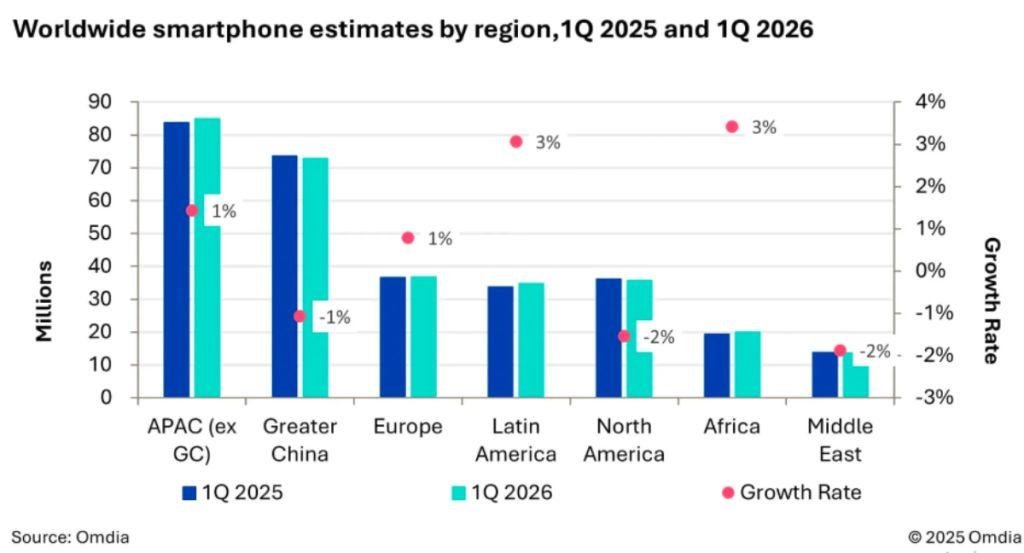

The global smartphone market shipped 298.5 million units in Q1 2026, registering 1 percent year-on-year growth, according to Omdia. The quarter reflected a complex mix of strong vendor performance and weakening consumer demand, driven largely by supply-side dynamics and inflationary pressures.

Samsung retained its leadership position with 65.4 million shipments, growing 8 percent year-on-year. Its performance was supported by strong demand across both entry-level A-series devices and premium Galaxy S26 models.

Apple followed with 60.4 million units, rising 10 percent, driven by the iPhone 17 series, including strong traction for the iPhone 17e in Europe and Japan, and a 42 percent surge in Mainland China for Pro models.

Based on shipments, Samsung held around 21.9 percent market share, while Apple captured approximately 20.2 percent. Xiaomi ranked third with 33.8 million units, translating to about 11.3 percent share, but recorded a sharp 19 percent decline due to heavy exposure to the sub-$200 segment and rising component costs. OPPO, including realme and OnePlus, shipped 30.7 million units for roughly 10.3 percent share, while vivo accounted for 21.3 million units or about 7.1 percent share, both experiencing single-digit declines.

Among emerging players, HONOR stood out with 19.2 million shipments, growing 19 percent year-on-year, driven by strong international expansion, particularly in the Middle East and Africa.

Smartphone buying trends in Q1 2026 were heavily influenced by vendor-led front-loading. Smartphone brands accelerated shipments ahead of anticipated increases in memory and component costs, boosting overall market performance, Omdia Research Manager Le Xuan Chiew said in the report.

However, this created a disconnect between shipments and actual consumer demand. Persistent inflation has reduced discretionary spending, leading to longer replacement cycles and more selective purchasing, especially in mid-to-premium segments.

Entry-level smartphones faced additional pressure as vendors passed on rising costs to consumers, impacting demand in price-sensitive emerging markets. This has widened the gap between channel inventory and real consumption.

Looking ahead, the market is expected to face a correction starting in Q2 2026 as excess inventory is absorbed. Growth is likely to remain subdued in the second half of the year, with inflation continuing to impact consumer spending. Vendors are expected to shift focus toward inventory management, margin protection, and disciplined shipments, as the industry navigates a period of structural disruption driven by rising component costs and evolving demand patterns.

BABURAJAN KIZHAKEDATH