The global private mobile network market continues to gain momentum as enterprises, governments, manufacturers, utilities, ports, and mining companies increasingly deploy dedicated LTE and 5G networks to support digital transformation, automation, security, and mission-critical communications.

According to the latest Global mobile Suppliers Association (GSA) Private Mobile Networks Summary Report released in June 2026, the number of private mobile network customer references has reached 2,003, highlighting the growing demand for enterprise-grade wireless connectivity.

The GSA report indicated that 2,003 organizations and government entities had deployed at least one private mobile network project valued at more than €100,000 by the end of the first quarter of 2026. An additional 178 projects were valued between €50,000 and €100,000, a category introduced in 2024 to capture smaller deployments and trials. During the first quarter of 2026 alone, the market added 48 new customer references valued above €100,000 and eight projects valued between €50,000 and €100,000.

Private mobile network deployments now span 88 countries worldwide. GSA has identified country-level information for 1,615 deployments, representing 85 percent of all customer references. Lithuania, Namibia, and Suriname were among the latest countries added to the database.

Canada recorded the fastest growth among the top ten reporting countries, with customer references increasing by 5 percent during the quarter, followed by the United Kingdom at 4 percent, the United States at 2 percent, and Germany at 1 percent.

The GSA report indicates strong industry participation across the ecosystem. More than 50 equipment providers have supplied LTE or 5G private network infrastructure, while over 66 telecom operators have been involved in private mobile network projects. The market also includes system integrators, software vendors, consulting firms, and hyperscale cloud providers offering private network solutions either independently or through partnerships with operators and network vendors.

Technology adoption continues to shift toward 5G. LTE remains the dominant technology, deployed by 1,369 identified customers. However, 5G is now being used by 974 customers, representing 49 percent of all cataloged deployments.

Pure 5G networks account for 30.3 percent of customers, up by one percentage point compared with the fourth quarter of 2025.

LTE-only networks represent 50 percent of deployments, while networks using both LTE and 5G account for 18.3 percent. GSM-R deployments represent 1.1 percent of the market, while 0.2 percent remain unconfirmed.

Manufacturing remains the leading industry for private mobile network adoption, with 387 identified deployments. Education and academic research follows with 171 deployments, while mining accounts for 146 deployments. Defense and peacekeeping organizations have deployed 130 networks, while both device testing and lab-as-a-service facilities and power utility companies account for 119 deployments each. Manufacturing added 13 new customer references during the quarter, while seaports and mining each added six new deployments.

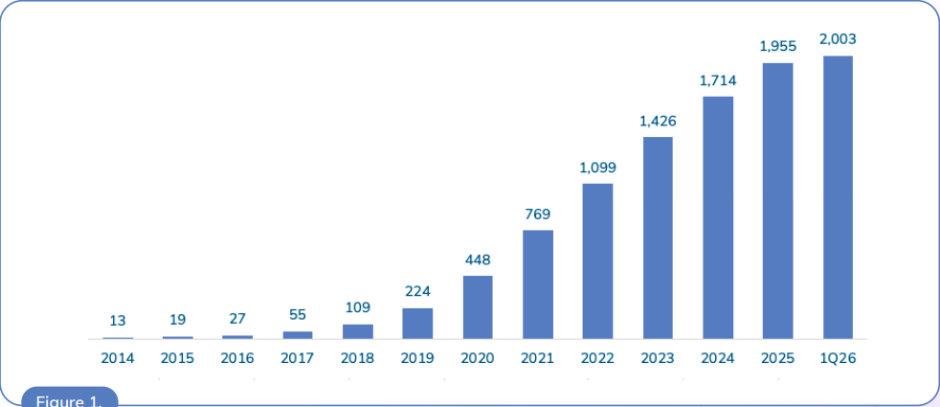

The GSA database reveals that customer announcements for private mobile networks have grown at a compound annual growth rate (CAGR) of 37 percent between 2019 and 2026. The number of identified customer references increased from 224 in 2019 to 448 in 2020, 769 in 2021, 1,099 in 2022, 1,426 in 2023, 1,714 in 2024, 1,955 in 2025, and 2,003 in the first quarter of 2026.

According to GSA, approximately 76 percent of all private mobile network references in its database are non-public and unique deployments contributed by members of the GSA Private Mobile Networks Special Interest Group. In sectors such as military and defense, maritime, and power plants, more than 80 percent of deployments are not publicly disclosed. The Special Interest Group currently includes 17 companies and organizations, including 450Alliance, 5G-ACIA, AiLink, Airspan, Celona, Dell, Ericsson, GSMA, JMA Wireless, Keysight Technologies, Mavenir, Monogoto, Nokia, OnGo Alliance, OneLayer, PrivateLTEand5G.com, and TCCA.

The United States, Germany, the United Kingdom, China, and Japan continue to lead the global private mobile network market. GSA notes a strong correlation between the availability of dedicated spectrum and the number of private network deployments, suggesting that regulatory support remains a key driver of market growth. With more regulators making LTE and 5G spectrum available for enterprise use, GSA expects significant developments in the private mobile network sector throughout 2026 and beyond.

BABURAJAN KIZHAKEDATH