Global sales of semiconductor manufacturing equipment are set to reach a new record in 2025 as artificial intelligence accelerates investments across logic, memory and advanced packaging, SEMI said on Tuesday.

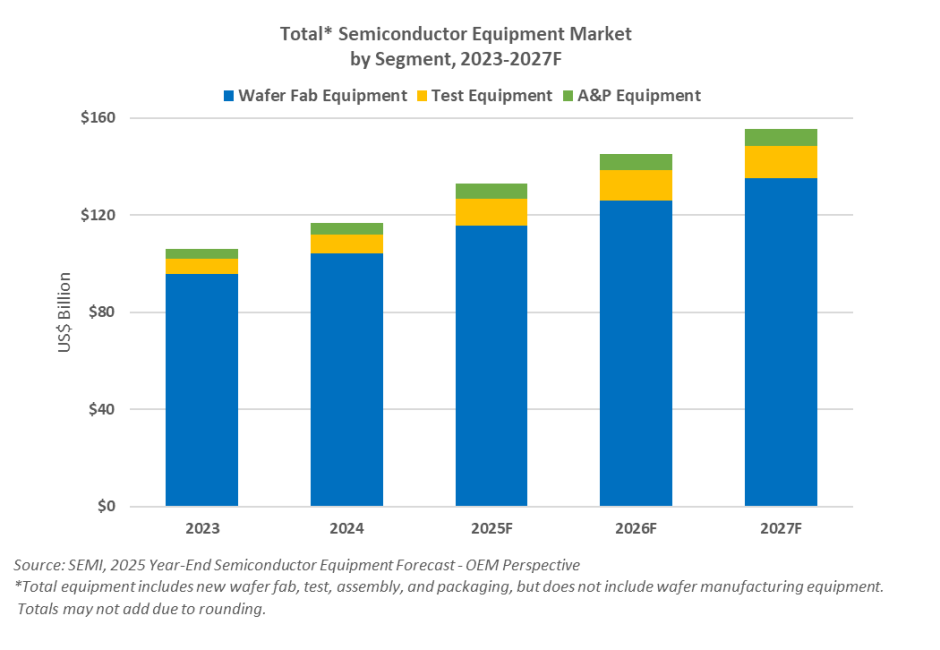

Total semiconductor manufacturing equipment sales by original equipment manufacturers are forecast to climb to $133 billion in 2025, marking growth of 13.7 percent, according to SEMI’s Year-End Total Semiconductor Equipment Forecast – OEM Perspective released at SEMICON Japan 2025.

SEMI expects the growth momentum to extend well beyond 2025. Equipment sales are projected to rise to $145 billion in 2026 and further to $156 billion in 2027, driven largely by sustained capital spending tied to AI workloads, high-bandwidth memory and leading-edge manufacturing technologies.

“Global semiconductor equipment sales show robust momentum, with both the front-end and back-end segments projected to see three consecutive years of growth, culminating in total sales surpassing $150 billion for the first time in 2027,” said Ajit Manocha, president and CEO of SEMI. He added that AI-related investments have exceeded expectations since the midyear forecast, prompting SEMI to upgrade its outlook across all major equipment segments.

Wafer Fab Equipment Leads Front-End Growth

The wafer fab equipment segment continues to anchor the industry’s expansion. After posting record sales of $104 billion last year, wafer fab equipment sales are projected to grow 11.0 percent to $115.7 billion in 2025. This reflects stronger than anticipated spending on DRAM and high-bandwidth memory to support AI computing, along with continued capacity expansion in China.

Looking ahead, wafer fab equipment sales are expected to increase 9.0 percent in 2026 and 7.3 percent in 2027, reaching $135.2 billion. SEMI said the growth will be fueled by higher investments in advanced logic nodes and next-generation memory technologies as chipmakers respond to demand from AI, data centers and high-performance computing.

