 million in Q3 2024, IDC said.

Xiaomi Consolidates Recovery with 14 percent Market Share

Xiaomi maintained strong momentum, capturing 14 percent of the global market in 3Q25. The company continued its recovery across Europe and Latin America, driven by the popularity of its Redmi Note and Poco series. IDC reported that Xiaomi’s strategic focus on midrange devices with AI imaging features and competitive pricing helped it regain share amid recovering consumer demand. Xiaomi shipped 43.5 million smartphones in Q3 2025 vs 42.8 million in Q3 2024, IDC said.

Omdia added that Xiaomi’s ability to optimize inventories during the slower first half of 2025 positioned it well to meet the Q3 rebound, as vendors ramped up production ahead of the holiday season.

Transsion and Vivo Expand in Emerging Markets

Transsion Holdings, which manages the Tecno, Infinix, and Itel brands, and vivo each captured 9 percent of the global market in Q3 2025, according to Omdia.

Transsion recorded double-digit growth, marking its highest-ever third-quarter volume, driven by strong demand across North and East Africa, and refreshed models such as the Infinix Hot 60 and Smart 10 series.

IDC highlighted Transsion’s competitive strength in the sub-$200 smartphone segment, supported by extensive distribution networks and effective marketing. Transsion shipped 29.2 million smartphones in Q3 2025 vs 25.7 million in Q3 2024, IDC said.

Vivo, meanwhile, regained share in emerging markets, leveraging AI-driven camera features and aggressive online promotions. Vivo shipped 28.8 million smartphones in Q3 2025 vs 27 million in Q3 2024, IDC said.

AI, Foldables, and Financing Models Drive Growth

Analysts from both IDC and Omdia emphasized that AI integration, foldable innovation, and flexible purchasing options were the defining trends of 3Q25.

Nabila Popal, Senior Research Director at IDC, said OEMs have “mastered the art of innovation” in both hardware and financing models, combining cutting-edge features with trade-in and installment programs that make upgrading easy for consumers.

Runar Bjorhovde, Senior Analyst at Omdia, said competitive pressures in the market are intense, and many vendors are experiencing significant strain on profitability. Rising bill-of-materials (BoM) costs, for example, are tightening the balance between competitive pricing versus margins.

Omdia analysts added that AI-powered smartphones, bold color designs, and back-cover displays have captured consumer attention, while portfolio segmentation and marketing execution remain critical to sustaining momentum.

Outlook: AI-Enabled Smartphones to Drive Year-End Surge

Looking ahead, both research firms forecast continued momentum into Q4 2025, with demand expected to rise as vendors launch AI-optimized models and holiday promotions.

IDC expects a strong finish to 2025, supported by aggressive pricing, diverse product portfolios, and growing enthusiasm for AI-driven experiences.

However, analysts caution that vendors still face rising component costs and competitive pricing pressures, especially in emerging markets. Strategic focus on ecosystem monetization, accessory bundles, and subscription services will be key to maintaining profitability amid tightening margins.

Baburajan Kizhakedath