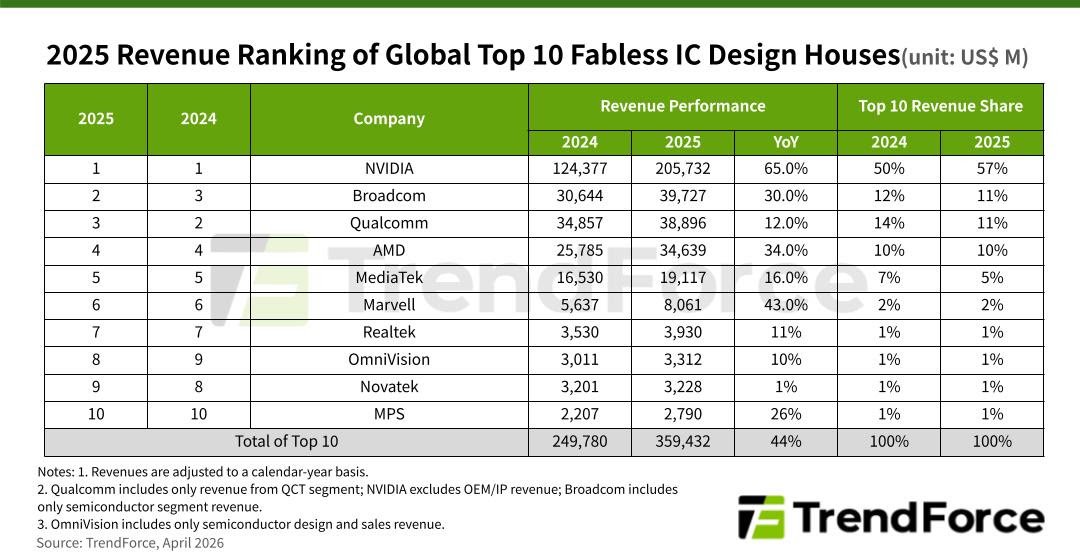

Continued investments in artificial intelligence infrastructure by major cloud service providers are accelerating growth across the semiconductor ecosystem, with fabless chip designers emerging as key beneficiaries. According to TrendForce, the top 10 fabless IC design companies generated over $359.4 billion in revenue in 2025, marking a strong 44 percent year-on-year increase driven largely by demand for AI chips, GPUs, and custom silicon.

NVIDIA retained its dominant position, delivering record-breaking revenue growth of 65 percent to $205.7 billion. The company continues to lead the AI revolution, with data center revenue contributing nearly 90 percent of its fourth-quarter earnings. NVIDIA’s expanding ecosystem, including its GPUs and software stack, has solidified its leadership, accounting for 57 percent of total revenue among the top ten players.

Strengthening its AI ambitions, NVIDIA recently announced a $2 billion investment in Marvell to co-develop advanced technologies such as customized XPUs, NVLink Fusion-based interconnects, and silicon photonics. This partnership highlights a shift in competition toward platform-level innovation, where interconnect efficiency and system integration are becoming as critical as raw compute power.

Broadcom climbed to second place with $39.7 billion in revenue, up 30 percent, fueled by growth in custom AI silicon and networking products. Its performance underscores the rising importance of Ethernet switches and network interface cards in scaling AI workloads.

Meanwhile, Qualcomm slipped to third despite posting $38.9 billion in revenue, reflecting its continued reliance on the smartphone segment. Although premium device demand supported growth, overall expansion remained moderate at 12 percent.

AMD secured fourth place with $34.6 billion in revenue, driven by over 30 percent growth in data center business, signaling increasing competition in AI servers and the rise of open computing ecosystems. MediaTek ranked fifth, benefiting from strong flagship smartphone chip shipments.

Other notable players include Marvell in sixth place, achieving 43 percent growth due to AI data center connectivity demand, and Realtek, which secured seventh despite seasonal fluctuations. OmniVision climbed to eighth, supported by rising adoption of ADAS and imaging technologies, while Novatek and Monolithic Power Systems rounded out the top ten.

Company-wise Revenue Comparison (2025 vs 2024)

NVIDIA remained the clear leader, increasing revenue from $124.4 billion in 2024 to $205.7 billion in 2025, delivering the highest growth rate of 65 percent and significantly expanding its market share.

Broadcom moved up to second place, with revenue rising from $30.6 billion to $39.7 billion, reflecting strong demand for AI networking and custom silicon.

Qualcomm slipped to third, posting moderate growth from $34.9 billion in 2024 to $38.9 billion in 2025, impacted by its reliance on the smartphone market.

AMD recorded strong gains, with revenue increasing from $25.8 billion to $34.6 billion, driven by data center and AI server demand.

MediaTek grew from $16.5 billion to $19.1 billion, supported by premium smartphone chip shipments.

Marvell delivered one of the fastest growth rates, with revenue jumping from $5.6 billion to $8.1 billion, fueled by AI connectivity and custom ASIC demand.

Realtek saw steady growth from $3.5 billion to $3.9 billion, despite seasonal fluctuations in consumer electronics.

OmniVision increased revenue from $3.0 billion to $3.3 billion, driven by imaging solutions and ADAS adoption.

Novatek remained relatively flat, with revenue inching up from $3.2 billion to $3.23 billion amid weak consumer electronics demand.

Monolithic Power Systems (MPS) grew from $2.2 billion to $2.79 billion, supported by demand for AI-related power management solutions.

BABURAJAN KIZHAKEDATH