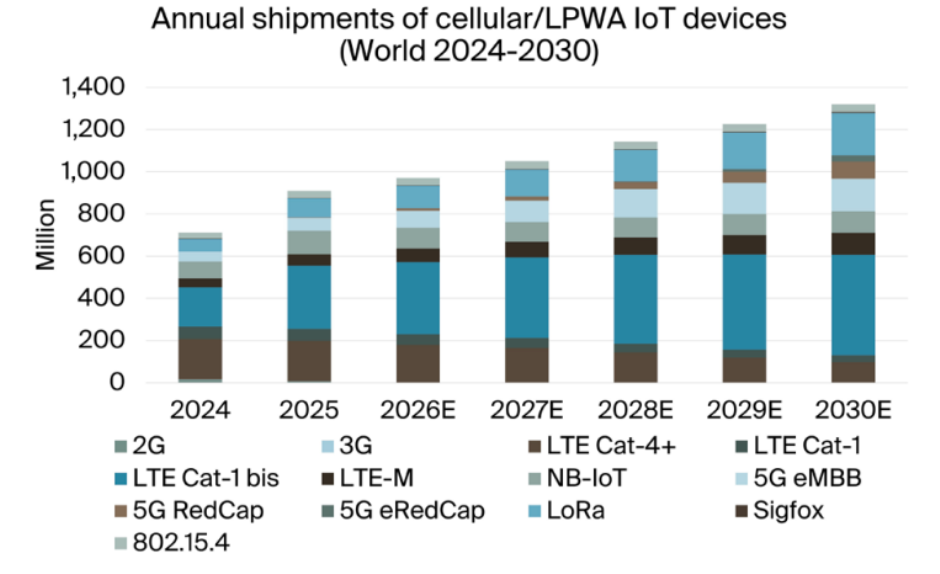

The global market for cellular Internet of Things (IoT) and Low Power Wide Area (LPWA) connectivity technologies is entering a new phase of expansion, with annual shipments of cellular and non-3GPP LPWA IoT modules projected to increase from 909 million units in 2025 to 1.32 billion units by 2030, representing a compound annual growth rate (CAGR) of 7.7 percent, according to the latest Berg Insight report.

By the end of 2025, approximately 4.8 billion devices were connected to wide area networks using cellular and LPWA technologies, highlighting the rapid expansion of IoT deployments across industries. The market spans multiple ecosystems, including 2G, 3G, 4G, 5G cellular, LoRa, Sigfox, IEEE 802.15.4-based protocols, Wirepas Mesh, DECT-2020 NR (NR+), and Mioty.

The report shows that shipments of cellular IoT modules, excluding automotive Network Access Device (NAD) modules, reached 612 million units in 2025, marking 33 percent year-on-year growth. Annual revenue from cellular IoT modules increased 19 percent to US$5.6 billion.

The leading module vendors by revenue were Quectel, Fibocom, Telit Cinterion, MeiG, and China Mobile IoT, which together accounted for 73 percent of the market.

In shipment volumes, Quectel, China Mobile IoT, Sunsea AIoT, Lierda, and Fibocom dominated, while ZXInfoTek strengthened its position through the point-of-sale terminal market.

Major IoT chipset suppliers include ASR Microelectronics, Qualcomm, Eigencomm, UNISOC, Xinyi, and MediaTek.

Cellular IoT module shipments are forecast to grow at a 7.2 percent CAGR, reaching 976 million units by 2030.

In the automotive sector, Quectel led the NAD module market with a 27 percent share, followed by Rolling Wireless with 13 percent. Other important suppliers include LG Electronics, Aumovio, Kontron, Favalon (Fibocom), MeiG, and Compal. Qualcomm remained the dominant automotive chipset supplier, while MediaTek ranked second. NAD module shipments are expected to rise from 78 million units in 2025 to 98 million units by 2030, representing a 4.6 percent CAGR.

LoRa continues to strengthen its position as a global IoT connectivity platform. Cumulative shipments of LoRa end nodes reached 500 million at the beginning of 2026, with private networks accounting for most deployments. Smart gas and water metering remain the largest application segments, followed by smart sensors and asset tracking across cities, industrial facilities, and commercial buildings.

The expansion of Amazon Sidewalk beyond the United States is expected to accelerate smart home adoption.

Annual LoRa device shipments reached 90 million units in 2025 and are forecast to increase at a 17.5 percent CAGR to 202 million units by 2030.

Emerging LPWA technologies are also gaining momentum. Wirepas Mesh surpassed an installed base of 20 million devices in early 2026, while Sigfox ended 2025 with 15 million installed devices under the ownership of Singapore-based UnaBiz. Mioty has exceeded 1 million installed devices, driven by smart water metering projects, while DECT-2020 NR (NR+) remains in the pilot and early commercial deployment phase. IEEE 802.15.4 continues to be the most mature technology among emerging LPWA standards, with broad adoption in smart metering applications.

SHAFANA FAZAL