The global media and entertainment (M&E) industry is entering a new phase of transformation in 2026, driven by the maturation of streaming platforms, the rapid rise of AI deployment, emerging content formats such as microdramas, and deeper structural partnerships between broadcasters, telcos, and streaming providers, according to the latest analysis from Omdia.

Omdia’s latest e-book, How AI, partnerships, and new revenue models are shaping the media’s future in 2026, highlights how economic uncertainty, changing consumer behavior, and fragmentation across TV and video ecosystems are redefining growth strategies for media companies, telecom operators, and technology vendors.

Media and Entertainment Industry Faces Fragmentation in 2026

Omdia said 2026 will continue to be characterized by geopolitical instability, economic uncertainty, and evolving digital consumption patterns. The addressable global M&E market is increasingly fragmented as multiple household types coexist across traditional TV, streaming, premium platforms, and free services.

In 2026, the global addressable market for media and entertainment will be divided into three major demographic groups:

31 percent of homes will rely solely on streaming services

30 percent of homes will combine traditional TV with streaming

36 percent of homes will still depend exclusively on traditional TV services

This fragmentation is intensifying competition among broadcasters, pay-TV operators, streamers, and telecom providers as each segment competes for consumer attention and subscription revenue.

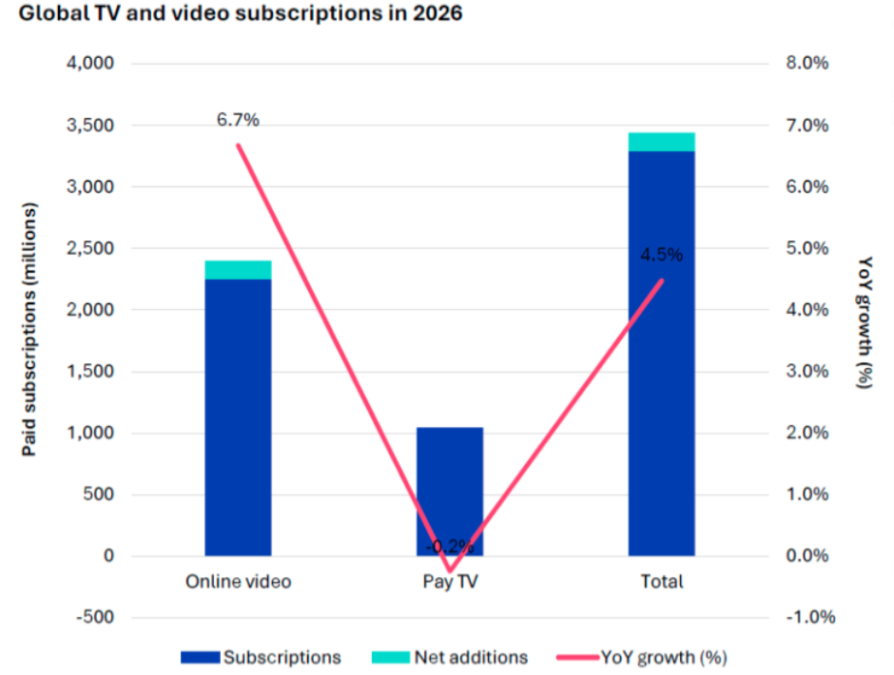

Streaming Revenue and Subscriptions to Surpass Pay TV

Streaming platforms are expected to dominate both subscription volumes and industry revenue in 2026, overtaking traditional pay-TV globally. However, Omdia noted that the streaming industry is approaching maturity, with annual growth rates slowing into single digits.

Online subscription growth in 2026 is forecast at 6.7 percent compared with 2025 levels. The report said hybrid SVOD and AVOD business models are helping sustain market momentum, particularly through the expansion of lower-cost advertising-supported subscription tiers.

Global SVOD platforms are expected to add just over 150 million net new subscriptions in 2026. Omdia noted this is a relatively modest figure that mirrors subscription growth levels last seen in 2017.

