The consolidation in the telecom sector has been favorable for Bharti Airtel, after many years of weak returns on capital, is now set to see a swing in its fortunes, Motilal Oswal Financial Services said.

Consistent market share gains, organic ARPU improvements and controlled costs have boosted Airtel’s EBITDA, offsetting the higher Capex internally and continued deleveraging. Over the next couple of years, we believe that Airtel will continue to benefit from the favorable market construct, which should result in improvements in FCF and ROCE. The company is expected to execute awaited tariff hikes in the next couple of quarters, which could act as a catalyst for the stock, in our view.

Tariff hike to support growth

We expect the awaited tariff hike (assuming 20 percent) to take place in the next couple of quarters after the general election, which could increase EBITDA by 12-15 percent. We currently do not factor in a material price hike in our model. A 20 percent price hike should increase Airtel’s ARPU to INR270 in FY26E. At 70 percent incremental margin, India Wireless EBITDA should rise to INR 580 billion / INR 688 billion in FY25E/FY26E. Factoring in a tariff hike, Airtel could generate post-interest FCF of INR 247 billion in FY25E and INR350b in FY26E, representing to a 3-5 percent FCF yield (highest in last 10 years).

Long-term growth story favorable for Airtel

Over the last four years (FY20-24E), Airtel’s India Mobile business posted a CAGR of 17 percent/29 percent in revenue/EBITDA, driven by multiple tariff hikes (strong 40 percent growth in ARPU), market share gains, 2G-to-4G subscriber shift, premiumization toward postpaid, and reduction in spectrum usage charges. However, in the last few quarters, growth has decelerated due to the absence of a tariff hike, slower market share gains and lower mix benefits as the base of 2G tariffs has gone up.

Airtel and Reliance Jio both should be the key beneficiaries in gaining subscriber/AGR market share: a) the heavy capex by the two strong players, underscoring the opportunity for the monetization of 5G and tariff hikes; and b) once Vodafone Idea’s (VIL) debt moratorium (AGR + spectrum liability) expires in FY26E, its ~INR 400 billion revenue size may offer a strong market share growth opportunity in two years. Further, in the long term, there should be opportunities to monetize heavy investments as the Indian telecom market size of INR2.3t is largely served by merely two sizeable players – Jio and Airtel, with far lower competitive intensity.

VIL has raised INR 200 billion via equity in the combination of FPO and INR 20.75 billion preferential allotment to promoter, Aditya Birla Group (ABG). VIL plans to raise additional INR 250 billion via debt. Following are our views on this fundraise:

Near-term support for VIL: VIL plans to utilize the funds for capex, which is a welcome move as it should improve its 4G capabilities; however, the magnitude of investment requirement and timelines may be key in arresting its market share loss. Further, VIL needs to significantly increase its EBITDA (INR84b in FY24E pre INDAS 116) to service ~INR300b AGR and spectrum annual installment in FY26 and INR 430 billion FY27 onward.

No risk to Airtel from change in competitive landscape: Unlike the risk of increasing market share competition, we believe the profitability consciousness will provide continued tariff hike opportunities over the next 2-3 years.

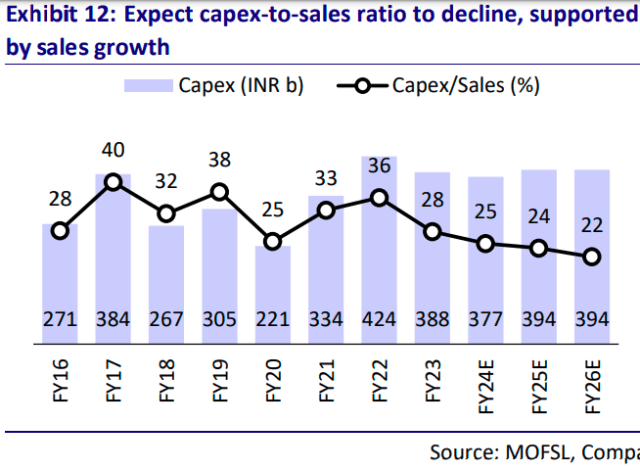

5G Capex may remain prolonged but the cash flow may subside the impact

Jio and Airtel together deployed 436k 5G base transceiver stations (BTS) by Mar 2024, up 8x from 54k in Jan 2023. We expect the large proportion of BTS deployment to be done by Jio as Airtel has deployed 100k mobile broadband base stations (including 3G/4G/5G) in the last one year.

We expect this gap in BTS deployment will keep the 5G Capex prolonged and expect the consolidated Capex to remain around INR 400 billion for FY25-26. The positive factor is that the operating profit generation would be enough to fund the capex requirement internally, unlike during the 4G investment cycle.

Visibility for high FCF/ROCE

After 10 years, Airtel is once again in a sweet spot. It is returning to a healthy monetization stage thanks to EBITDA improvement. We estimate Its FCF yield (with tariff hike) at 3-5 percent, with RoCE at ~13 percent/15 percent in FY25/FY26. FCF has increased to INR52b in FY24E, despite 5G Capex and deleveraging limited to INR 135 billion. We expect BHARTI’s cumulative OCF/FCF of INR1.3t/INR500b for the next two years. Moreover, inflows from the ~INR210b rights issue could help it reduce debt. Gross/net debt (excluding lease liability) currently stand at INR1.6t/INR1.3t, and we expect net debt to come down to INR500b in FY26. EBITDA improvement, together with a reduction in net debt, could result in ROCE improvement (with tariff hike) to ~15 percent in FY26E vs. 9.4 percent in FY24E, after many years of weak RoCE (lower-mid single digit).

Over the next 2-3 years, with a tariff hike, Airtel has the opportunity to grow its EBITDA by 40-50 percent and halve its net debt. The company is well poised to gain from sector tailwinds, stemming from 1) market share gains, 2) improved ARPU led by premiumization and tariff hikes, and 3) non-wireless segments, including Home and Enterprise. The key catalysts would be ARPU hike and moderation in capex. We do not expect any major probability of earnings cuts; hence, the risk-reward looks favorable at the current valuation (without factoring in tariff hike).