The Telecom Regulatory Authority of India’s (TRAI) report on the latest subscriber data for January 2025 reveals early signs of how 5G investments are shaping the mobile internet business in the country.

Although the overall broadband subscriber base saw only a marginal monthly growth of 0.04 percent, mobile broadband continues to be the primary growth driver, increasing from 898.57 million to 899.04 million subscribers.

A key development is the inclusion of 5G Fixed Wireless Access (FWA) users in the wireless category, adding 5.72 million new subscribers, the majority of whom (over 96 percent) are from urban areas. This shift highlights the accelerating rollout of 5G infrastructure in urban India and the initial concentration of next-gen connectivity in cities. The urban-rural digital divide, however, remains stark.

Despite the slow overall rise in wireless mobile users (from 1,150.66 million to 1,151.29 million, just 0.05 percent), the reclassification of 5G FWA has driven a noticeable 0.55 percent jump in the broader wireless segment. This change points to how advanced wireless technologies are reshaping traditional telecom reporting and user bases.

Further reflecting the digital transformation, Machine-to-Machine (M2M) mobile connections surged by 4 million, reaching 63.09 million. This growth signals increasing adoption of IoT across sectors like smart cities, logistics, and industrial automation — areas where 5G’s low latency and high bandwidth are critical enablers.

Broadband subscribers

Total broadband subscribers saw a modest increase from 944.96 million in December 2024 to 945.16 million in January 2025, reflecting a monthly growth rate of just 0.04 percent. While the overall broadband growth was minimal, the underlying trends within its subcategories tell a more nuanced story.

Mobile broadband remained the key driver of growth, increasing from 898.57 million to 899.04 million. In contrast, fixed (wired) broadband subscriptions declined slightly from 41.19 million to 41.15 million. Fixed wireless broadband saw a more noticeable drop from 5.21 million to 4.98 million, underscoring a continuing shift in consumer preference toward mobile and more flexible connectivity options.

Fixed broadband

The top five fixed broadband operators showed a continued consolidation of market share among major players.

Reliance Jio maintained its lead with 11.48 million subscribers, followed by Bharti Airtel at 8.55 million and Bharat Sanchar Nigam at 4.26 million. Atria Convergence Technologies and Kerala Vision Broadband rounded out the top five with 2.28 million and 1.28 million subscribers, respectively.

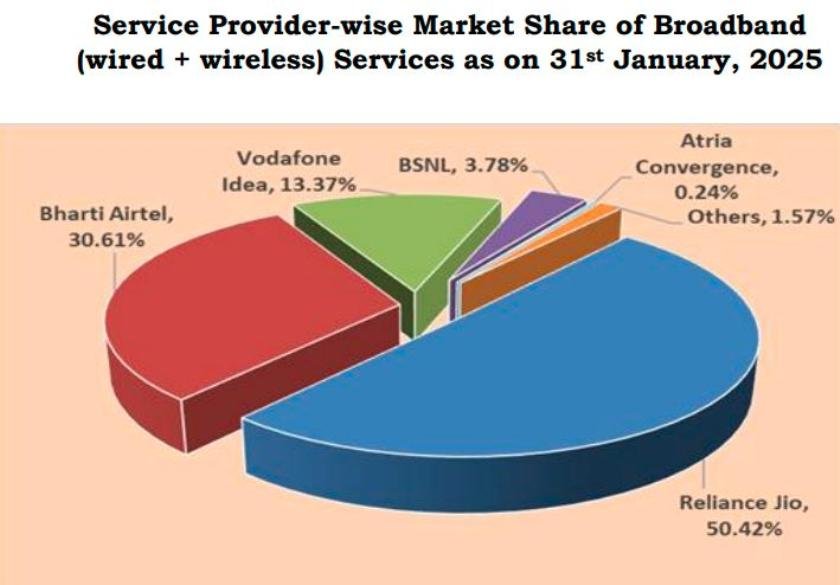

When looking at overall broadband (including mobile and wireless), Reliance Jio again led with a massive 465.10 million subscribers, followed by Bharti Airtel at 280.76 million, Vodafone Idea at 126.41 million, Bharat Sanchar Nigam at 31.52 million, and Intech Online with a minimal footprint at 0.09 million.

The wireless segment showed a notable overall increase in subscribers, jumping from 1,150.66 million in December 2024 to 1,157 million in January 2025 — a growth rate of 0.55 percent. This jump, however, is largely attributable to a reporting shift that moved 5G Fixed Wireless Access (FWA) subscribers from the wireline to wireless category.

The inclusion of 5G FWA significantly altered the statistical landscape, introducing 5.72 million new subscribers into the wireless base, with 5.513 million in urban areas and only 0.202 million in rural areas. Urban users accounted for a dominant 96.46 percent of the 5G FWA total, highlighting a pronounced urban-rural divide in the early adoption of advanced wireless technology.

When examining the mobile wireless category specifically, growth remained nearly flat, moving from 1,150.66 million to 1,151.29 million, a marginal increase of 0.05 percent. Urban mobile wireless subscriptions actually saw a slight decline, from 627.08 million to 626.08 million — a drop of 0.06 percent — while rural areas experienced a small gain, from 523.28 million to 525.20 million, with a growth rate of 0.19 percent. These shifts may reflect market saturation in urban centers and incremental growth potential in rural markets.

Additionally, the total wireless subscriptions in urban areas — factoring in both mobile and 5G FWA —increased from 627.08 million to 631.60 million, while rural subscriptions rose from 523.28 million to 525.41 million. This translates to a higher urban growth rate of 0.82 percent, compared to 0.23 percent in rural areas, once again emphasizing the stronger demand or faster rollout capacity in urban regions.

Another significant data point is the Machine-to-Machine (M2M) cellular mobile connections, which increased from 59.09 million to 63.09 million, indicating growing adoption of IoT applications. This 4 million jump suggests momentum in sectors relying on automated device communication, such as logistics, utilities, and smart infrastructure.

While total broadband and mobile subscriptions show only marginal gains, the reclassification of 5G FWA and growth in M2M connections indicate deeper transformations in how users and devices are connecting. The rural-urban gap persists across all segments, particularly in advanced technologies like 5G FWA, highlighting a continuing digital divide that may require targeted policy and infrastructure efforts.

Baburajan Kizhakedath