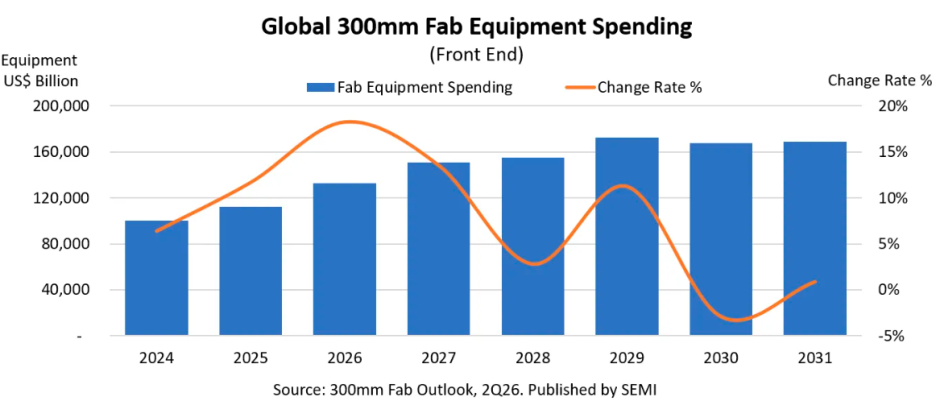

Global investment in 300mm semiconductor fabrication equipment for the memory industry is set to reach a record in 2026, fueled by surging artificial intelligence workloads, expanding hyperscale data centers, and growing demand for next-generation memory technologies.

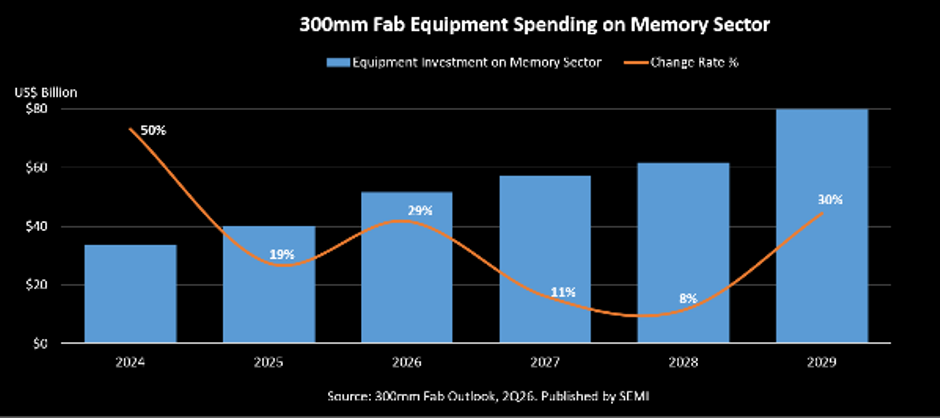

According to SEMI’s latest 300mm Fab Outlook, worldwide spending on 300mm memory fab equipment is forecast to increase 29 percent to $52 billion in 2026, marking the first time annual investment will exceed $50 billion. Investment is projected to grow by another 11 percent to $57 billion in 2027, SEMI report said.

The strong investment cycle reflects the semiconductor industry’s focus on expanding advanced memory production to support AI infrastructure, cloud computing, and high-performance computing applications. Between 2024 and 2029, worldwide 300mm memory fab equipment spending is expected to register a robust 19 percent compound annual growth rate (CAGR).

AI Demand Boosts Memory Manufacturing Capacity

The expansion of AI services is driving unprecedented demand for high-performance memory solutions such as High Bandwidth Memory (HBM), advanced DRAM, and next-generation 3D NAND flash. As a result, global 300mm memory manufacturing capacity is forecast to reach 4.1 million wafers per month in 2026, rising further to 4.2 million wafers per month in 2027.

Ajit Manocha, President and CEO of SEMI, said strong demand for HBM and other advanced memory technologies is reshaping investment priorities across the semiconductor supply chain. Growing AI infrastructure deployments are prompting memory manufacturers to accelerate investments in both production capacity and technology migration to support increasingly data-intensive applications.

DRAM Equipment Spending to Reach $37 Billion

SEMI’s 2Q26 edition of the 300mm Fab Outlook has raised its projection for memory equipment spending, citing stronger capital expenditure plans from major cloud service providers and continued demand for AI accelerators.

