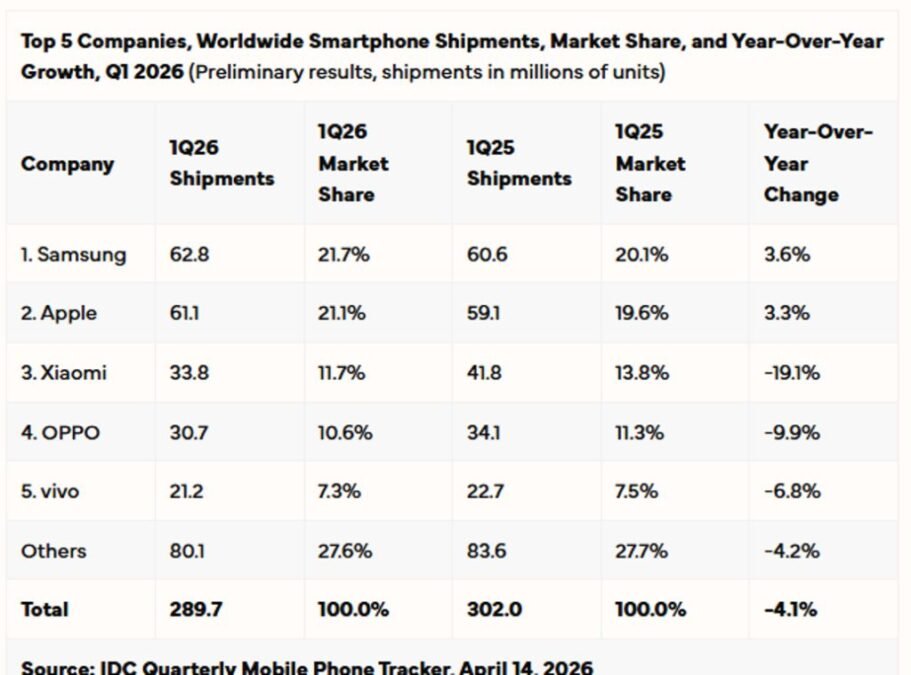

The global smartphone market entered a challenging phase in the first quarter of 2026, with shipments declining 4.1 percent year-over-year to 289.7 million units, IDC report said.

IDC’s Worldwide Quarterly Mobile Phone Tracker said this downturn ended a 10-quarter growth streak that had persisted since mid-2023, signaling a shift in market dynamics driven by supply-side pressures and rising costs.

Memory Shortages and Rising Costs Weigh on Growth

The slowdown in the global smartphone market is attributed to memory supply constraints, which have limited production volumes while simultaneously driving up component costs. Smartphone vendors are facing increased bill-of-materials expenses, leading to price hikes across several markets.

In emerging economies, smartphone prices have surged by 40-50 percent, significantly dampening demand in price-sensitive segments, Nabila Popal, senior research director for Worldwide Consumer Devices, IDC, said.

Smartphone manufacturers are responding with cost-control measures such as reducing marketing spend, tightening channel support, and adopting despecing strategies. However, these steps are also constraining growth potential.

Additional pressure from higher energy and logistics costs, partly linked to geopolitical tensions in the Middle East, is further complicating the outlook for 2026.

Samsung and Apple Lead Amid Market Turbulence

Despite the smartphone market decline, Samsung and Apple emerged as the only top five vendors to register year-over-year growth.

Samsung reclaimed the top position, driven by strong demand for its flagship Galaxy S26 Ultra and the timely rollout of its mid-range A-Series. The company recorded a 3.6 percent increase in shipments, supported by stable pricing and a balanced product strategy.

Apple secured second place with a 3.3 percent growth in shipments, fueled by the success of the iPhone 17 series, particularly in China where sales grew by over 30 percent. However, supply disruptions and reduced channel support in certain regions limited further expansion.

Chinese Vendors Maintain Positions Despite Pressure

Chinese smartphone makers faced mixed performance during the quarter. Xiaomi retained its third position despite experiencing the steepest decline among the top five, as it strategically reduced shipments of older models to avoid aggressive price increases.

OPPO ranked fourth, benefiting from stronger domestic performance following its integration with realme, which helped offset global declines. vivo secured fifth place, supported by robust performance in China and continued leadership in India.

Outside the top five, vendors such as Honor, Lenovo (Motorola), and Huawei posted positive growth, with Honor leading the top ten with a 24 percent increase, driven by its international expansion strategy.

Market Shifts Toward Premiumization

The smartphone industry is increasingly shifting toward higher price segments as vendors attempt to offset rising costs. Premium devices continue to show resilience, with Samsung and Apple leveraging their strong positioning to maintain stable pricing strategies.

Meanwhile, brands with significant exposure to entry-level devices are under increasing pressure as the sub-$200 segment faces erosion due to rising component costs. Vendors are gradually repositioning their portfolios toward higher-margin products, though this transition remains challenging in highly competitive markets.

Outlook: Challenging Road Ahead with Gradual Stabilization

The 4 percent decline in Q1 2026 is expected to be an early indicator of broader challenges throughout the year. Developed markets such as the US are likely to remain relatively resilient due to financing options and trade-in programs that support premium device adoption.

In contrast, emerging markets will face significant constraints, with limited affordable options available to consumers. The memory supply situation is expected to remain tight in the near term, with stabilization projected only by the second half of 2027.

Despite these headwinds, the long-term trend toward premiumization and higher average selling prices is expected to continue, reshaping the global smartphone landscape as vendors adapt to evolving cost structures and consumer demand patterns.

BABURAJAN KIZHAKEDATH