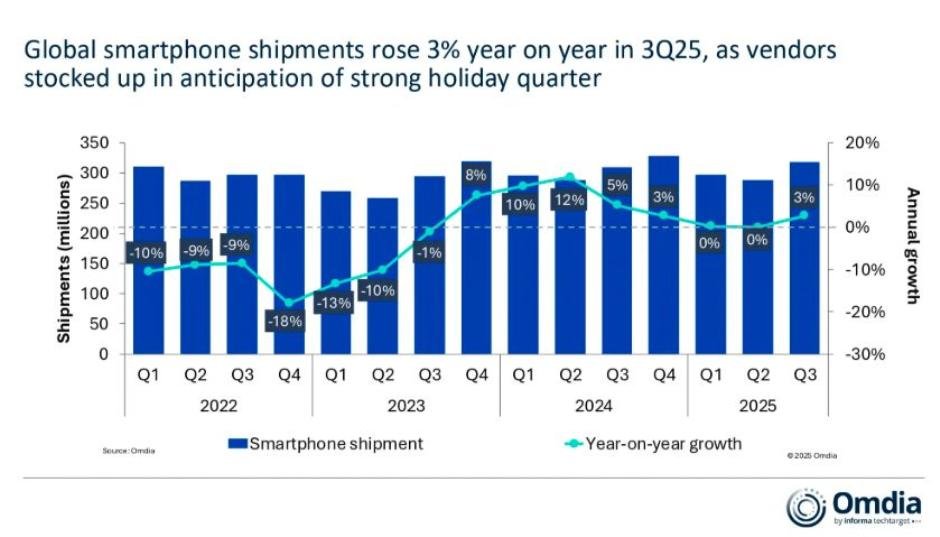

The global smartphone market returned to growth in the third quarter of 2025, rising 3 percent year on year, driven by strong product launches and replacement demand, according to the latest research from Omdia.

Strong 3Q25 Growth Fueled by Replacement Demand and Inventory Stocking

This rebound signals renewed momentum in the global smartphone industry ahead of a busy holiday season, Le Xuan Chiew, Research Manager at Omdia, said in the report. The market recovery was powered by consumers upgrading their devices and vendors stocking inventories in preparation for 4Q25, historically the busiest quarter for smartphone sales. Omdia highlighted that this growth reflects a positive response to the industry’s major launch events and evolving consumer preferences.

Top Vendors in 3Q25

The top five smartphone vendors maintained strong performances during the quarter:

Samsung: Maintained the number one spot for the third consecutive quarter with 19 percent market share, supported by the Galaxy A series and its 7th generation foldable lineup.

Apple: Grew iPhone shipments by 4 percent, achieving its strongest Q3 performance ever, thanks to early demand for the iPhone 17 series, securing 18 percent market share.

Xiaomi: Delivered a steady quarter, capturing 14 percent market share.

TRANSSION: Expanded by double digits, supported by the Infinix Hot 60 and Smart 10 series, achieving its highest 3Q volume ever with 9 percent market share.

vivo: Also captured 9 percent market share, rounding out the top five globally.

Product Highlights Driving Consumer Interest

Omdia noted that consumer excitement is centered on devices offering:

Foldables and innovative form factors

Slim, colorful designs

Enhanced back-cover displays

The iPhone 17 series stood out with upgraded storage options, redesigned Pro and Pro Max models, and a compelling value proposition, driving global adoption. Even the iPhone Air, while modest in volume, served as a testbed for Apple’s future innovations.

Strategic Inventory and Market Management

Vendors leveraged the muted first half of 2025 to streamline operations, optimize launch cycles, and calibrate inventories, positioning themselves to benefit from renewed consumer demand in 3Q25.

Market Challenges: Profitability, BoM Costs, and Emerging Markets

Despite growth, vendors face intense competitive pressures and rising bill-of-materials (BoM) costs, especially for semiconductors, storage, and memory, as AI and datacenter demand intensifies.

“The reality is that neither competition nor BoM costs will see short-term relief, making it essential for vendors to capture wider opportunities to grow revenues and differentiate themselves in the market,” noted Runar Bjørhovde, Senior Analyst at Omdia.

To maintain profitability and expand revenue streams, vendors are increasingly focusing on:

Subscription services and ecosystem offerings

Accessories and bundle sales

Financing options in emerging markets to avoid price wars while keeping devices accessible

Outlook for the Global Smartphone Market

Omdia’s research underscores that 3Q25 growth reflects both strong replacement demand and strategic vendor planning. Success in the coming quarters will depend on effective portfolio segmentation, marketing strategies, and the ability to navigate economic uncertainties while addressing consumer expectations for innovation and affordability.

The global smartphone market is regaining momentum, with Samsung and Apple leading the charge. Phone vendors that can balance volume growth, profitability, and strategic innovation are positioned to capitalize on the recovering market and emerging opportunities.

Baburajan Kizhakedath