Investment in DRAM manufacturing equipment is expected to climb 29 percent to $37 billion in 2026. The increase is being driven primarily by rising demand for HBM and DDR5 memory used in graphics processing units (GPUs) and AI accelerator platforms powering generative AI workloads.

3D NAND Investment Climbs to $14 Billion

Investment in 3D NAND equipment is also forecast to grow significantly, rising 28 percent to $14 billion in 2026. The increase reflects expanding storage requirements as enterprises, hyperscale cloud providers, and AI developers deploy larger AI models that require massive, high-speed storage infrastructure.

Advanced Memory Technology Migration Continues

SEMI noted that ongoing investment in advanced-node DRAM, HBM, and higher-layer 3D NAND technologies is supporting an improved outlook for global memory production capacity. However, effective capacity expansion remains constrained by the increasing complexity of technology migration and manufacturing processes associated with advanced DRAM nodes, HBM integration, and higher-layer NAND transitions.

Main vendors

Applied Materials is expanding manufacturing and R&D capacity, including a $500 million expansion in Singapore, while launching new materials engineering systems for AI chips, advanced DRAM, HBM and advanced packaging. The company expects AI-driven memory investments to remain a major growth driver.

Lam Research continues to invest heavily in equipment for advanced DRAM, HBM and 3D NAND. The company is expanding technologies supporting higher-layer NAND and advanced memory scaling as AI accelerates wafer fab spending.

Tokyo Electron is increasing investment in AI-driven semiconductor manufacturing solutions, focusing on advanced DRAM, HBM, and next-generation NAND process technologies. The company expects sustained demand from leading memory manufacturers.

KLA is expanding its portfolio of inspection and metrology systems required for increasingly complex HBM, advanced DRAM and 3D NAND manufacturing, where process control has become critical for yield improvement.

ASML continues increasing shipments of advanced EUV lithography systems that enable leading-edge DRAM and HBM production. AI-related semiconductor investments continue to support strong long-term demand for its lithography platforms.

ASM International continues strengthening its ALD and epitaxy portfolio, technologies that are increasingly important for advanced DRAM scaling, HBM manufacturing and next-generation memory devices.

Major Companies Investing in 300mm Memory Fab Equipment

The current wave of investment in 300mm memory wafer fabrication equipment is being led primarily by the world’s largest DRAM and NAND manufacturers, driven by soaring demand for AI servers, High Bandwidth Memory (HBM), DDR5, and enterprise SSDs.

Samsung Electronics

Samsung remains the world’s largest memory chip producer and is investing heavily in expanding advanced DRAM, HBM, and 3D NAND manufacturing. The company recently announced plans to build two new semiconductor fabrication plants as part of South Korea’s 800 trillion won (about $518 billion) national semiconductor ecosystem initiative aimed at supporting AI-driven chip production.

SK Hynix

SK Hynix is expanding production of HBM4, advanced DRAM, and AI memory technologies. Alongside Samsung, it will build two new fabrication facilities under South Korea’s semiconductor expansion program. The company continues to prioritize HBM capacity to meet demand from AI accelerator manufacturers.

Micron Technology

Micron is significantly increasing investments in AI memory manufacturing. The company expects approximately $10 billion in capital expenditure during 2026 while expanding HBM production and advanced DRAM capacity. It has secured $22 billion in long-term supply agreements with 16 strategic customers and continues expanding manufacturing in the United States and Singapore.

Kioxia

Kioxia continues investing in next-generation BiCS 3D NAND technology and advanced 300mm manufacturing lines. While maintaining disciplined capital spending, the company is expanding production to support growing AI storage demand and expects strong demand through 2027.

Western Digital

Western Digital continues investing alongside its NAND technology roadmap to address enterprise SSD and AI storage demand. The company is focusing on higher-capacity flash memory products for cloud and AI data centers as enterprise storage requirements continue to grow.

Yangtze Memory Technologies (YMTC)

China’s YMTC continues expanding domestic 3D NAND production as part of the country’s broader semiconductor self-sufficiency strategy. The company is increasing investment in advanced NAND manufacturing despite global competition and export restrictions.

BABURAJAN KIZHAKEDATH