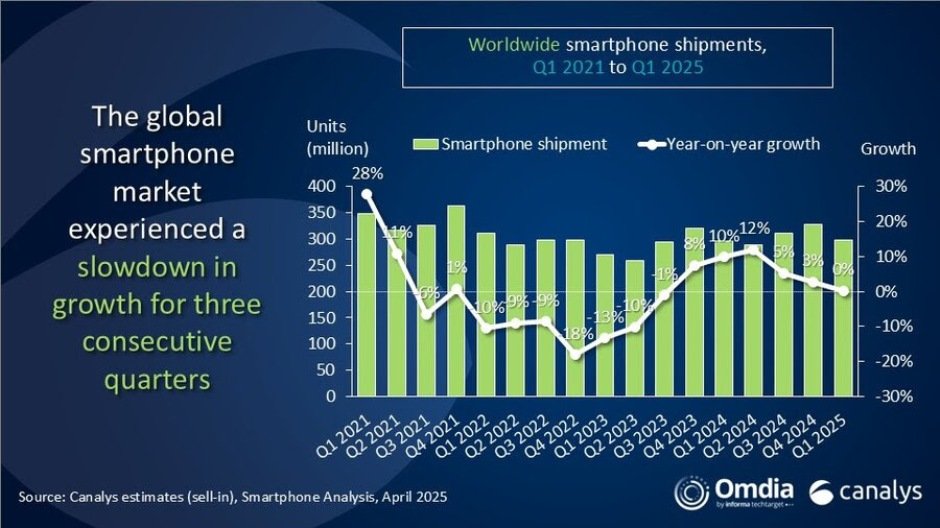

The global smartphone market grew just 0.2 percent in Q1 2025, reaching 296.9 million units from 296.2 million in Q1 2024, according to Canalys (now part of Omdia).

Growth of the smartphone market slowed for the third consecutive quarter due to the end of the peak replacement cycle and efforts by phone vendors to maintain healthy inventory levels.

Samsung retained the top spot with 60.5 million units shipped, boosted by its new flagship and affordable A-series models.

Regional trends diverged sharply: while India, Latin America, and the Middle East saw declines due to market saturation, growth continued in Mainland China, helped by government subsidies, and in Africa, supported by strong retail activity. In contrast, Europe declined again due to high-end inventory backlogs and regulatory disruptions.

The U.S. smartphone market outperformed, rising 12 percent, driven by Apple’s preemptive inventory buildup ahead of potential tariff changes.

Apple expanded iPhone production in India, signaling a strategic shift to reduce dependence on China. Tariff impacts are expected to raise average selling prices and reduce entry-level device availability in the U.S., potentially increasing market volatility in the coming quarters.

Despite a weak Q1, vendors remain optimistic, expecting a recovery in H2 2025, buoyed by declining inventories and new product launches. However, challenges persist, including cautious hardware upgrades, intensified mid-range competition, and growing pressure for localized manufacturing amid geopolitical tensions.

Smartphone leaders

In Q1 2025, Samsung shipped 60.5 million smartphones, up slightly from 60.0 million in Q1 2024, maintaining a steady 20 percent market share.

Apple saw a notable increase in shipments from 48.7 million to 55.0 million, resulting in a rise in market share from 16 percent to 19 percent.

Xiaomi, including its sub-brands Redmi and POCO, shipped 41.8 million units compared to 40.7 million the previous year, holding a consistent 14 percent share.

Vivo grew its shipments from 21.4 million to 22.9 million, with its market share increasing from 7 percent to 8 percent.

OPPO experienced a decline, shipping 22.7 million units versus 25.0 million a year earlier, though its market share remained at 8 percent. The Others category saw a significant drop in shipments from 100.5 million to 94.0 million, with market share falling from 34 percent to 32 percent.

Baburajan Kizhakedath