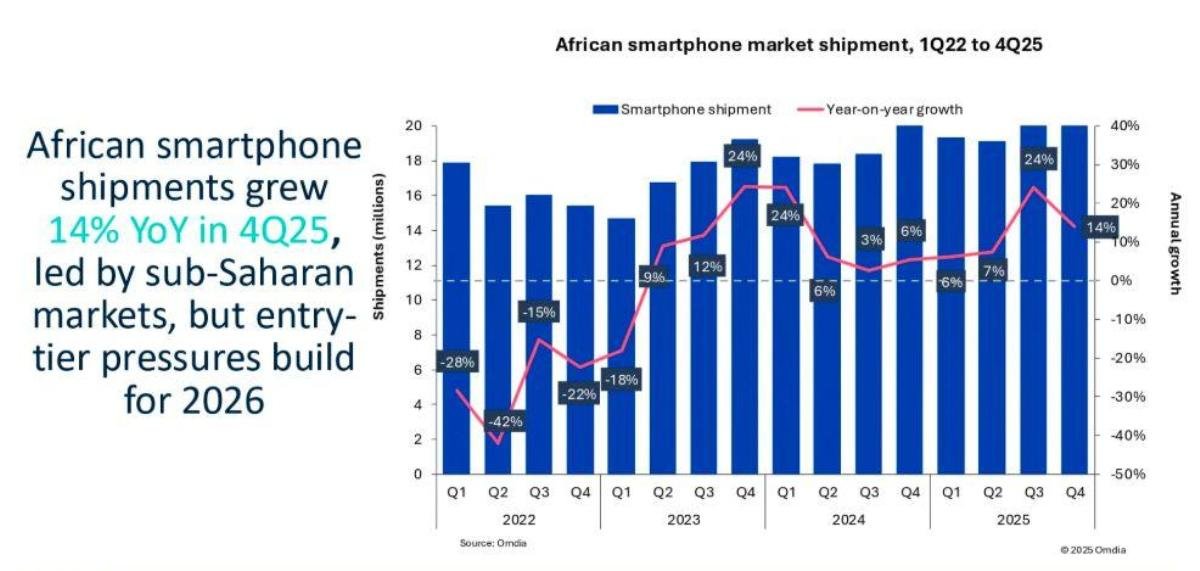

Africa’s smartphone market ended 2025 on a strong footing, with fourth quarter shipments rising 14 percent to 23.1 million units, according to new research from Omdia.

Growth in Africa smartphone market was supported by expanding device-financing options across East, West, and Southern Africa, stabilizing currencies, accelerating 4G adoption, and early 5G rollout in markets such as South Africa and Egypt, Manish Pravinkumar, Principal Analyst at Omdia, said in the report.

Full-Year 2025 Shipments Reach 84.4 Million Units

In 2025, Africa shipped 84.4 million smartphones, marking 13 percent growth and outperforming global market trends. The year represented the strongest recovery phase since 2021, as deferred replacement demand normalized and channel inventories stabilized.

Smartphones accounted for around 55 percent of mobile handset shipments in 2025, underlining the region’s steady transition from feature phones to entry-level and mid-tier smartphones.

Sub-Saharan Africa Leads Regional Growth

In 4Q25, Sub-Saharan Africa outperformed North Africa, reinforcing its role as the main growth engine.

South Africa recorded 38 percent growth, driven by strong prepaid demand, with sub-$100 devices contributing 22 percent of shipments.

Nigeria expanded 25 percent, supported by affordable 4G smartphone adoption, with sub-$200 models dominating volumes.

Kenya posted modest 3 percent growth as cost-of-living pressures limited discretionary upgrades.

In North Africa:

Egypt grew 22 percent, aided by local manufacturing and value-focused portfolios from vendors such as Samsung, Xiaomi, and OPPO. Devices priced between $100 and $199 accounted for 60 percent of shipments.

Algeria rose 5 percent.

Morocco declined 3 percent due to high import duties affecting affordability.

