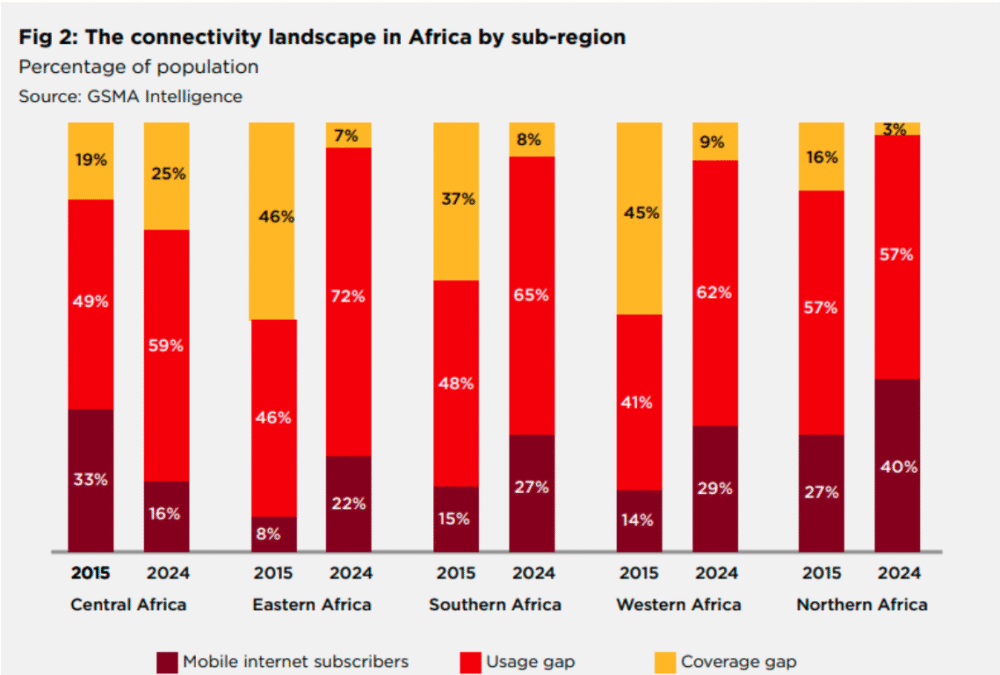

Africa faces a significant mobile internet usage gap despite major improvements in network coverage. While the coverage gap narrowed sharply from 41 percent in 2015 to 9 percent in 2024, the usage gap widened by nearly 20 percentage points over the same period, reaching 64 percent. Africa accounts for 33 percent of the world’s unconnected population, largely due to low smartphone ownership and adoption, GSMA Intelligence said in a report.

Smartphone affordability remains the primary barrier. In 2024, smartphone ownership penetration in Africa was only 24 percent of the population, far below the global average of 56 percent. In Sub-Saharan Africa, the median price of an entry-level smartphone increased from about $38 in 2023 to $39 in 2024, representing 26 percent of monthly GDP per capita, compared with 16 percent across low- and middle-income countries. While mobile data is relatively affordable at around 2 percent of monthly income, the high cost of devices continues to limit access, particularly for lower-income groups. As a result, only 40 percent of mobile internet subscribers in Africa use a 4G or 5G smartphone, slowing digital inclusion despite expanding network availability.

Africa’s smartphone market remains heavily dependent on imports from China and other Asian countries due to the absence of large-scale domestic manufacturing. Imported devices face shipping costs, customs delays, import duties and distribution margins, significantly inflating retail prices. As a result, a smartphone with an ex-factory price of $50 in China typically sells for $90 to $110 in African markets, an increase of 80 to 120 percent.

To improve affordability and create jobs, governments and OEMs have promoted local smartphone production, mainly through assembly plants. Several facilities have been established or expanded in recent years, often with government support or international partnerships, including initiatives in South Africa, Zimbabwe and Angola. However, most African plants rely on completely knocked-down or semi-knocked-down kits, importing key components rather than manufacturing them locally. This dependence on global supply chains, combined with high energy costs, skills shortages and continued logistics and customs expenses, limits cost competitiveness. In addition, strong consumer preference for well-known international brands with higher specifications constrains demand for locally assembled devices, leading to weak performance and, in some cases, the suspension of operations by domestic manufacturers.

Mobile operators in Africa have invested nearly $120 billion over the past decade to expand network infrastructure, with a strong focus on mobile broadband. This investment has driven a sharp rise in coverage, with 3G reaching 91 percent of the population and 4G expanding from 7 percent to 78 percent by the end of 2024. Nearly 50 operators have also launched 5G services, extending 5G coverage to about 12 percent of the population.

Despite these advances, the transition away from legacy 2G and 3G networks remains slow in Africa. While network shutdowns are accelerating globally, only operators in seven African countries have announced plans to phase out 2G and or 3G by 2030. As of September 2025, 2G and 3G still account for almost half of all mobile connections in the region, underscoring the scale of the migration challenge. Although 4G and 5G now cover most of the population, successful network transition will also depend on the wider availability and affordability of 4G, VoLTE and 5G capable devices, as many users continue to rely on 3G smartphones or feature phones.

BABURAJAN KIZHAKEDATH