China’s tablet market recorded strong growth in 2025, driven by replacement demand, government subsidies, and rising consumer upgrades, according to new data from IDC.

China tablet shipments rise 13.1 percent in 2025

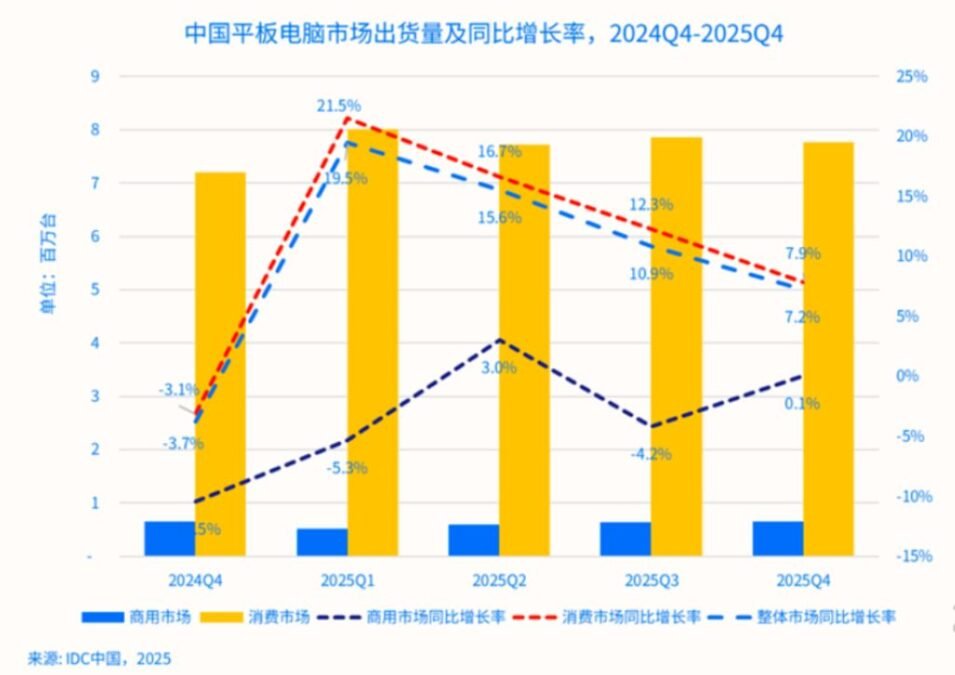

IDC’s Quarterly Tablet Tracker shows that tablet shipments in China reached 33.76 million units in 2025, representing 13.1 percent growth. The growth was supported by an ongoing replacement cycle and the impact of government subsidy programs that encouraged consumers to upgrade devices and boosted purchase conversions.

In the fourth quarter of 2025, tablet shipments increased 7.2 percent, though growth slowed compared with earlier quarters as subsidy programs tightened in some regions. The tablet market is shifting from policy-driven demand to product and user demand.

Consumer upgrades drive growth while commercial demand slows

Consumer segment shows clear upgrade trend

The consumer market was the main growth engine, with shipments rising 14.4 percent. Several factors drove the upgrade cycle:

Higher demand for performance and premium experiences

Lower entry barriers due to subsidies

Expansion of mid- to high-end tablet portfolios

Growth of large-screen, compact flagship, AI-enabled, and 2-in-1 tablets

As a result, the mainstream price band increased by around RMB 500 compared with the previous year.

Commercial market faces budget pressure

The commercial tablet segment declined 1.6 percent in 2025 due to budget constraints and limited new use cases in some industries. However, the education sector remained stable, with rising demand from private schools and training institutions providing some support.

Top tablet vendors in China in 2025

Huawei retains No.1 position

Huawei remained the market leader with 29.2 percent share in 2025 vs 32.3 percent in 2024. New product launches strengthened its positioning in productivity and multi-scenario usage, keeping brand momentum strong.

Apple strengthens premium segment

Apple ranked second with 24.5 percent share in 2025 vs 26.6 percent share in 2024. Apple has recorded annual shipment growth. New flagship launches reinforced its leadership in the high-end market, while promotional campaigns boosted quarterly share.

Xiaomi records annual growth but Q4 slows

Xiaomi secured third place with 13.1 percent share in 2025 vs 12.7 percent share in 2024. Xiaomi achieved double-digit annual shipment growth. However, tightening subsidies and earlier product refresh cycles led to weaker Q4 momentum.

Lenovo surges with strong Q4 performance

Lenovo saw rapid shipment growth in 2025 and moved up to third place in Q4. Lenovo has 9.7 percent share in 2025 vs 6.7 percent share in 2024. Lenovo’s value-for-money products and rising interest in smaller tablets supported expansion.

Honor maintains fifth position

Honor ranked fifth for both the full year and Q4. Honor has 8.6 percent share in 2025 vs 8.3 percent share in 2024. Honor is focusing on product upgrades and expanding its portfolio across consumer and education segments.

Market outlook: AI, rising costs and replacement demand shape future

IDC highlights several trends shaping the future of China’s tablet market:

Expanding user base supports future upgrades

The replacement cycle and subsidy programs have expanded the tablet user base, creating a stronger foundation for future upgrades and continued demand.

Rising component costs increase pressure

Higher memory and component prices are creating cost challenges for tablet vendors. Companies will need stronger supply chain optimization, product planning, and channel strategies.

AI and scenario-based use cases remain key

The tablet market is expected to evolve toward AI integration and multi-scenario usage. Future competition will depend on ecosystem development, application optimization, and real-world use case innovation.

IDC expects the market to continue transitioning from subsidy-driven growth to product-driven and demand-driven expansion, with AI and premium upgrades becoming the next major growth drivers.

BABURAJAN KIZHAKEDATH