Q4-2025

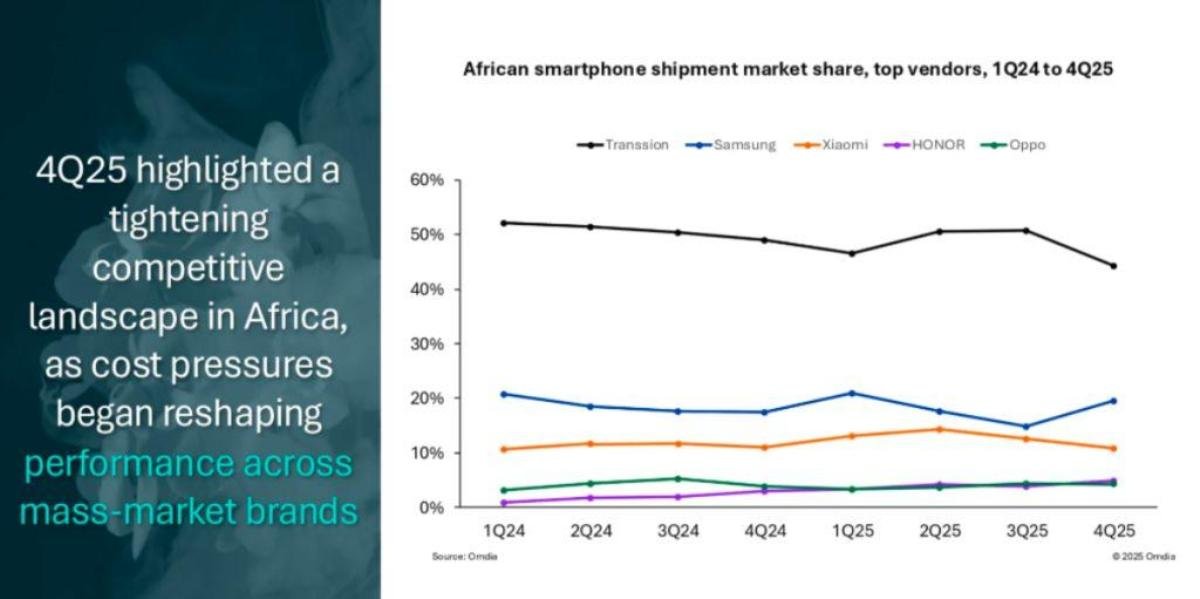

Vendor Performance: TRANSSION Retains Leadership

Africa’s smartphone market in 4Q25 showed steady growth in shipments, with notable shifts in market share among leading vendors compared to 4Q24. Africa’s smartphone market in 4Q25 reached 23.1 million, registering 14 percent growth.

TRANSSION retained its leadership position with shipments rising slightly to 10.2 million units in 4Q25 from 10.0 million in 4Q24. However, its market share declined to 44 percent from 49 percent, indicating intensified competition despite stable volume growth.

Samsung recorded strong growth, with shipments increasing to 4.5 million units from 3.5 million a year earlier. Its market share expanded to 20 percent in 4Q25 from 17 percent in 4Q24, making it the biggest gainer among the top vendors.

Xiaomi posted moderate growth, shipping 2.5 million units compared to 2.2 million in 4Q24. Its market share remained stable at 11 percent year over year.

HONOR saw significant momentum, with shipments nearly doubling to 1.1 million units from 0.6 million in 4Q24. Its market share rose to 5 percent from 3 percent, reflecting rapid expansion.

OPPO increased shipments to 1.0 million units from 0.8 million, while maintaining a steady 4 percent market share.

The “Others” category also grew to 3.7 million units from 3.1 million, with market share edging up to 16 percent from 15 percent.

Overall, Africa’s smartphone market in 4Q25 experienced shipment growth across most vendors, with competitive dynamics shifting as Samsung and HONOR gained share while TRANSSION’s dominance slightly narrowed.

2025

Africa’s smartphone market recorded solid growth in 2025, with total shipments increasing across most major vendors compared to 2024, while market share dynamics showed gradual shifts among leading brands.

TRANSSION maintained its dominant position with shipments rising to 40.5 million units in 2025 from 37.9 million in 2024. However, its market share declined to 48 percent from 51 percent, reflecting intensifying competition despite higher volumes.

Samsung shipped 15.3 million units in 2025, up from 13.9 million in 2024. Its market share slipped slightly to 18 percent from 19 percent, indicating steady growth in volume but marginal share erosion.

Xiaomi posted strong gains, with shipments climbing to 10.7 million units from 8.4 million in 2024. Its market share improved to 13 percent from 11 percent, making it one of the key share gainers during the year.

HONOR recorded the fastest growth among leading vendors, more than doubling shipments to 3.5 million units from 1.4 million in 2024. Its market share increased to 4 percent from 2 percent, highlighting rapid expansion in the region.

OPPO saw shipments rise modestly to 3.4 million units from 3.1 million, while maintaining a stable 4 percent market share year over year.

The “Others” category grew to 11.1 million units from 10.0 million, with market share steady at 13 percent.

Overall, Africa’s smartphone market in 2025 expanded in terms of shipments, with TRANSSION retaining leadership but losing some share, while Xiaomi and HONOR emerged as the strongest gainers in both volume and market presence.

Africa’s smartphone average selling prices increased 11 percent in 4Q25, reflecting higher component costs and a shift toward better-specified entry and mid-tier devices.

2026 Outlook: Market Correction Expected

Omdia forecasts a 23 percent year-on-year decline in smartphone shipments across Africa in 2026. With 81 percent of 2025 shipments priced below $200, the market remains highly exposed to component inflation.

Rising prices could lead prepaid and first-time buyers to delay upgrades or shift to lower configurations and refurbished devices. Channel partners are expected to tighten inventory discipline, focusing on faster-moving models to mitigate stock risks.

The impact is expected to vary by country. Nigeria and Kenya may experience sharper volume pressure due to their concentration in sub-$200 devices, while Egypt could remain more resilient due to local manufacturing advantages. South Africa’s operator-led and postpaid structure may offer relative insulation through premium demand.

BABURAJAN KIZHAKEDATH