The broader TV and video industry is forecast to grow total subscriptions by 4.5 percent in 2026, adding approximately 147 million new subscriptions worldwide. Most of this growth will come from streaming platforms.

Traditional pay-TV operators are projected to lose around 2.6 million subscriptions globally in 2026. While negative, this represents an improvement compared with the severe declines recorded during 2023 to 2025, when pay-TV platforms collectively lost 32 million subscriptions.

Microdramas Emerging as Major Growth Opportunity

Omdia believes 2026 will become the breakout year for microdramas, positioning the format as one of the most important new revenue opportunities in digital video.

The analyst firm described microdramas as the mobile-first equivalent of scripted television, targeting younger viewers consuming short-form content primarily on smartphones. Unlike FAST channels, which emerged from the United States as a solution for cord-cutters seeking free linear TV, microdramas are largely originating from China and are optimized for vertical-video and social-media-driven viewing habits.

Omdia stated that the microdrama market opportunity in 2026 could become twice the size of the FAST market, underlining the growing commercial significance of short-form premium storytelling formats.

The report said telecom operators are uniquely positioned to capitalize on the trend because of their control over mobile ecosystems, smartphone distribution, and integrated digital entertainment services.

Partnerships Between Broadcasters, Telcos, and Streamers to Accelerate

Following several transformative partnership agreements across the TV and streaming industries during 2025, Omdia expects 2026 to bring a major acceleration in long-term structural integration deals.

Broadcasters, pay-TV distributors, telecom operators, and streaming platforms are expected to deepen collaboration strategies to remain competitive in an increasingly saturated market.

According to Omdia, siloed growth models are no longer sustainable. Success in 2026 will depend on integrated content ecosystems where traditional TV providers and digital streamers work together on distribution, bundling, advertising, audience monetization, and subscriber retention strategies.

The growing convergence between telecom and media sectors is expected to strengthen the role of operators as central aggregators of entertainment products and services.

AI Adoption in Media Moves Beyond Experimentation

Artificial intelligence is also entering a new stage of acceptance across the media industry. Omdia said resistance toward AI within the M&E sector is beginning to soften, even as concerns remain around copyright usage and AI involvement in creative production.

The analyst firm expects widespread pragmatic acceptance of AI technologies in 2026, particularly as media companies shift focus from opposing AI adoption to maximizing revenue opportunities and operational efficiency.

Omdia noted that companies increasingly recognize attempts to reverse AI adoption or prevent the use of copyrighted training data are unlikely to succeed long term. Instead, businesses are prioritizing monetization strategies tied to AI-powered content creation, recommendation systems, audience analytics, automation, and advertising optimization.

Asia & Oceania to Lead Global Media Revenue Growth

Among all global regions, Asia & Oceania is forecast to deliver the strongest revenue expansion for media and entertainment companies in 2026.

According to Omdia data:

Media revenue across Asia & Oceania will rise from $331.8 billion in 2025 to $359.7 billion in 2026

The region will generate an annual revenue increase of $27.9 billion

North America will record a comparable increase of $27.7 billion

Western Europe is expected to add approximately $10 billion in media revenue during 2026

The report covers multiple media categories, including music, gaming, cinema, TV, and online video.

Omdia Recommendations for Operators and Vendors

Omdia advised service providers and telecom operators to prepare for the rapid emergence of microdramas and other new digital content models. Operators were encouraged to integrate these formats into existing entertainment ecosystems to capture younger mobile-first audiences.

The firm also recommended that operators continue strengthening partnerships across both traditional TV and streaming ecosystems instead of attempting to compete independently.

For technology vendors, Omdia warned that increasing market maturity may limit future growth opportunities, making flexibility and long-term partnership strategies increasingly important.

Vendors were also advised to remain agile in supporting the microdrama ecosystem, especially because many short-form content platforms already possess vertically integrated in-house technology stacks optimized for mobile and social video experiences.

BABURAJAN KIZHAKEDATH