The legacy of U.S. tariffs introduced under the Donald Trump administration continues to impact the global foundry industry, even years after their introduction.

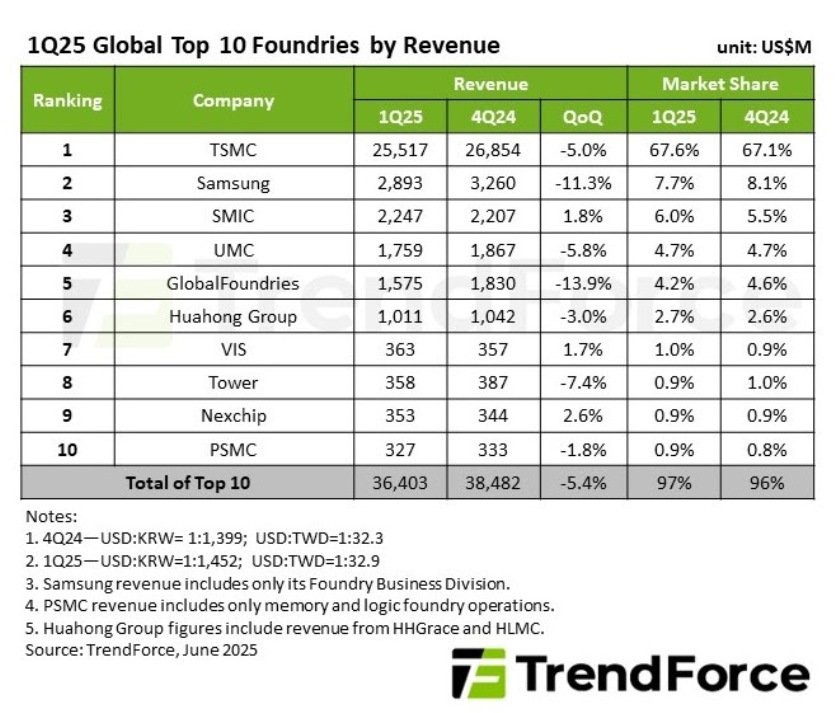

The revenue of the top 10 foundries amounted to $36.40 billion in Q1 2025, down 5.4 percent from Q4 2024, according to TrendForce. However, the downturn was cushioned in part by a wave of last-minute client orders made in anticipation of the expiration of U.S. reciprocal tariff exemptions.

These urgent purchases, driven by the desire to avoid tariff-related cost increases, temporarily boosted demand and helped offset the typical seasonal slowdown. This effect was particularly pronounced in companies with strong U.S.-China exposure or those producing components for consumer electronics targeted by tariffs.

Revenue share

In Q1 2025, TSMC reported revenue of $25,517 million, a 5.0 percent decline from Q4 2024, with a market share of 67.6 percent.

Samsung posted $2,893 million in revenue, down 11.3 percent quarter-over-quarter, holding a 7.7 percent market share.

SMIC saw its revenue rise 1.8 percent to $2,247 million, increasing its market share to 6.0 percent.

UMC generated $1,759 million in revenue, a 5.8 percent drop, maintaining a 4.7 percent market share.

GlobalFoundries reported $1,575 million, down 13.9 percent, with a 4.2 percent market share.

Huahong Group had $1,011 million in revenue, a 3.0 percent decline, holding a 2.7 percent market share.

VIS posted $363 million, growing 1.7 percent quarter-over-quarter, capturing 1.0 percent of the market. Tower earned $358 million, a 7.4 percent drop, with a 0.9 percent share.

Nexchip increased revenue by 2.6 percent to $353 million, also holding 0.9 percent market share.

PSMC saw a 1.8 percent decline to $327 million, with a 0.9 percent share.

Winners and Losers of Tariff-Induced Demand

TSMC, the dominant market leader, saw limited revenue decline thanks to its diversified demand base. Alongside strong AI and high-performance computing (HPC) demand, TSMC also received urgent orders for TV-related components — likely from clients seeking to evade upcoming tariff hikes.

China-based SMIC emerged as a notable beneficiary of the tariff environment. The company saw a 1.8 percent revenue increase in Q1, driven by early stocking strategies from domestic clients who sought to mitigate the combined impact of U.S. tariffs and capitalized on China’s consumer subsidy program. This helped SMIC offset average selling price (ASP) declines.

Similarly, Vanguard and Nexchip saw gains in revenue — up 1.7 percent and 2.6 percent respectively —buoyed by early procurement linked to tariffs and subsidies. Their higher-than-usual utilization rates during an off-season period underscore the short-term boost provided by these policies.

Tariff Fallout for Others

On the other hand, foundries with less exposure to China’s subsidy-driven demand or with clients outside the U.S.-China tariff scope saw sharper revenue declines. Samsung Foundry, for example, posted an 11.3 percent QoQ decline due to limited benefits from Chinese subsidies and continued pressure from U.S. restrictions on advanced nodes. GlobalFoundries experienced a 13.9 percent revenue drop, impacted by seasonal factors and its customer base being less active in tariff-driven pre-stocking.

Looking Ahead

While tariff-induced demand temporarily supported industry revenues in Q1, this momentum is expected to fade in Q2. Foundries now face a more normalized order cycle, with only China’s subsidy program and inventory build-up for upcoming smartphone launches providing short-term support.

Overall, the Trump-era tariffs have added new layers of volatility and complexity to foundry demand cycles, triggering defensive procurement behavior among customers and creating uneven benefits across the industry. These disruptions continue to ripple through the supply chain, influencing inventory strategies, pricing, and capacity utilization well into 2025.

Baburajan Kizhakedath