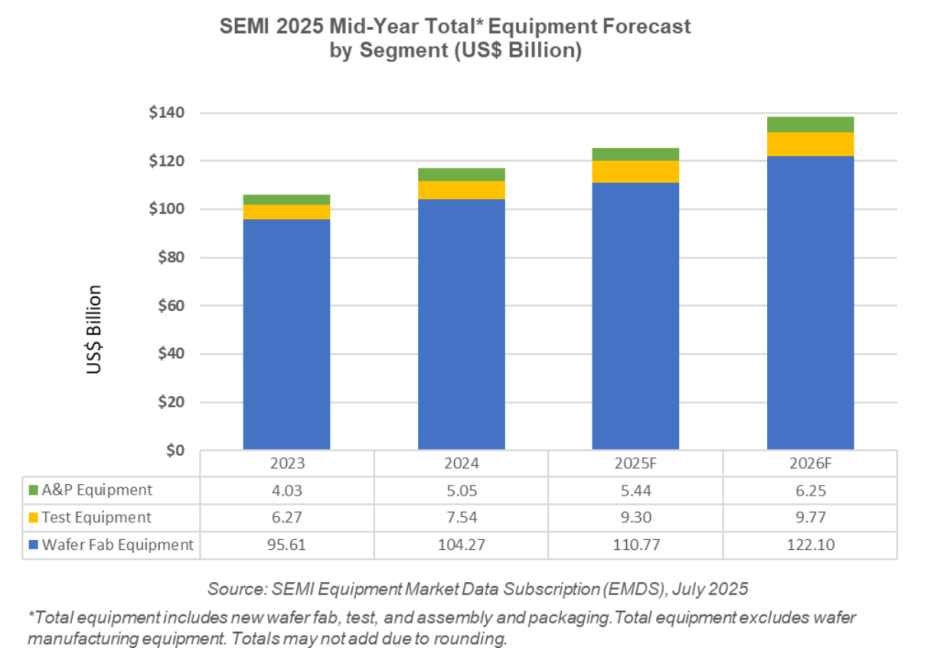

Global sales of semiconductor manufacturing equipment by OEMs are forecast to reach a record $125.5 billion in 2025, marking a 7.4 percent year-on-year increase, according to SEMI’s Mid-Year Total Semiconductor Equipment Forecast – OEM Perspective.

The growth in the sales of semiconductor manufacturing equipment is expected to continue in 2026, with sales projected to climb further to $138.1 billion, driven by surging investments in leading-edge logic, memory, and process technology transitions. SEMI President and CEO Ajit Manocha attributed this growth to AI-driven demand and ongoing capacity expansions despite prevailing macroeconomic uncertainties.

Wafer Fab Equipment (WFE), encompassing wafer processing, fab facilities, and mask/reticle equipment, is set to grow from $104.3 billion in 2024 to $110.8 billion in 2025, a 6.2 percent increase. This figure is an upward revision from SEMI’s previous forecast of $107.6 billion, spurred by higher sales to foundry and memory customers. The WFE segment is anticipated to rise 10.2 percent further in 2026 to $122.1 billion, propelled by capacity expansions for AI workloads and continued technology migration in major segments.

Back-end equipment is also on a robust growth path. Following a 20.3 percent surge in 2024, semiconductor test equipment sales are expected to grow another 23.2 percent in 2025 to a record $9.3 billion. Assembly and packaging equipment, which saw a 25.4 percent jump in 2024, is projected to increase by 7.7 percent to $5.4 billion in 2025. This upward trend is forecast to continue into 2026 with test equipment growing 5.0 percent and assembly and packaging sales expanding 15.0 percent, fueled by increasing device complexity and strong performance demands for AI and high-bandwidth memory (HBM) semiconductors, although growth will be partially constrained by weaker demand in the automotive, industrial, and consumer markets.

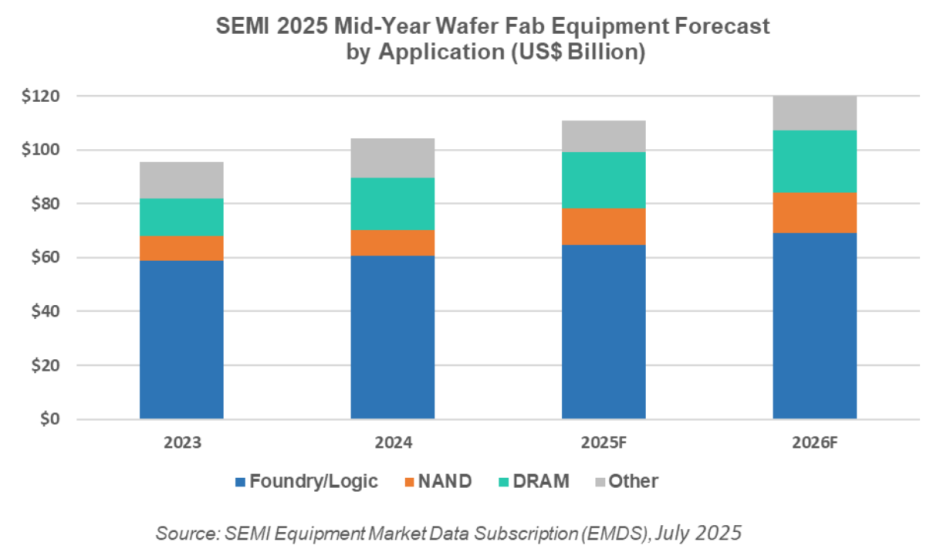

WFE sales for foundry and logic applications are projected to grow 6.7 percent year-on-year to $64.8 billion in 2025, followed by another 6.6 percent increase to $69.0 billion in 2026, supported by capacity expansions and rising demand for leading-edge technologies such as the 2nm gate-all-around (GAA) node. In memory, NAND equipment is expected to rebound strongly with a 42.5 percent growth in 2025 to $13.7 billion and a 9.7 percent increase to $15.0 billion in 2026, driven by 3D NAND stacking and capacity expansion. DRAM equipment sales, which jumped 40.2 percent in 2024 to $19.5 billion, are forecast to grow by 6.4 percent in 2025 and 12.1 percent in 2026, as HBM demand for AI applications continues to rise.

Regionally, China, Taiwan, and Korea are projected to remain the top three markets for semiconductor equipment through 2026. While China is expected to maintain its lead despite a decline from its 2024 record investment of $49.5 billion, all other regions except Europe are anticipated to see significant growth in equipment spending beginning in 2025. However, ongoing trade policy risks may influence the pace of regional expansion.

TelecomLead.com News Desk