Samsung Electronics has announced plans to invest more than 110 trillion won, or about $73.24 billion, in 2026 to strengthen its semiconductor leadership, with a sharp focus on artificial intelligence (AI). The move comes amid a global AI-driven memory supercycle that is reshaping revenue models, capital expenditure priorities, and long-term industry dynamics.

AI Boom to Drive Revenue Growth and Pricing Power

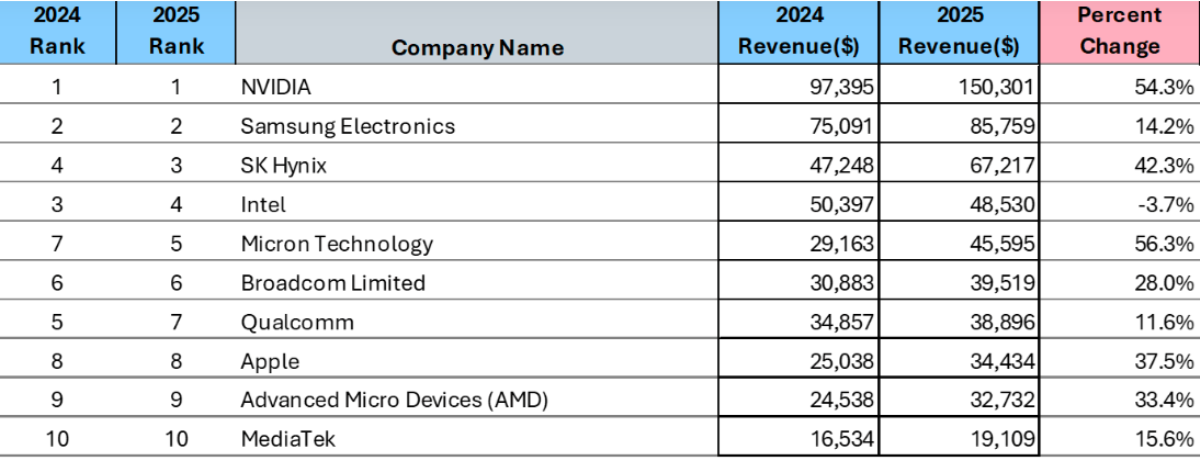

Samsung’s aggressive investment aligns with a broader industry trend where AI infrastructure is fueling unprecedented revenue expansion across memory chipmakers. Demand for high-bandwidth memory (HBM), a critical component for AI accelerators, is rising sharply, with forecasts indicating more than 70 percent growth in 2026 alone.

The HBM market itself is expected to reach about $54.6 billion in 2026, growing 58 percent year-on-year, highlighting a massive revenue opportunity for Samsung.

At the same time, supply constraints are strengthening pricing power. Analysts note that memory prices, including DRAM and NAND, are rising due to tight supply conditions and production discipline across leading players.

Capex Expansion Reflects Industry-Wide Investment Race

Samsung’s planned 110 trillion won investment marks one of the largest annual spending programs in semiconductor history. This includes both R&D and fabrication capacity expansion, particularly for advanced nodes and HBM production.

The scale of spending mirrors broader industry trends. Competitors like Micron Technology are raising annual capex beyond $25 billion, while SK Hynix continues to invest heavily in next-generation memory and packaging technologies.

Supply Constraints and Market Imbalance to Support Margins

Despite investments, the semiconductor industry is struggling to keep up with AI demand. Reports indicate that memory supply growth in 2026 will remain below historical averages, with DRAM and NAND supply rising only around 16 percent and 17 percent respectively.

At the same time, wafer shortages could persist until 2030 due to the complexity of scaling production for AI memory.

Competitive Pressure in High-Bandwidth Memory (HBM)

Samsung faces competition in the AI memory segment. SK Hynix currently leads the HBM market with over 50 percent share, while Micron Technology is rapidly gaining ground.

HBM is becoming the centerpiece of AI infrastructure, with demand expected to grow around 30 percent annually through 2030.

Samsung is expected to accelerate its HBM roadmap, including next-generation HBM4, to regain market share and compete more effectively in AI data center deployments.

AI Reshaping Semiconductor Strategy and Product Mix

AI demand is transforming how semiconductor companies allocate resources. Manufacturers are prioritizing high-margin AI memory products over traditional DRAM, tightening supply for conventional applications.

Additionally, HBM is projected to account for a growing share of total DRAM output, reflecting a structural shift in product mix toward AI-centric memory solutions.

This transition is expected to improve overall profitability, as AI memory commands significantly higher margins compared to commodity memory products.

Expansion Beyond Semiconductors and Future Growth Areas

Samsung is pursuing mergers and acquisitions in robotics, medical technology, automotive electronics, and air-conditioning solutions. This diversification strategy aligns with global trends in automation, smart mobility, and energy-efficient systems.

Samsung’s $73 billion investment is not just a capacity expansion strategy but a long-term bet on AI as the dominant driver of semiconductor revenue, positioning the company to benefit from sustained growth, higher margins, and technological leadership in the next decade.

BABURAJAN KIZHAKEDATH