Global smartphone shipments dipped slightly to 288.9 million units in Q2 2025 due to subdued consumer demand, with vendors focusing on selective regional growth and profitability strategies.

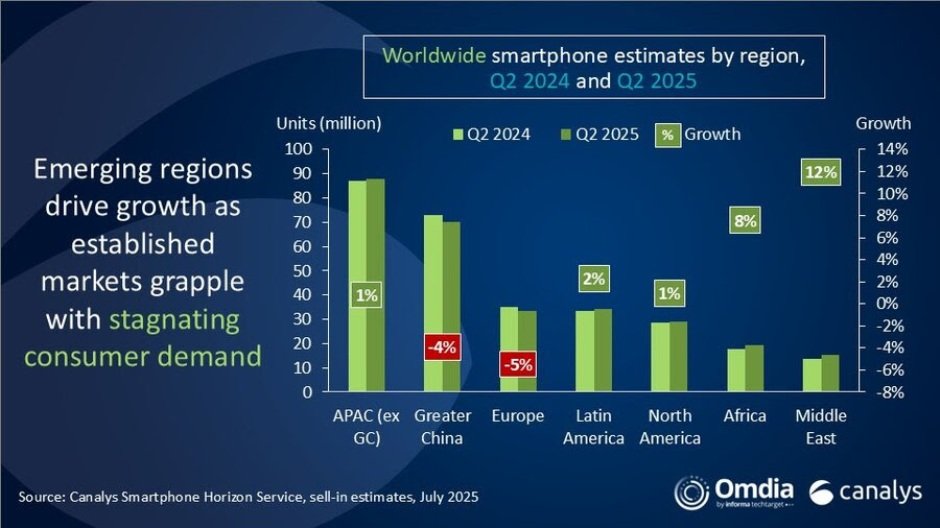

According to Canalys and Omdia, smartphone shipments in Q2 2025 increased most notably in the Middle East, up 12 percent, followed by Africa at 8 percent, Latin America at 2 percent, and North America at 1 percent.

The Asia Pacific region (excluding Greater China) also grew modestly by 1 percent. In contrast, Greater China and Europe saw declines, with shipments falling by 4 percent and 5 percent, respectively.

This shift reflects the growing importance of emerging telecom markets in sustaining telecom growth, as mature markets struggle with saturation and subdued consumer sentiment.

Regional trends played a critical role, with Africa and the Middle East emerging as growth drivers — supported by government policies, financing innovations, and seasonal sales, Manish Pravinkumar, Principal Analyst at Canalys, said.

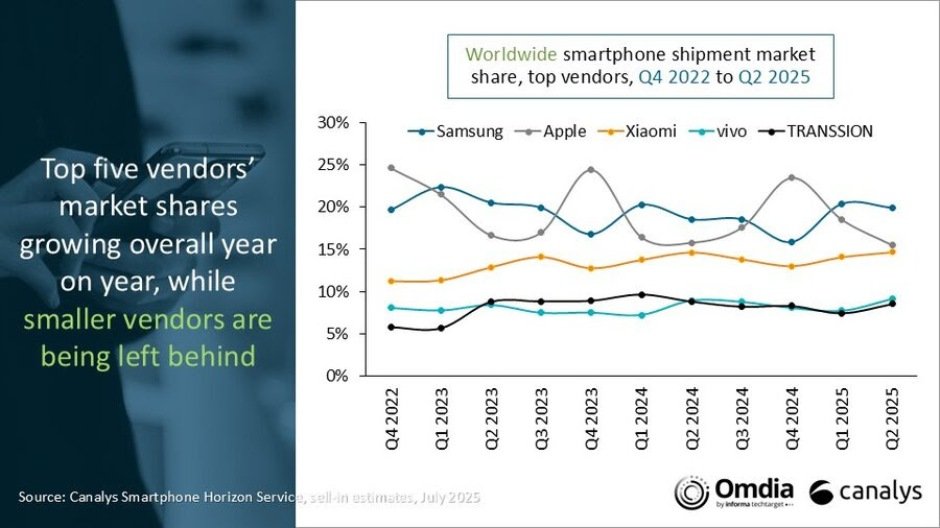

Top smartphone vendors

Samsung led the market with 57.5 million units shipped, up from 53.5 million last year, increasing its market share from 19 percent to 20 percent. Samsung’s growth was fueled by strong performance in its Galaxy A series and strategic inventory moves in the US, Aaron West, Senior Analyst at Omdia, said.

Apple shipped 44.8 million units, a slight dip from 45.6 million, maintaining a 16 percent share. Apple maintained resilience despite pressure in China and the US.

Xiaomi remained steady with 42.4 million units compared to 42.3 million last year, holding a 15 percent share. Xiaomi held third place boosted by demand in Latin America and Africa.

Vivo shipped 26.4 million units versus 25.9 million, keeping a 9 percent share. Vivo achieved 2 percent growth on Indian momentum.

TRANSSION’s shipments dipped 3 percent to 24.6 million from 25.5 million, retaining its 9 percent share.

New player Nothing recorded a standout 177 percent surge, driven by success in India.

Top smartphone vendors share Q2-2025The “Others” category saw a notable decline from 96.2 million to 93.3 million shipments, with market share dropping from 33 percent to 32 percent.

Vendors emphasized profitability through “smart volume” strategies, such as Samsung’s focus on entry-level A0x and A1x models and premium S25 series.

Outlook

Looking ahead, smartphone vendors are adjusting strategies to a flat annual outlook, emphasizing cost controls, operational efficiency, and targeted launches around AI and foldables to revive demand.

However, global smartphone vendors face challenges from cautious consumer sentiment, tariff shifts, and post-inventory corrections, especially in the United States and China, making effective channel management vital for long-term success.

Baburajan Kizhakedath