Back-End Equipment Recovery Gains Strength

The back-end equipment market is also set for a strong multi-year upcycle following its recovery in 2024. Semiconductor test equipment sales are forecast to surge 48.1 percent to $11.2 billion in 2025, while assembly and packaging equipment sales are expected to rise 19.6 percent to $6.4 billion.

SEMI expects this momentum to continue through 2027, with test equipment sales growing 12.0 percent in 2026 and 7.1 percent in 2027. Assembly and packaging equipment sales are forecast to expand 9.2 percent in 2026 and 6.9 percent in 2027. The growth is being driven by more complex device architectures, rapid adoption of advanced and heterogeneous packaging, and demanding performance requirements for AI processors and high-bandwidth memory. These positives are partially offset by weaker demand in consumer, automotive and industrial markets.

Strong Demand Across Logic and Memory Applications

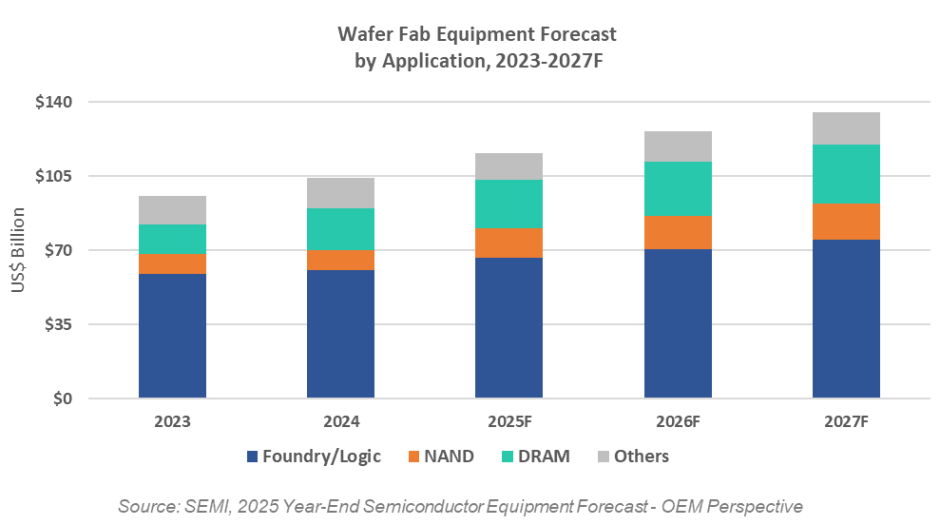

Within wafer fab equipment, spending on foundry and logic applications is projected to grow 9.8 percent year on year to $66.6 billion in 2025. The segment is expected to expand further in 2026 and 2027, reaching $75.2 billion as manufacturers add capacity for AI accelerators, premium mobile processors and high-performance computing chips. Investments are increasingly targeting leading-edge technologies, including the transition to 2nm gate-all-around manufacturing.

Memory-related equipment spending is forecast to see particularly strong growth through 2027. The NAND equipment market is expected to jump 45.4 percent to $14.0 billion in 2025, followed by continued growth through 2027 as suppliers advance 3D NAND stacking and expand capacity. DRAM equipment sales are projected to rise 15.4 percent to $22.5 billion in 2025, with further gains in subsequent years as memory makers ramp high-bandwidth memory production and migrate to more advanced process nodes.

China, Taiwan and Korea Dominate Regional Spending

China, Taiwan and South Korea are expected to remain the top three regions for semiconductor equipment spending through 2027. China is forecast to maintain its leading position as domestic chipmakers continue investing in mature and select advanced nodes, although growth is expected to moderate after 2025.

In Taiwan, strong spending in 2025 reflects large-scale leading-edge capacity builds focused on AI and high-performance computing. South Korea’s equipment investments are being driven by aggressive spending on advanced memory technologies, particularly high-bandwidth memory.

SEMI noted that all other regions are also expected to see higher equipment spending in 2026 and 2027, supported by government incentives, regionalization strategies and targeted specialty capacity expansions.

Baburajan Kizhakedath