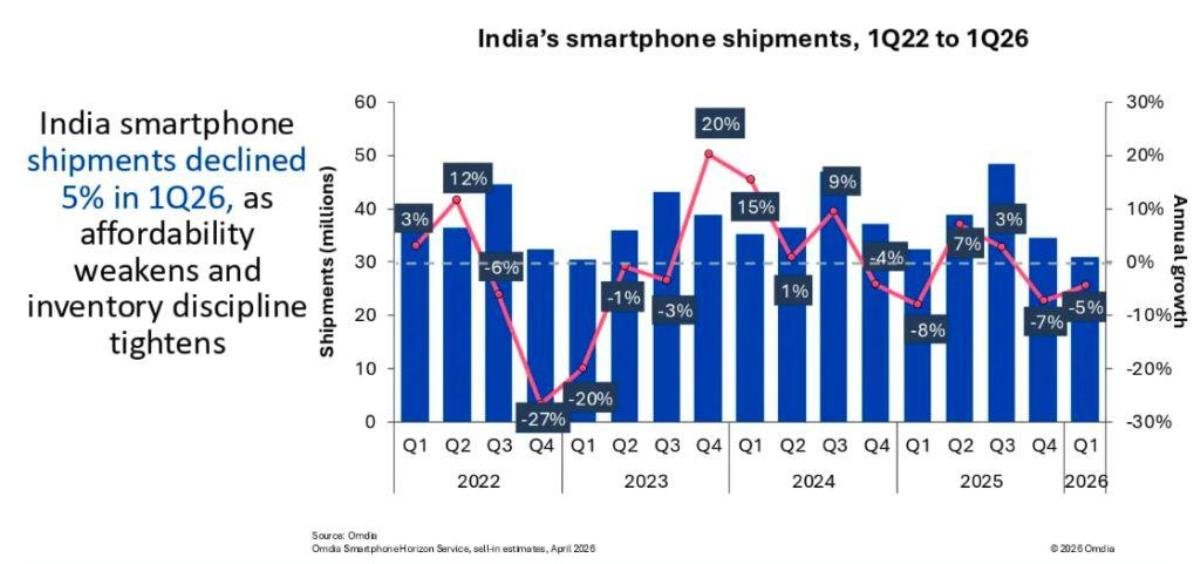

India’s smartphone market entered 2026 on a weak footing, with shipments declining 5 percent year on year to 30.9 million units in Q1 2026, according to Omdia. The decline reflects seasonally soft demand combined with cautious channel inventory strategies, as vendors and retailers adjusted to rising cost pressures and uncertain consumer sentiment, Sanyam Chaurasia, Principal Analyst at Omdia, said.

Macroeconomic challenges played a central role in dampening demand. Rupee depreciation and rising inflation reduced consumer affordability, while expectations of further price increases led to earlier front-loading of purchases, limiting fresh channel intake during the quarter. As a result, upgrade cycles slowed, and discretionary spending remained constrained, Omdia report said.

Vivo retained its top position with shipments steady at 6.3 million units, maintaining a 20 percent market share year on year. Strong traction from its V70 series and consistent sell-out performance supported its dominance.

Samsung held firm in second place with 5.1 million units and a 16 percent share, showing no change compared to Q1 2025. Samsung’s performance in the India smartphone market was driven by late-quarter momentum from flagship Galaxy S26 launches, refreshed A-series models, and solid entry-level volumes from A07 and A17 devices.

OPPO was the standout performer, increasing shipments from 3.9 million to 4.7 million units, boosting its market share from 12 percent to 15 percent, reflecting 21 percent annual growth. Growth was fueled by strong demand across the A6x, K14, and Reno 15 series, supported by a broader SKU mix spanning mid-range to premium segments.

Xiaomi saw shipments decline from 4.0 million to 3.8 million units, though its market share remained stable at 12 percent.

Apple experienced a drop in shipments from 3.2 million to 2.9 million units, with market share slipping from 10 percent to 9 percent. Apple’s entry into India’s top five in Q1 for the first time highlighted increasing traction in the premium segment.

The “Others” category declined significantly, with shipments falling from 9.9 million to 8.2 million units and market share shrinking from 30 percent to 27 percent.

Pricing Strategies Diverge Amid Cost Pressures

Rising component costs, particularly memory inflation, forced vendors to adopt varied pricing strategies. OPPO implemented flat, portfolio-wide price hikes to reset margins quickly, while Xiaomi pursued a tiered pricing approach to prioritize higher-value SKUs. In contrast, Samsung and vivo opted for phased price increases to protect demand and maintain smoother channel absorption.

These pricing differences were most visible in the ₹10,000 to ₹20,000 segment, where uniform price hikes reduced affordability and impacted volume growth. At the same time, overlapping old and new inventory increased the complexity of channel execution, making inventory management a critical differentiator.

Smaller Vendors Struggle as Market Consolidates

While leading brands demonstrated resilience, smaller vendors faced mounting challenges. Rising costs and weaker channel confidence led to sharper declines among long-tail players. However, select brands such as Motorola, iQOO, and Google showed relative stability, supported by focused product strategies and niche positioning.

India Smartphone Market Faces Double-Digit Decline Risk in 2026

Looking ahead, Omdia warns of significant downside risk, with India’s smartphone shipments expected to decline by double digits in 2026. Price increases have accelerated into Q2 2026, with entry-level devices already seeing steep hikes of 18 percent to 20 percent due to sustained memory cost inflation.

As affordability pressures intensify, consumer behavior is shifting. Demand in the entry-level segment is increasingly moving toward repairs, second-hand devices, and financing-led purchases, while upgrade cycles are expected to lengthen further.

Long-Term Strategy Critical for Vendors

The evolving market environment signals a structural reset rather than a temporary slowdown. Vendors must balance margin recovery with demand sensitivity, while aligning channel inventory to avoid disruptions. Companies that adapt their business models and revenue strategies for long-term sustainability, rather than focusing solely on short-term survival, are likely to emerge stronger in India’s highly competitive smartphone market.

BABURAJAN KIZHAKEDATH